Will $1 Trillion In Treasury Basis Trades Blow Up The Clearinghouses

By Russell Clark of Capital Flows and Asset Markets

Reading the excellent article by Brian Meehan of Bloomberg Intelligence, “Basis Trade Growth Is Massive”, I was reminded just how stupid clearinghouses really are. If you ever meet a head of a clearinghouse, I can assure it was not brains that got them to this key position in global finance.

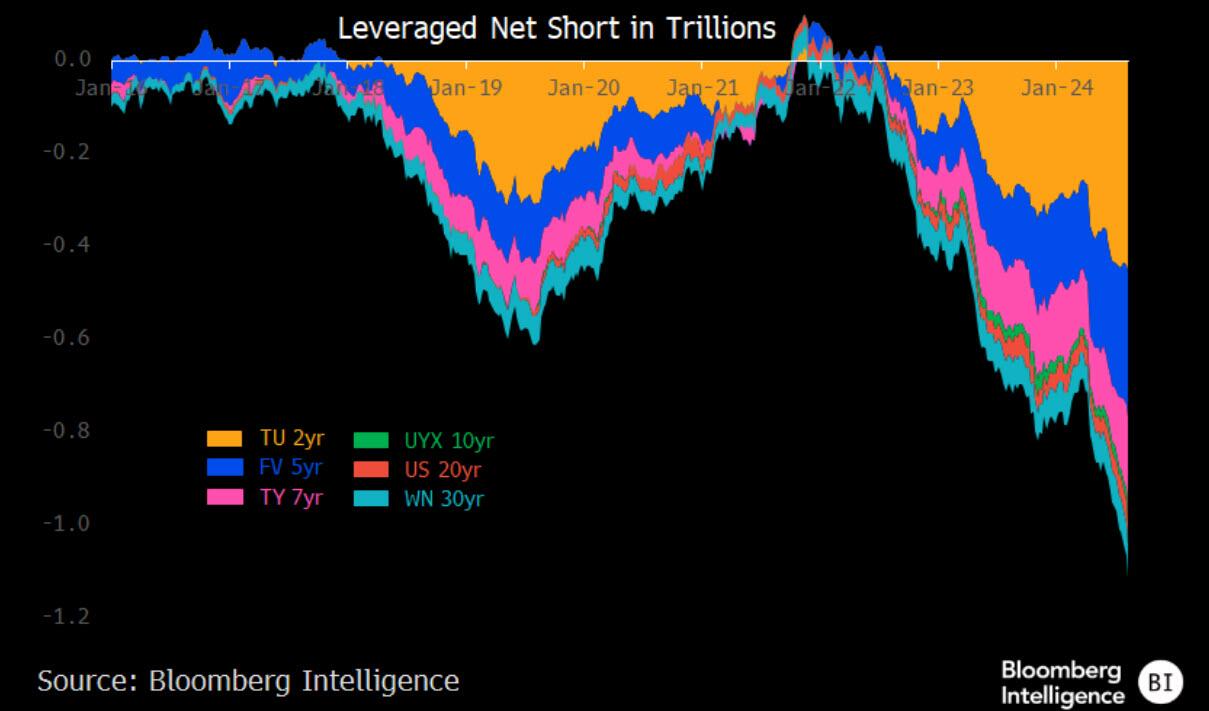

As the article points out, there is now a $1.1 trillion notional short position in US treasury futures. You should not read this as the market being bearish on treasuries. It is a levered trade to make a “risk free” return on the difference in price between off the run treasuries and treasury future positions. For every short position in the treasury futures, there should be a long position in the physical market.

The size of the trade has been large for awhile. The Federal Reserve took a look at it and thought it was not a problem (uh oh!). It has the same data as above, just that Bloomberg has provided an up to date estimate. In the post GFC world, much of this trade has migrated from prop desks at banks to hedge funds.

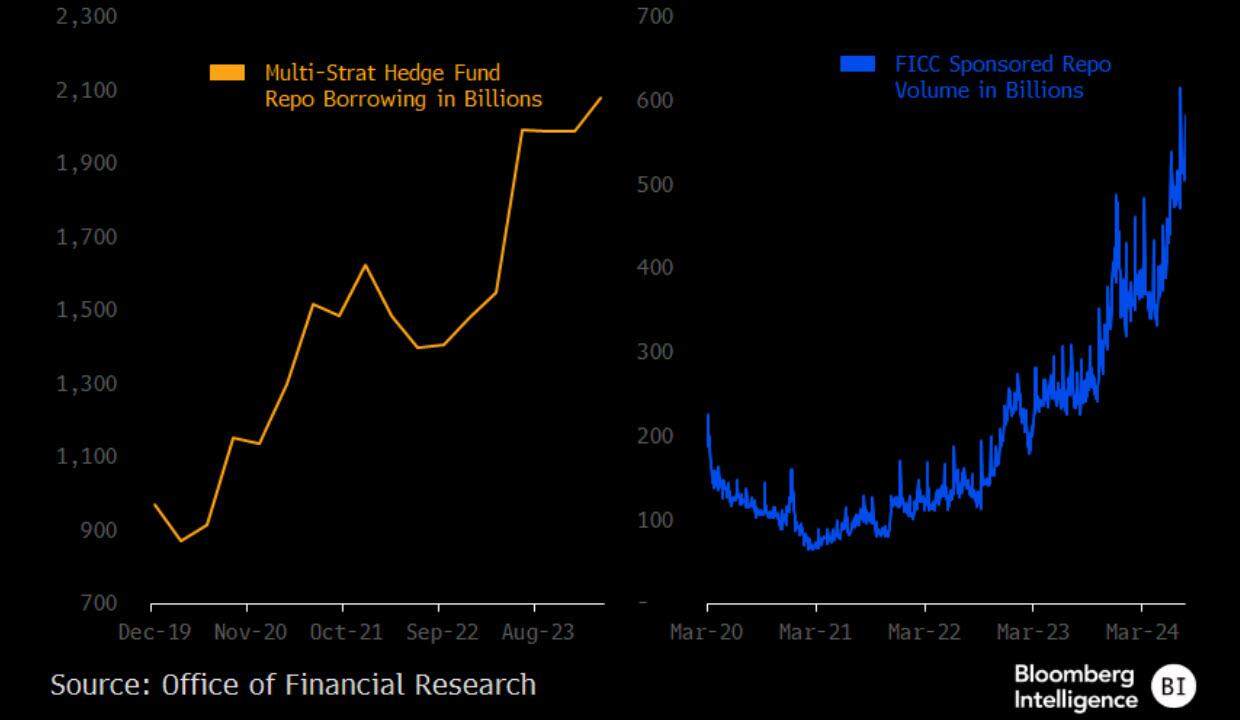

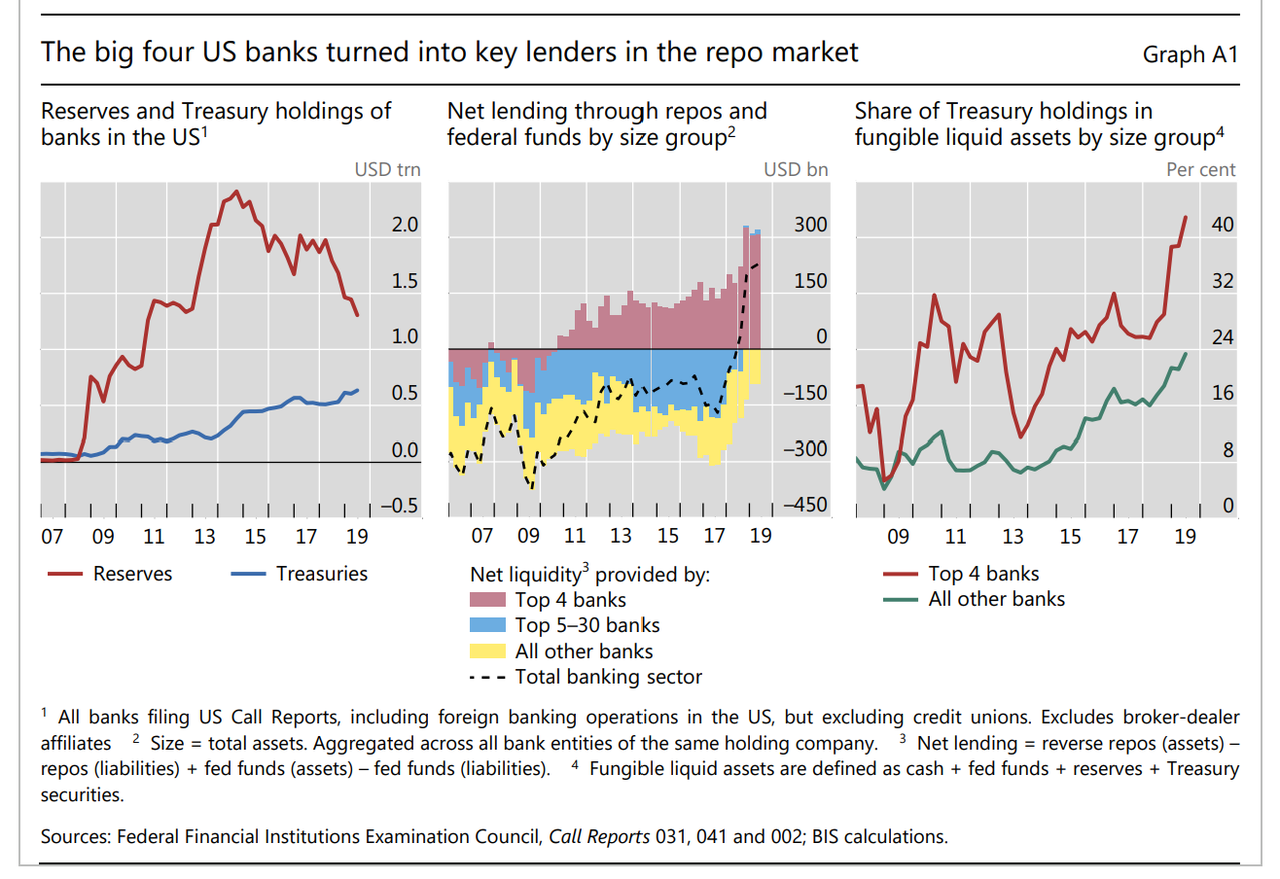

This is not a new phenomenon. BIS noted in 2019 reports that the Repo market has become bifurcated between banks and hedge funds. See dotted line in middle graph.

This is a natural by-product of how clearinghouses work. The clearinghouses at the centre of repo trading (LCH and CME) are only concerned with how quickly trades can be liquidated. As they tend to settle on a daily basis, and hedge funds and other asset managers need to settle constantly, they tend to allow trades to grow in size much more than when investment banks were at the centre of repo market.

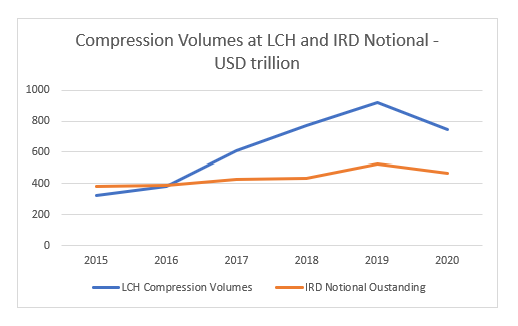

Clearinghouses cannot go bust. So they pursue policies to grow volumes as much as possible. One such policy is compression trades. This is where very similar interest rates products can be compressed into a single product to allow more leverage to be used. Below show that a multiple of outstanding notional is being compressed every year.

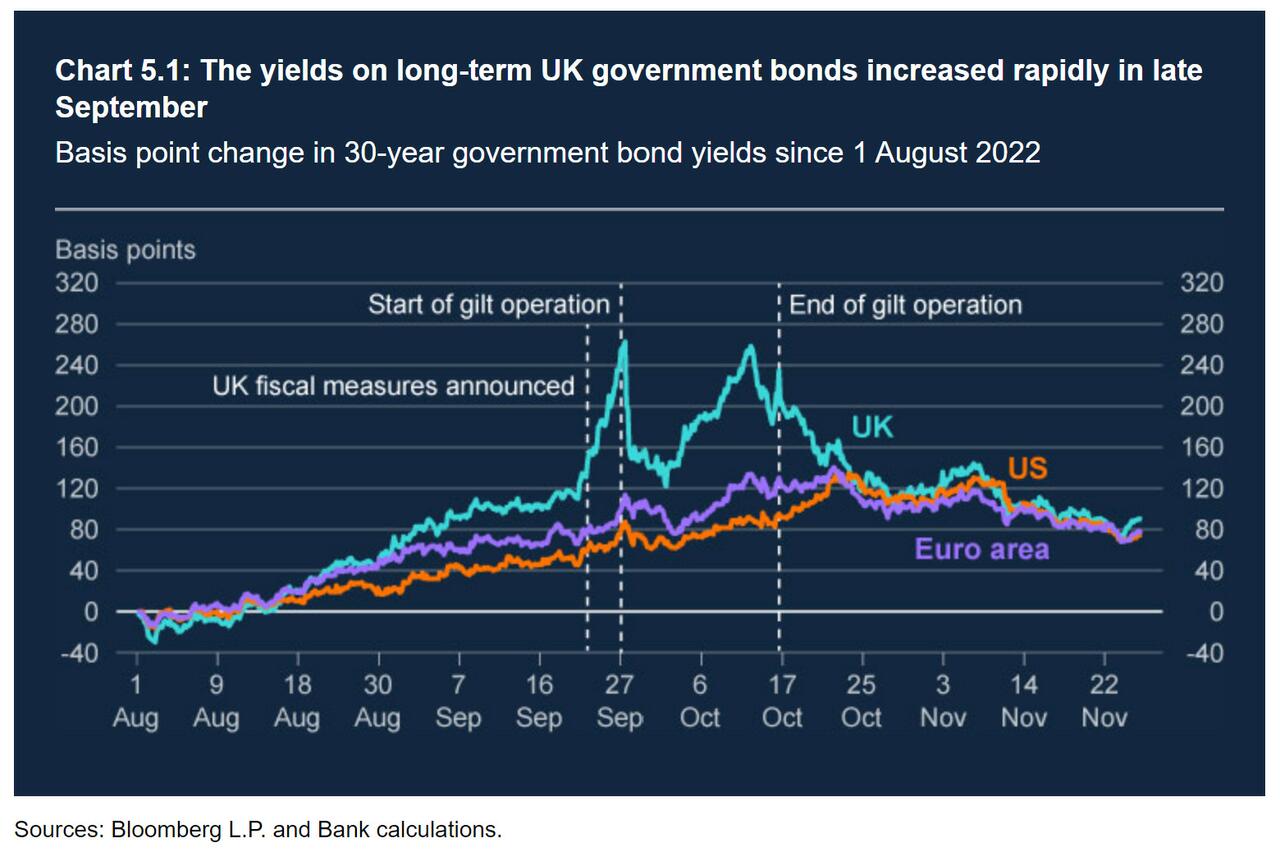

The problem is that when there is a shock in interest rate markets, then liquidity disappears and clearinghouse starts demanding more margin from all players, which then leads to spiraling weaker market. We saw just such a circumstance in the UK gilt market under the PM Truss. The sell off in gilts could only be contained by the Bank of England becoming a buyer of last resort.

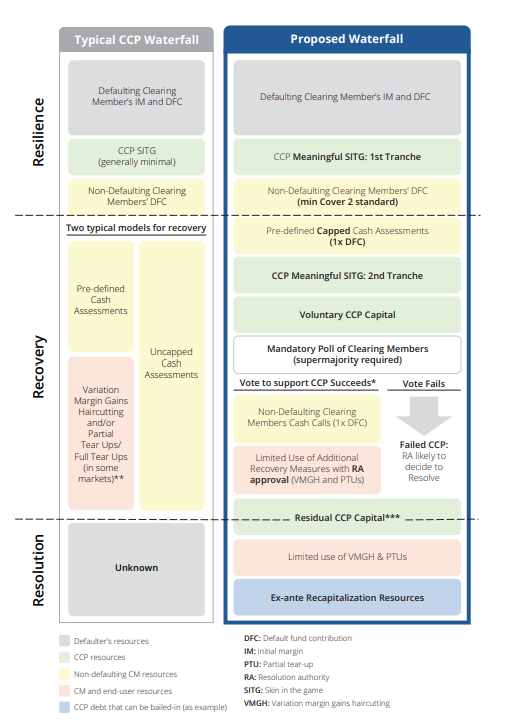

The big investment banks know that the clearinghouse misprice risk, which is why they suggested that they should take more financial risk in pricing, to incentivise them to do a better job. Regulators have so far ignored this advice. The proposed risk waterfall is presented below. More detail here. A close look at the proposed margin from the waterfall is a the ability to bankrupt CCPs. This has so far been rejected.

So how does this fit in with LTCM? Well LTCM focused on risk free arbitrage trades. The problem with most of the trades is that you need substantial leverage to make them work. Most banks would feel uncomfortable lending a hedge fund that much. The downfall of LTCM as it was told to me, and I did work at UBS, was that one day there were industry drinks and one trader mentioned how much business he was doing with LTCM - and another trader said, hang on a second, we are doing just as much business as well. The traders then worked out that LTCM had far more leverage than they had disclosed, and as they traders worked this out, sold their positions before LTCM could. This put downward pressure on their trades, eventually forcing them bankrupt and bringing about a bailout. In essence, LTCM became the market, and at that point, it was destroyed. But it only became so leveraged because it acted in secrecy.

Under the new clearinghouse system, no such subterfuge is necessary. The clearinghouse actively wants you to borrow as much as possible, as long as you meet the liquidity and volatility seen over the look back period - typically 10 years. The problem, as the details above show, is that the hedge funds are all in. So are retail investors. Shares outstanding in TLT has skyrocketed.

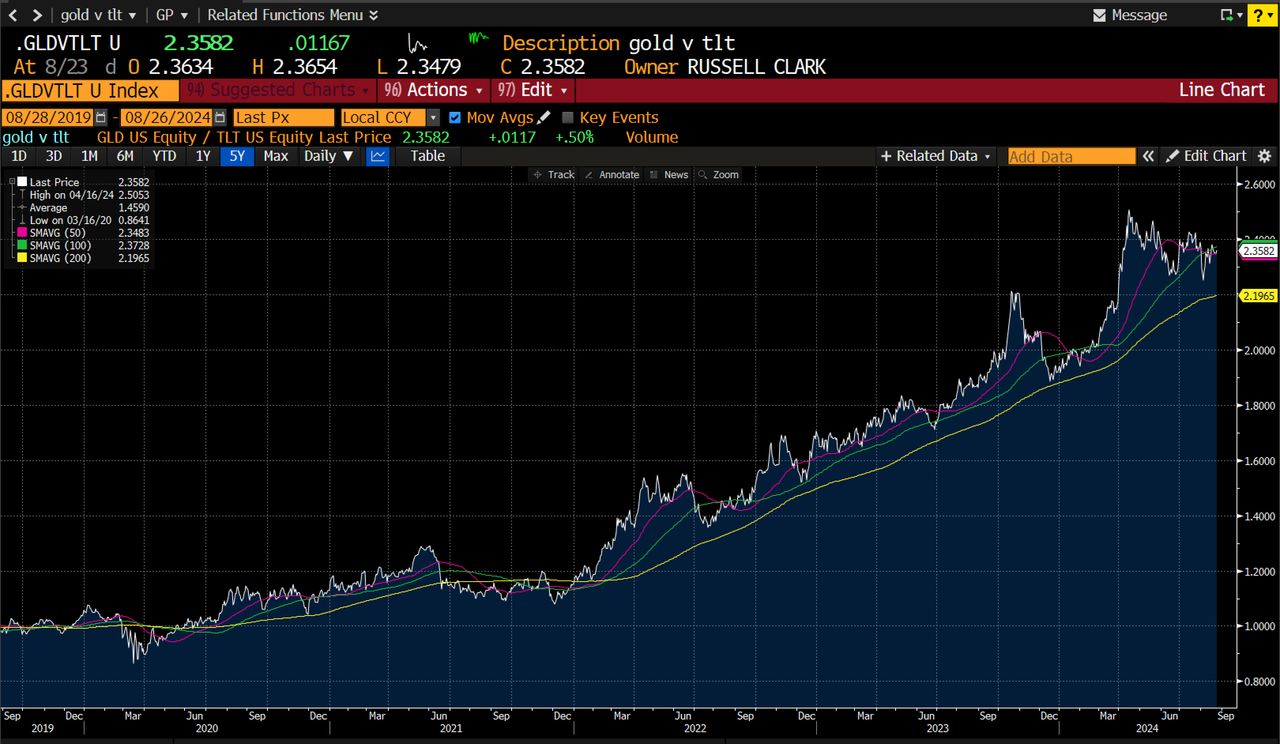

So what could go wrong? Well in the US, after the presidential election is out of the way, you could expect inflationary policies to be announced (higher minimum wage, more tariffs, more stimulus). This leads to inflation expectations rising. Physical treasuries are held in ETFs like TLT, which probably see redemptions. Treasuries fall, basis trade widen, margin calls are issued, which leads to more selling of treasuries, and more basis widening, until the Fed steps into buy treasuries. This seems likely to me: a long GLD/TLT trade should do well in that environment. Having gone sideways for a few months, a move higher looks overdue.

The clearinghouse reform is failed reform - but it will take a crisis to change. Maybe this will be the one.

https://ift.tt/qQYjiAr

from ZeroHedge News https://ift.tt/qQYjiAr

via IFTTT

0 comments

Post a Comment