Morgan Stanley: We Are Rethinking Our Preferences In The Credit Markets

By Vishwanath Tirupattur, global head of Quantitative Research at Morgan Stanley

It has been a rough ride for credit investors thus far this year. While total returns year-to-date have been disappointing across the board in corporate credit markets, US investment grade (IG) bonds have underperformed significantly, with total returns of -12% compared to -6% for US high yield (HY) and +0.4% for leveraged loans. Remember, returns to credit investors have both an interest rate and a credit risk component. It is worth noting that much of this underperformance is more attributable to moves in interest rates than to worries about the creditworthiness of underlying companies. While spreads have widened across credit markets, the effect of the dramatic move in interest rates has been more overwhelming – IG spreads have widened about 35bp since the beginning of the year, while underlying interest rates have moved four times as much. The significantly higher interest rate exposure (or longer duration, in bond market parlance) of IG bonds relative to other segments of the credit markets explains their underperformance.

Our credit strategists have been ahead of the curve on this front, preferring to take default risk over duration risk. In practical terms, that has translated into favoring lower-quality over longer-duration segments of the credit market – loans over HY over IG. This strategy has clearly worked thus far. However, (1) changes in the market pricing of the path of interest rates, (2) revisions in economic growth expectations as well as (3) concerns about the prospects for earnings growth all argue for rethinking our preferences in the credit markets.

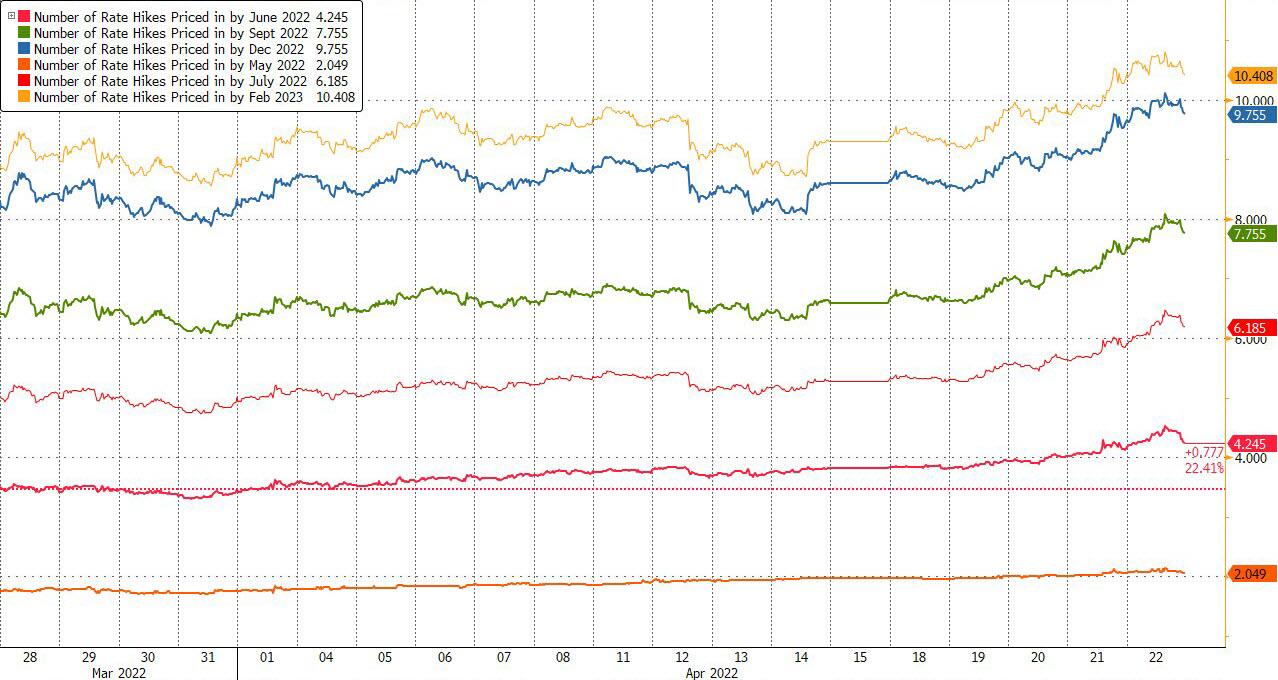

- First, interest rate markets already reflect aggressive rate hike expectations. Incoming data as well as hawkish rhetoric from Fed officials have contributed to ratcheting up terminal rate expectations, which currently stand at 3.40%, up from 1.57% at the beginning of the year. Markets are also pricing about eleven 25bp hikes between now and February 2023, and market expectations are clearly front-loaded, with 50bp hikes priced in for the next three FOMC meetings.

Regardless of whether this rates path is realized, it is clear that market pricing already reflects significantly hawkish expectations for monetary policy. For interest rate expectations to move up significantly from these levels, we need incoming inflation data to ratchet up, which runs counter to the expectations of our US economists. The takeaway for credit markets is that given what is in price, duration concerns are unlikely to intensify over the next few months. - Second, as our economists have noted, the combination of heightened geopolitical tensions and tightening monetary policy has increased the downside risks to the US growth outlook, and recession risks have risen. Our economists have lowered their forecast for real GDP growth in 2022 by 1pp to 3.0% on a 4Q/4Q basis, and our forecast for 2023 by 0.9pp to 2.1% 4Q/4Q. While corporate balance sheets are in good shape entering a front-loaded Fed hiking cycle, and low net leverage and record-high liquidity should help the median HY issuer to navigate near-term stresses, our concerns about tail cohorts have risen as they are vulnerable to both slower growth and structurally higher funding costs.

- Third, downside risks to earnings and earnings growth have emerged on multiple fronts. Our equity strategists anticipate multiple headwinds to earnings, including a payback in consumer demand, excess inventory build and demand destruction from sustained high prices. For the lowest-quality segments of the credit markets, this implies oncoming headwinds.

None of this means we are about to see a spike in defaults. Not at all. In-place fundamentals are indeed the strongest they have ever been going into a hiking cycle. Furthermore, taking into account the more 'termed-out' maturity profiles, conviction around the ability of US corporates to absorb the initial rate hikes remains high. Of the nearly US$2.9 trillion in index-eligible HY bonds and loans outstanding, only US$300 billion (about 10%) matures in the next three years.

That said, it is undeniable that for the lower-quality segments of the credit markets, risks have risen, and risk/reward calculus no longer favors default risk over duration risk. Thus, our credit strategists recommend moving up in quality, particularly in high yield credits – BBs over CCCs – and close out the preference for leveraged loans over HY bonds.

Within investment grade, the back-up in rates has created pockets of value in low dollar-price bonds. The average dollar price of the IG index has fallen sharply, with a significant proportion of bonds now trading at a substantial discount. Low dollar-price bonds are concentrated in relatively newer issuance as well, making them a tradeable part of the secondary market. While lower cash prices have been driven by higher rates, they provide a source of credit convexity as well.

Credit curves tend to bear-flatten into downturns, thus providing a cushion against MTM losses if growth weakens. With all-in yields around 4%, the cohort of low dollar-price, longer-duration bonds deserve careful reconsideration as a way to improve portfolio quality and liquidity.

https://ift.tt/1EoyJTG

from ZeroHedge News https://ift.tt/1EoyJTG

via IFTTT

0 comments

Post a Comment