JPMorgan Has Some Bad News For Hedge Funds Hoping The Nightmare Ends Soon

For a few hours this morning it seemed that all was lost for r/WallStreetBets and their crusade to teach Wall Street billionaires a lesson, when one exchange after another banned buying in the most-shorted stocks, an unprecedented unilateral decision made by brokerages (one of which, Robinhood, is effectively joined at the hip with hedge fund Citadel, which in turn is a part owner of Melvin Capital which was destroyed by the short squeeze that Robinhood banned, so a clear conflict of interest), and one which sent GME stock as low as $112 after trading at $500 just hours earlier.

However the hedge funds short Gamestop, who may have declared victory prematurely, had to put the champagne back on ice because just after the close, amid tremendous pushback from clients, Congress, and the public - not to mention what appears to be a liquidity crisis as millions of accounts bailed - Robinhood announced it would allow buying to resume on Friday, sending the stock up almost double after hours.

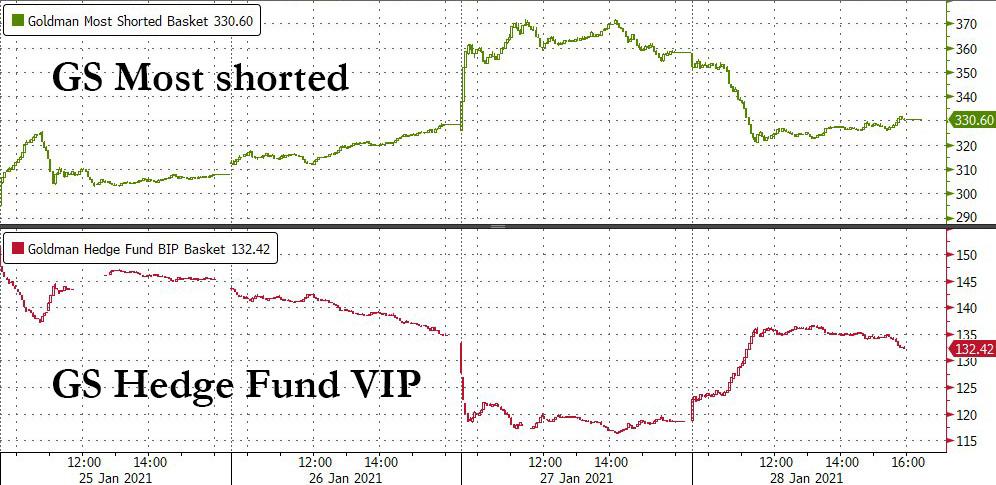

And since any victory for the WallStreetBets crowd means the short squeeze is back, it also means that a defeat for hedge funds, as can be seen in the chart below which shows that the Goldman most shorted basket is a mirror image of the Goldman hedge fund VIP basket.

In other words, any expectation that the WSB crowd would be finally crushed today and the hedge fund world would return to normalcy was crushed.

But what happens next, and how does it all end?

Last night we speculated that if indeed there are more shorts - both synthetically or otherwise - than available shares, then the only place bearish hedge funds will be get shares to cover their shorts is from the company itself. Which means that Gamestop can theoretically ask for any price (somewhat reasonable) and hedge funds will have to agree. After all, it's not GME's fault that hedge funds were so greedy they overshorted the company, which really is what all this boils down to.

The only wait out of this for the shorts may be to beg for the company to sell them stock. And GME can name any price https://t.co/4785L2P3VB

— zerohedge (@zerohedge) January 28, 2021

Of course, that is a bit of an idealistic take, one where hedge funds finally are forced to pay for their stupidity. Alas, in a country as corrupt as this one, that's unlikely to ever happen. Still, that doesn't change the fact that the answer suddenly matters extremely.

In fact, as JPM's Andrew Tyler writes in his EOD market intelligence note, "Are we there yet" -i.e., is the squeeze over - is "the biggest question and hardest to answer definitively."

Here is his take.

- POSITIONING INTELLIGENCE: The team published a new note, Tactical Takes | De-Grossing Accelerates – 1-Day Magnitude in Line with Last March, but Medium Trend Not There Yet

- Summary of what we saw yesterday:

- Globally, yesterday was a >3z (i.e. standard deviation) de-gross day with vastmajority (80%) happening in US, but did see it in EMEA (about 2z) and APAC(~1z).

- Equity L/S funds were the main ones reducing exposure in the US – for perspective, Tues was a -3z de-gross day and Wed was about 2x that.

- Quants were de-grossing DoD as well, but magnitudes were more in line with Tues, which was a 1z event.

- Despite all the recent Active de-grossing, gross and net $ exposure are relativelyunchanged YTD (because market still up in some parts, e.g. small caps, and HighSI names up a lot).

- For the US High SI names, yesterday appeared to be a ~5z covering event

- Notionally, because these stocks have rallied so much, the SMV is barelydown YTD, but the magnitude of the active covering over the past fewweeks appears to be nearly in line with what we saw last March.

- Performance on Wed was worst of past 3 days with long-short spread nearlydouble the worst days in March ’20 for L/S funds (long-short spread for Quants andMulti-Strats was quite negative as well).

- Are we there yet? (the biggest question and hardest to answer definitively)

- On the short side, the magnitude of covering in the High SI stocks would suggest it is closer to the end, but it is not clear that this holds true more broadly.

- The bigger risk seems to be whether the recent long selling that started in earnest this week has to persist for a while longer.

- Put together, in N. America, the 4wk active de-grossing has NOT yet reached even a 1z event and not nearly where things got to last March/April or in prior periods of strong de-grossing.

- Furthermore, with notional exposures effectively still near highs (and performance negative), it’s likely that gross leverage has gone up for many funds.

- With all this said, the fact that this is NOT occurring due to a broader weakening in the macro backdrop makes it harder to gauge how much further this should go.

In short, expect much more pain. No surprise there. What we find shocking however is that just yesterday another JPMorganite, Marko Kolanovic published a note urging clients to do just the opposite, BTFD, claiming that the WSB fiasco would be over soon and won't have any material impacts. In retrospect, we now know which report was meant for the "good" clients, and which was one the mindless fodder meant for general consumption.

https://ift.tt/2M5NbXe

from ZeroHedge News https://ift.tt/2M5NbXe

via IFTTT

0 comments

Post a Comment