How Goldman Is Convincing Its Clients Not To Freak Out About Fed Rate Hikes

Rate hikes are now just right around the corner and traders are freaking out, but not so fast according to Goldman.

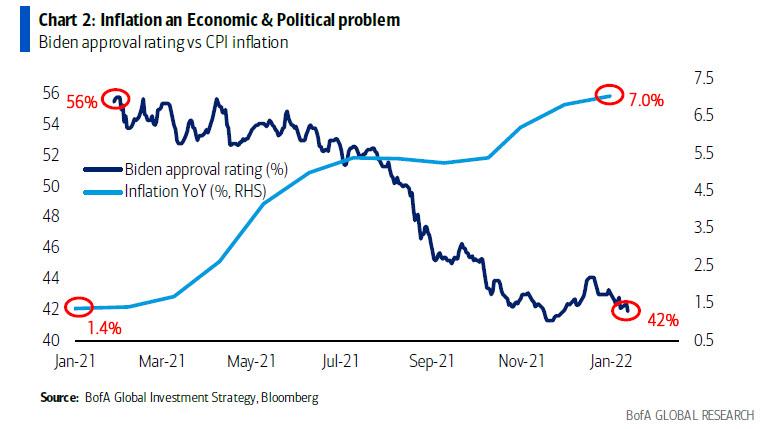

Following the FOMC meeting in mid-December, and especially last week's FOMC minutes and the subsequent jawboning by various Fed officials,, it has become clear that the Fed will not only double the pace of tapering but also signaled three hikes in 2022. As a result, virtually all sell-side economists - even stern holdouts such as Morgan Stanley and Bank of America - have raised their forecast from three hikes in 2022 to four – with the first hike now expected to occur in March. Their forecast reflects the greater sense of urgency on behalf of FOMC participants towards quelling inflation, which rose to a four-decade high of 7% as measured by the latest year/year CPI. Why this urgency? Because as one can imagine, Biden was very clear in what Powell's mandate was when he was renominated: "crush inflation as it is crushing my approval ratings", because as BofA's Michael Hartnett noted on Friday, "US inflation is up from 1.4% to 7.0%, while Biden's approval rating is down from 56% to 42% past 12 months."

But why is the Fed rushing to hike when a growing chorus of economists now agrees with us that the Fed is hiking right into a recession (or alternatively, hiking to create a recession) an observation that was validated by Friday's dismal retail sales data... and even without validation, the endgame is clear: as David Rosenberg noted recently, every time the US has had 5%+ inflation, it ended in recession.

Inflation is 7% and the last time this happened, we had a double-dip recession. Prior to the pandemic, 5%+ inflation presaged all seven recessions over the past sixty years. Les jeux sont faits. #Economy #Inflation #DavidRosenberg #RosenbergResearch #RRMacro pic.twitter.com/ZXXjCARL9D

— David Rosenberg (@EconguyRosie) January 13, 2022

Well, according to Goldman's David Kostin, the unprecedented strength of the labor market has made the Fed more sensitive to high inflation and less sensitive to slowing growth. Alongside rising inflation, the Fed has also cited strong employment data as a catalyst for earlier liftoff and balance sheet reduction. The unemployment rate now stands at 3.9%, falling slightly below the FOMC’s 4.0% median estimate of its long-term level (although looking ahead, Kostin notes that surveys of workers and businesses indicate wage growth is expected to slow to about 4% this year).

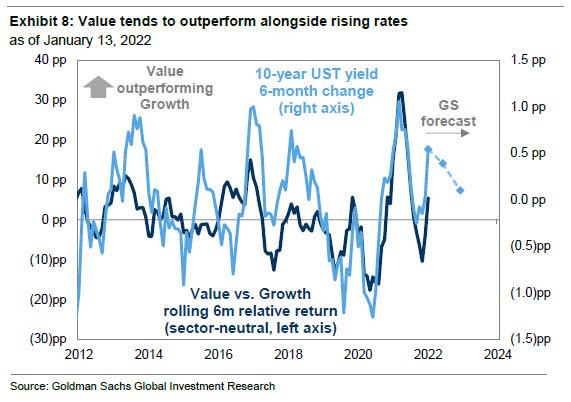

To be sure, the market already reflects this and real and nominal rates have both jumped in anticipation of the upcoming tightening cycle. Since the December FOMC meeting, the 10-year US Treasury yield has surged by 26 bp to 1.77%. Consistent with historical experience, equities have struggled amid this rapid rise in yields, and the fastest-growing and longest-duration pockets of the market - i.e., the biggest bubbles such as profiless tech names, the ARKK ETFs, SPACs and so on - have de-rated most.

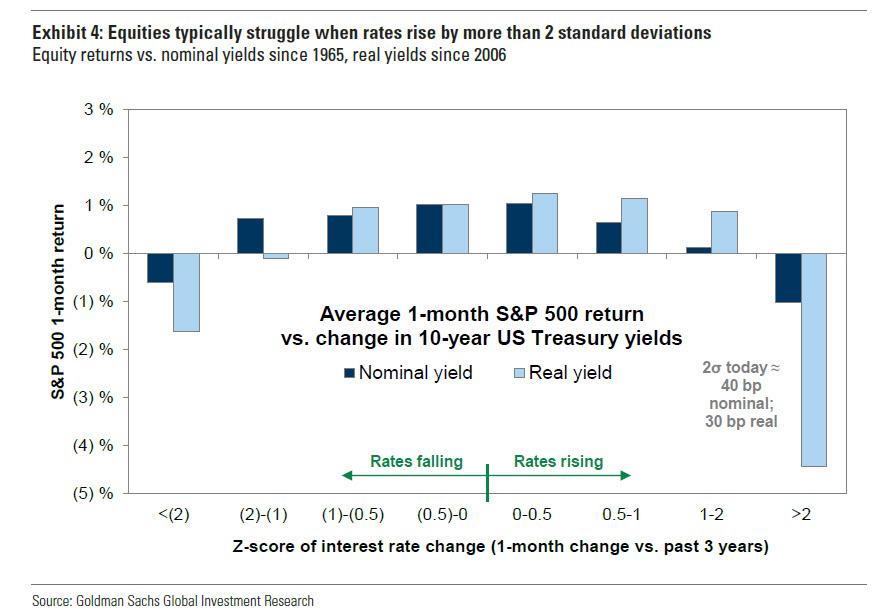

As a quick aside, perhaps the main reason for the equity puke in the past two weeks is not so much the jump in absolute yield in the past month, but the speed of the move. As Goldman showed in a separate report earlier this week (also available to professional subs), regardless of the level of interest rates, equities react poorly to sharp changes in the interest rate environment, and the past week has been no exception: "Historically, equity prices have declined when interest rates rose by two standard deviations or more. This is true for both nominal and real interest rates across both weekly and monthly periods. The two standard deviation threshold was exceeded on both horizons last week, and the accompanying equity weakness followed the usual historical pattern."

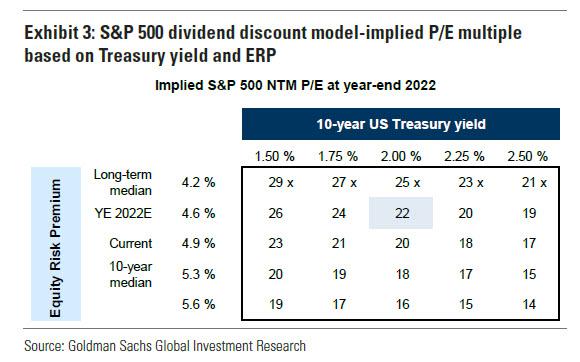

But while that may explain short-term moves, surely higher rates will lead to longer-term weakness no matter what. And while the answer is yes, the next table shows the sensitivity of the S&P 500 forward P/E multiple to various interest rate and ERP scenarios. Goldman's interest rate strategists forecast a continued rise in real interest rates that will lift the nominal 10-year Treasury yield to 2% by year-end 2022 (more below), however they also expect the ERP to compress modestly from current levels as the pandemic recovery continues and economic policy uncertainty surrounding potential reconciliation legislation passes. In this base case scenario, the S&P 500 P/E multiple would remain roughly flat this year, allowing earnings growth to lift the index price level. But, if the ERP were to rise to its 10-year median and the Treasury yield rises to 2.25%, the P/E multiple would compress by roughly 15% to 17x, and not even Goldman can spin that as positive.

In any case, as Kostin writes in his latest Weekly Kickstart, market pricing and client conversations indicate investors are braced for a string of hikes in 2022, and as a result, questions from Goldman clients during the past two weeks "have focused on the relationship between equities and interest rates, indicating that the hawkish FOMC pivot is being actively assessed by equity investors." Moreover, the overnight index swap (OIS) market is currently pricing 3.6 rate hikes in 2022 and 2.6 in 2023, just below the 4 and 3 hikes, respectively, that Goldman forecasts (spoiler alert: the total number of rate hikes will be far less once stocks crash).

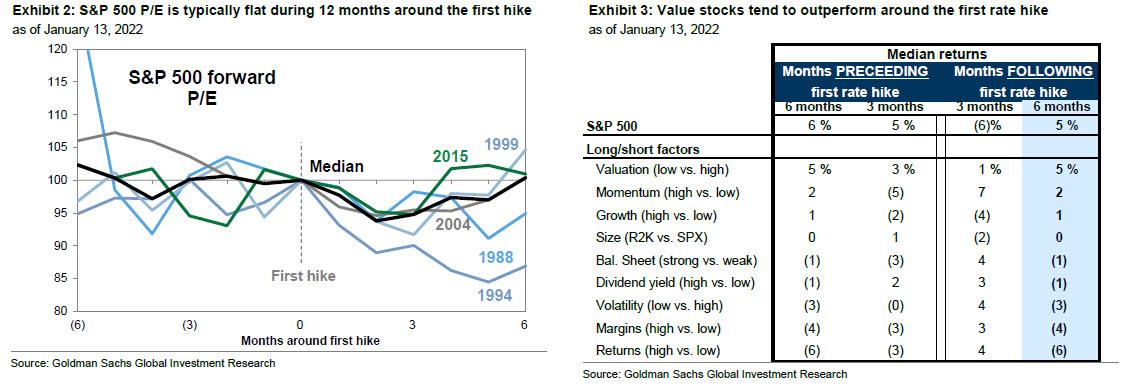

And this is where Goldman enters the bullish spin cycle, because the bank makes much more money when its clients buy (only to sell in the future), than selling now. So to ease client concerns that the bottom is about to fall off the market, Kostin writes that "historically" (because clearly we have had many "historical examples" when the Fed's balance sheet was 45% of US GDP), the S&P 500 index has been resilient around the start of Fed hiking cycles, noting that "although the index has returned -6% on average during the three months following the first hike of recent cycles, the weakness has been short-lived as returns average +5% during the six months following the first hike." Moreover, as Goldman shows in exhibit 3, the S&P 500 P/E is typically flat during the 12 months around the first hike.

Drilling down into segments, Goldman notes that cyclical sectors and Value stocks outperform around the first Fed hike. The reason: the start of Fed hiking cycles (usually) tends to coincide with a strong economy, which can help to lift cyclical sectors (Materials, Industrials, Energy). However, this time around it is starting as the economy is rapidly slowing yet inflation remains stubborn due to supply-chain blockages, and as such anything Goldman suggests you should do, please ignore it.

Which is probably also true for factors. According to Kostin, at the factor level, Value stocks tend to outperform in the months before and after the first hike: "High quality factors (e.g., high margins, strong balance sheets) underperform in the strong economic environment preceding hikes and outperform in the months following the initial rate increase. Growth is the worst performing factor in the 6 months around the first hike." Here too, we would flip this 180 degrees because the Fed is now hiking to effectively start a recession (or as the US is already en route to one), so what one should be selling is value while buying growth ahead of the next rate cuts/QE which are now just a matter of time.

Next, Kostin brings out the heavy artillery and urges his skittish clients to consider that "surprisingly" equities have historically performed well alongside rising expectations for Fed hikes. Here, the bank examines the six-month periods since 2004 when OIS pricing of the 5-year-ahead fed funds rate increased by 25 bps, excluding episodes when the Fed was cutting rates.

During these episodes, nominal 10Y yields typically rose by 52 bps with roughly even contributions from real yields and breakevens. Despite this, the S&P 500 returned 9% (vs. its unconditional 6-month average of 5%). Higher earnings expectations drove these rallies as increases in fed funds pricing usually coincided with improving expectations for economic growth. However, as we have repeatedly warned and as even Kostin concedes, "the current inflation-led hiking cycle may prove more challenging for equities." We are not sure this will boost the confidence level of Goldman clients who are on the fence to just BTFD...

After the initial stage, when markets price more eventual rate hikes, cyclical sectors typically outperform while bond proxies lagged according to Goldman. Industrials, Consumer Discretionary, and Materials outperform the S&P 500 on average during these episodes, with financials especially sensitive to the long-term interest rate outlook and also outperforming. Meanwhile, bond proxy sectors such as Utilities and Consumer Staples underperformed sharply.

As noted above, value has typically outperformed alongside rising market expectations for Fed hiking, but only in cases when the the hiking cycle was led by growth expectations, not to crush inflation, so this time one can argue that everything will be flipped. And while traditionally, small-caps also outperformed, as “quality” factors underperformed, the recent weakness in small-caps confirms that this is anything but an ordinary rate hike cycle.

Curiously, even in his bullish pitch to clients, Kostin - perhaps hoping to preserve some credibility- admits that this is not a typical rate hike cycle, and the recent hawkish pivot has been driven not by "improving growth expectations but by inflation risks" yet even so Goldman's economists expect growth to remain above-trend in 2022 because, of course, what else can they do: start sounding like Zero Hedge and admit that the Fed is hiking into a recession.

And indeed, Kostin admits that "fading expectations for fiscal stimulus and the hit from Omicron have led our economists to downgrade their growth outlook in recent weeks" however - perhaps unwilling to piss off Biden too much - they still forecast 3.4% GDP growth this year, a stepdown from the 5-6% pace in 2021 but still above their 1.75% estimate of trend growth. Translation: the US will be in a recession by the midterms, courtesy of the Fed.

So after all that, if Goldman clients aren't running for the hills, maybe the will BTFD after all, and for them, Kostin writes that investors "should balance their exposures to Growth and Value" as Goldman's rates strategists expect yields will continue to rise, a dynamic that should support Value over Growth, unless of course we enter stagflation at which point all is lost (incidentally, as noted last week, Goldman expects nominal 10-year yield to hit 2.0% by year-end 2022 (with real rates rising to -0.70% almost where they are now) and 2.3% by the end of 2023).

From a growth perspective, Goldman economists expect the waning of the Omicron wave to lift GDP growth from 2% in 1Q to 3% in 2Q, supporting Value stocks. But they expect growth will slow to a 2% pace by 4Q 2022, the type of environment that generally supports Growth stocks. Translation: yes, growth stocks are getting crushed now, but as soon as the current whisper of a recession/stagflation becomes a chorus, watch as "growth stocks" (i.e., the bubble/bitcoin baskets) explode higher and surpass their previous all-time highs.

In short, Goldman's current recommended sector overweights reflect a barbell of Growth and Value:

- Info Tech remains the bank's long-standing overweight due to its secular growth and strong profit margins.

- Financials should benefit from rising interest rates

- Health Care combines secular growth qualities with a deep relative valuation discount.

Finally, from a thematic perspective, Goldman continues to recommend investors own highly profitable growth stocks relative to growth stocks with low or no profitability. To this, all we can add is that with low growth stocks having been absolutely nuked by now, the highest convexity when the recessionary turn comes, will be precisely in the no profitability growth sector, which will double in no time once the coming recession/easing cycle becomes the dominant narrative.

https://ift.tt/33fRw2E

from ZeroHedge News https://ift.tt/33fRw2E

via IFTTT

0 comments

Post a Comment