A Former SAC PM's Advice To Traders: "Sit Tight, Be Right"

By Nicholas Colas, co-founder of DataTrek Research

Today’s story is about patience. Whether you are trading or investing, 2022 will require more calm thoughtfulness than any year in recent memory. History shows that as crises fade into the rearview mirror, market volatility (and the opportunities it brings) declines. Also, there is a real tug of war now between fundamentals and Fed policy. Lastly, the best places to make money in stocks (cyclicals, in our view) are volatile and rarely well-structured industries or companies. Bottom line: 2022 is a “measure twice, cut one” sort of year.

* * *

Strange as it may sound, I learned most of what I know today on this topic while working for Steve Cohen at the old SAC Capital. Yes, it was a (very) fast money trading shop. And yes, Steve’s trading process demanded absolute adherence to a specific set of rules and mindset. Price action, not opinion or emotion, defined right and wrong.

But SAC is also where I learned the old trader’s saying, “Sit tight, be right”. If your process is sound, from idea generation to risk management and exit discipline, then patience determines profitability. Simply put, big trades often take time to work.

Everyone at SAC had their own approach to cultivating patience, which in the context of the firm’s trading bent often meant simply distracting themselves rather than staring at their daily P&L. Steve might invite his family to lunch and actually take an hour off the desk with them if he was worried about being shaken out of a large position intraday. Other traders occupied their time by planning where to go for lunch or dinner (traders think about food a lot). As for me, I would spend hours on a forward calendar of catalysts that might offer new trading ideas (analysts think about data a lot).

Many years after leaving SAC, a hedge fund performance analytics firm showed me some research that put the importance of patience into even starker relief. Hedge funds, as a whole, are good at finding winning ideas. Their performance would often be better, however, if they held those ideas longer. Academic work on institutional investor (long only and hedge funds) behavior shows that the problem is structural. So much of money management marketing is pitching new ideas to gather assets that “old ideas” (those currently in the portfolio) get crowded out too early in order to take stakes in new names.

I bring all this up because 2022 feels very much like a year where patience will be the defining factor when it comes to outperformance. Whether you are bullish or bearish on a market, sector, investment theme or individual idea, it will take longer to get paid for your point of view than the last several years.

Three reasons I think that’s true:

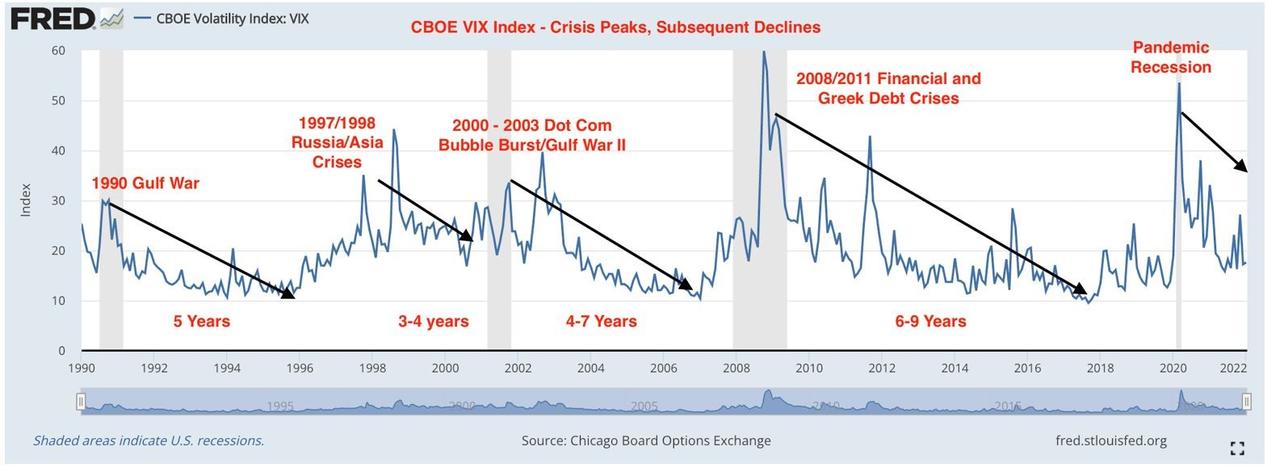

1: US equity market volatility historically declines in the years after a shock. The chart below shows the CBOE VIX Index back to 1990. As highlighted, there have been 4 notable VIX spikes since then. In each case volatility declined for several (3-9) years thereafter. In March 2022 we will be 2 full years into the post-pandemic market recovery. Volatility has already been declining. The VIX today is only 20, for example, even with the selloff and January’s choppy action.

2: There are times when fundamentals (i.e., corporate earnings) matter and then there are times when changes in macro conditions matter more.

- At the bottom in March 2020, macro mattered; fiscal and monetary policy supported the US economy during the Pandemic Crisis.

- From Q2 2020 to Q4 2021, US corporate earnings took over the market narrative. The S&P 500 earned 23 percent more in 2021 than it had pre-pandemic. Wall Street analysts were slow to acknowledge that fact, which allowed for a long series of earnings beats.

- We are now entering a period where the Federal Reserve will engage in a never-before-seen experiment: raising interest rates off zero and reducing the size of its balance sheet in the same year.

All this sets up 2022 as a tug of war between the relative certainty of strong corporate earnings and the absolute unknown effect of novel Fed policy. As we outlined earlier this week, the setup here reminds us a lot of 1994. Back then, the Fed embarked on a surprise series of aggressive rate hikes and investors simply had no idea what that would do to the US economy. Now, Fed communication may be better - they have telegraphed liftoff and runoff quite clearly – but the market is still left wondering what results will come from their decisions.

3: The sectors that have been working – and we still like – are not what one would call easy stories to love. Large cap Financials (+6 pct YTD) are cheap but face structural challenges from venture capital funded FinTech disruptors. Large cap Energy (+14 pct YTD) is an ESG nightmare, and you have to believe (as we do) that traditional carbon-based energy has several years of new demand highs ahead of it. Airlines (+7 pct YTD), which Jessica just highlighted earlier this week, are no one’s idea of a stable or well-structured industry.

As much as we like cyclical sectors, we know there will be sudden and violent rotations out of them through 2022. They have a tailwind but owning them in 2022 is not the same as holding Big Tech in 2020 – 2021. If nothing else, their competitive positions are not as strong. In trading parlance, you are “renting” these names rather than buying a forever home for capital.

Summing up: 2022 is set to bring us lower average US equity volatility, a see-saw dynamic between fundamentals and Fed policy, and rotation into cyclical (and often volatile) sectors with little to offer besides earnings leverage. It will be a year for patience and, just importantly, discipline. Sit tight, be right.

https://ift.tt/3FBmwHg

from ZeroHedge News https://ift.tt/3FBmwHg

via IFTTT

0 comments

Post a Comment