Jim Bianco Says This Is QE, Like Y2K

Authored by Mike Shedlock via MishTalk,

In contrast to Hussman, Jim Bianco, at Bianco Research says the Fed's repo actions are QE.

Earlier today I posted, Hussman Sides with Powell: It's Not QE4.

If Hussman convinced you the Fed was not conducting QE, I will give you a chance to change your mind again.

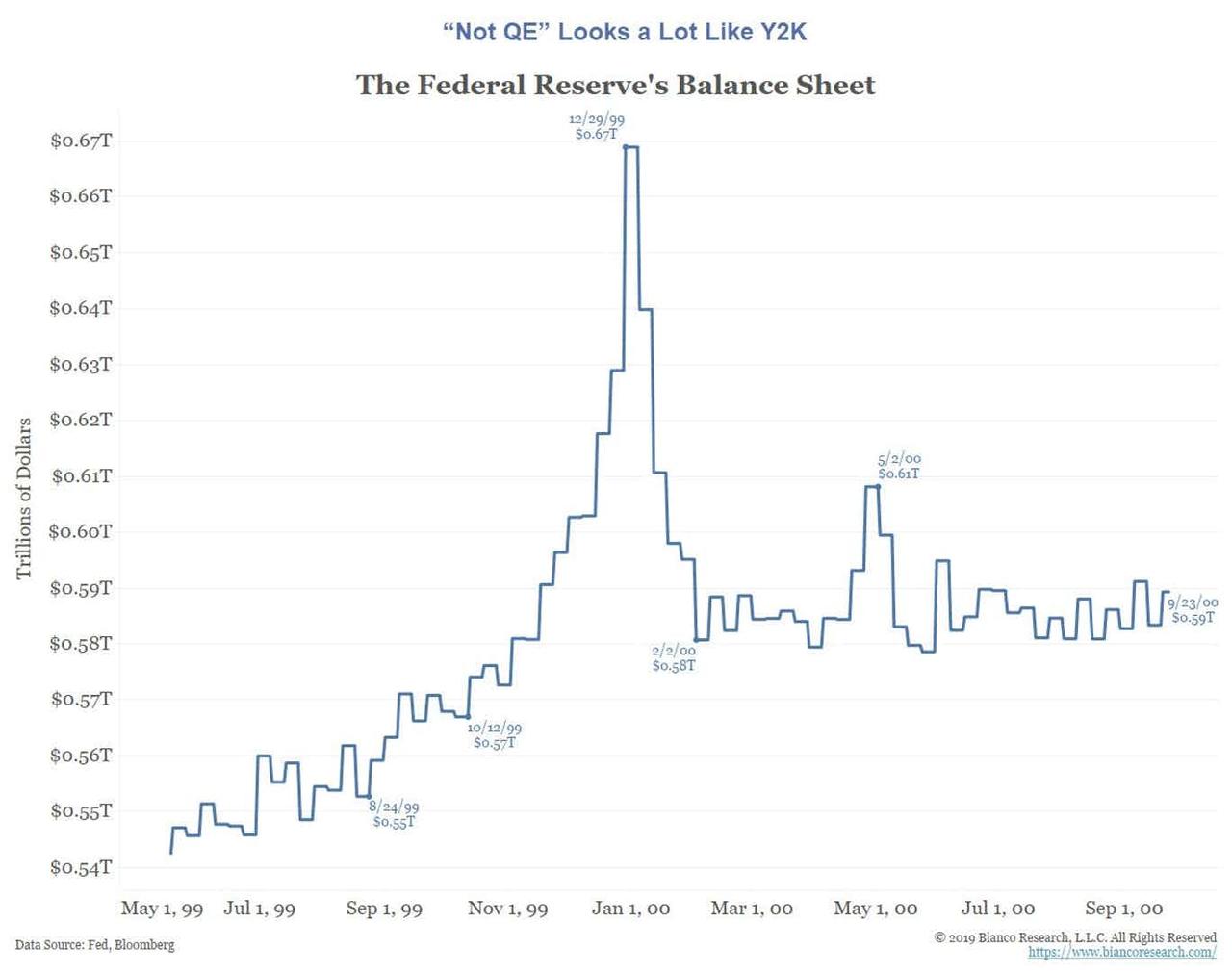

“Not QE” Looks a Lot Like Y2K

This is a guest post by permission from Jim Bianco

Jim Bianco at Bianco Research says “Not QE” Looks a Lot Like Y2K

We would argue the special lending facility that started in late 1999 to support the feared Y2K computer glitch offers a historical analogy to the current period.

Stories 20 years ago sound like they are describing what is happening today:

Dow Jones News Service – (December 28, 1999) CASH IS FLOWING LIKE CHAMPAGNE FOR Y2K

The volume of cash that the Federal Reserve has temporarily given to banks to avert potential Year 2000 strains is rising to dizzying levels. Including nearly $20 billion it gave to the banking system in the form of term “repurchase” agreements Monday, the Fed has almost $100 billion in hard currency loans outstanding to banks. That’s the most money lent out through repurchase agreements ever, said Peter Bakstansky, spokesman for the New York Federal Reserve. For some perspective, the Fed had $23 billion in outstanding “repos” in December 1998, and around $9 billion in December 1997.

The Y2K special lending facility had a similar effect on the Fed’s balance sheet. It was also done for “plumbing reasons.”

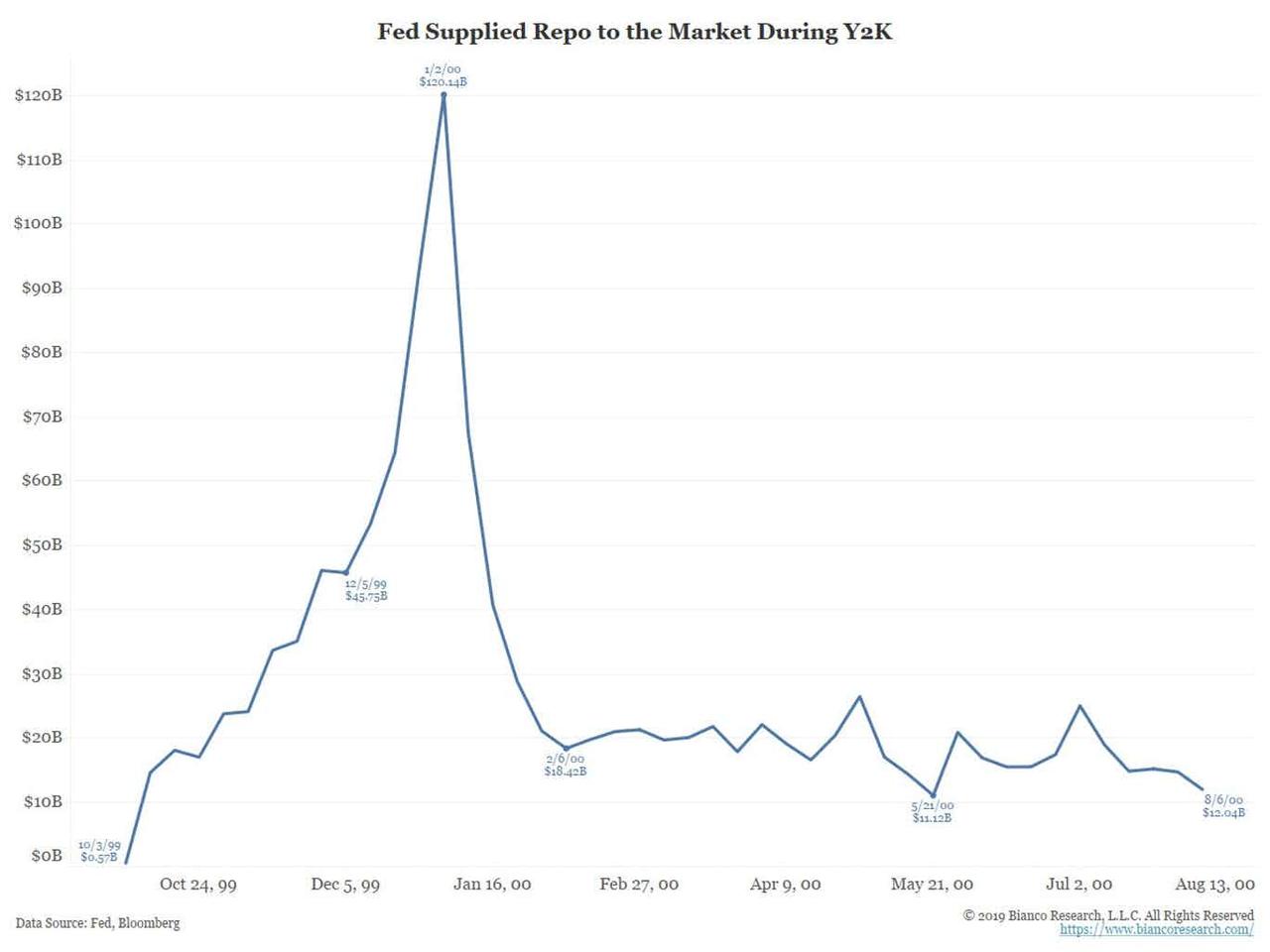

And, as the [Champagne] story points out, the Fed supplied record amounts of repo never before seen at the time.

Fed Supplied Repo to the Market During Y2K

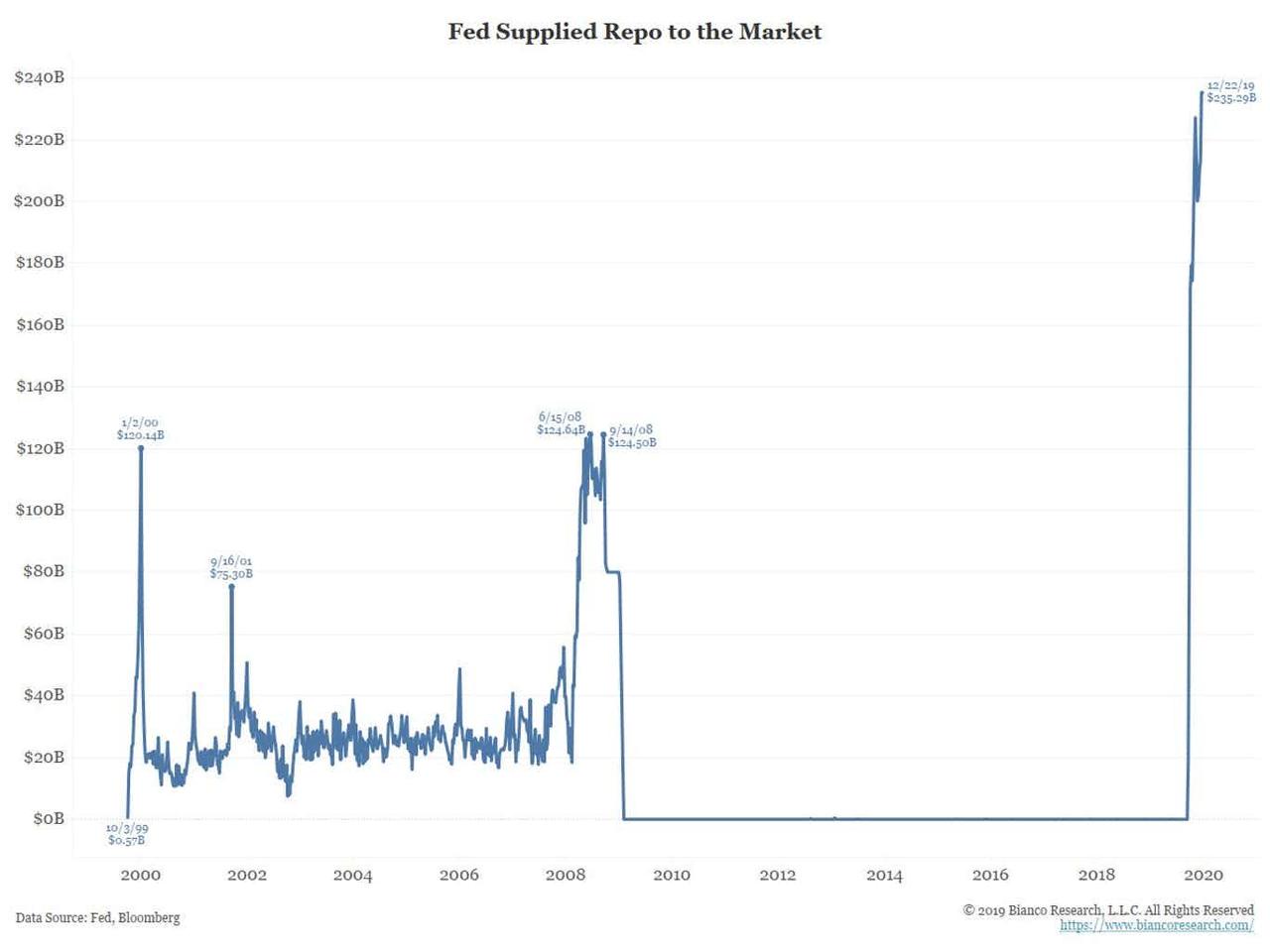

In fact, the amount of repo the Fed supplied in late 1999 was significantly more than on 9/11 and on par with the support offered during the financial crisis.

It was not until September 2019 that the Fed’s repo operations finally saw a meaningfully higher level.

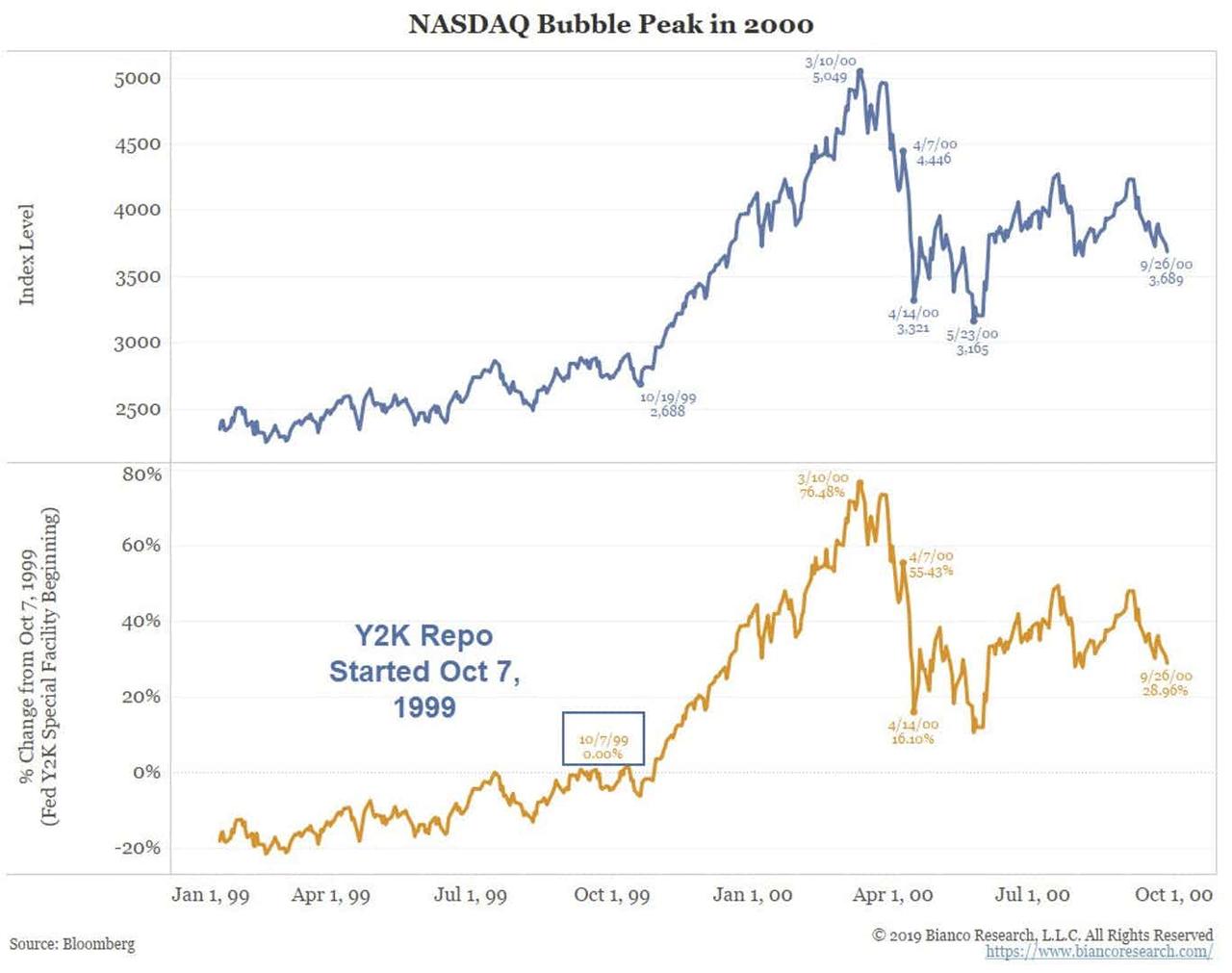

Y2K Special Lending Starter Oct 7, 1999

Note that the Y2K special lending facility ran from October 7, 1999, to April 7, 2000. And what did stocks do during this period? Below is the NASDAQ.

The Nasdaq went on a tear rarely seen in American finance, starting literally the day the Fed opened its Y2K lending facility. It crashed 25% the week the facility closed (April 7, to April 14, 2000).

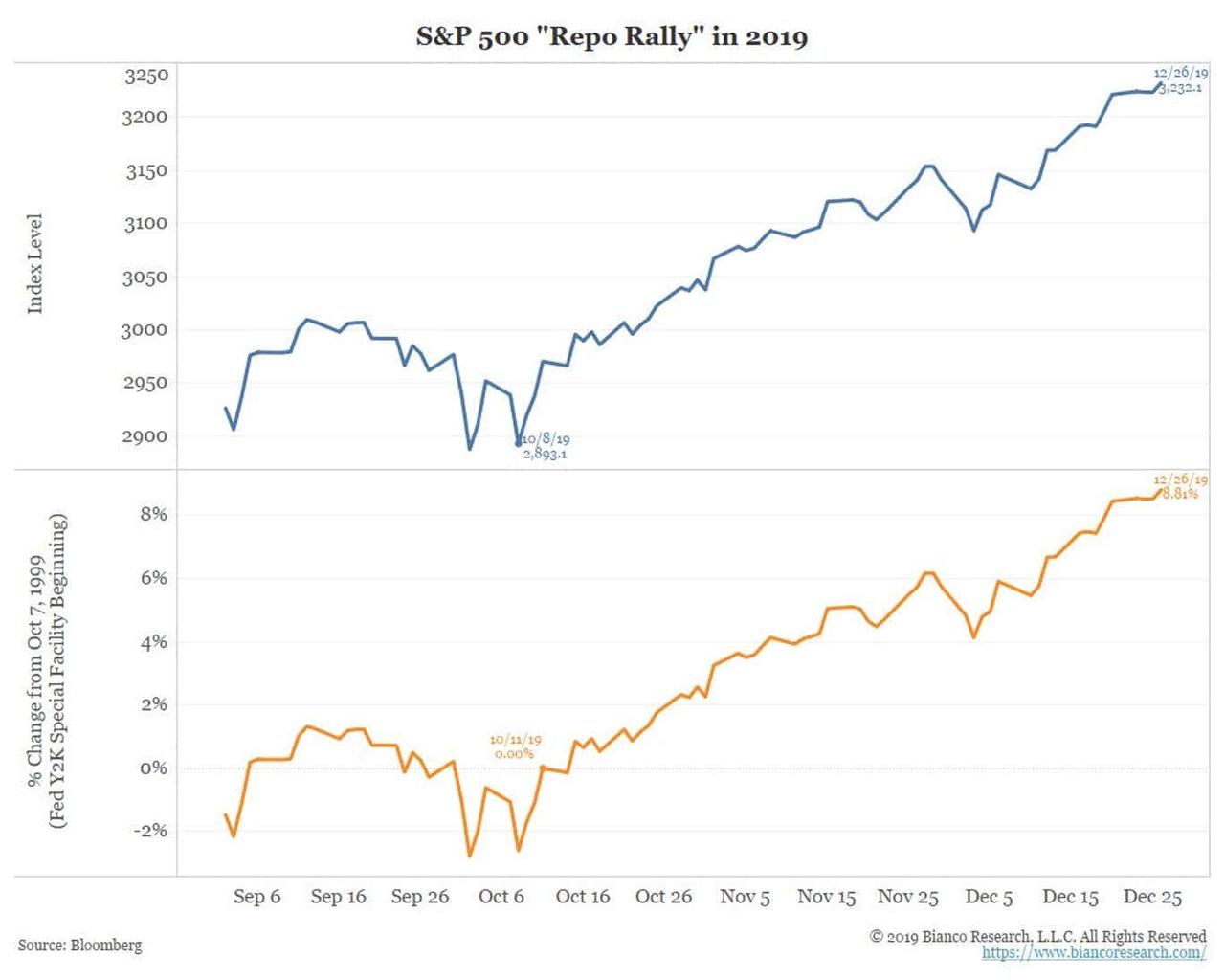

2019 Repo Rally

How does this analogy currently compare? The Fed announced it would start buying T-bills on October 11, 2019. Stocks have gone a tear since (clearly the magnitude of the NASDAQ returns above were larger, but the timing of the bottom in each case is similar).

Conclusion

There is no such thing as a one-factor model to explain the stock market. Metrics such as the Fed’s balance sheet, repo, etc. cannot explain the stock market’s movements in isolation.

That said, when the Fed injects money, funds generally flow to the best-returning market. During the financial crisis, it was the bond market. Today, as was the case in 1999, it is the stock market.

There have been indications of how important the Fed’s balance sheet is to financial flows in the recent past.

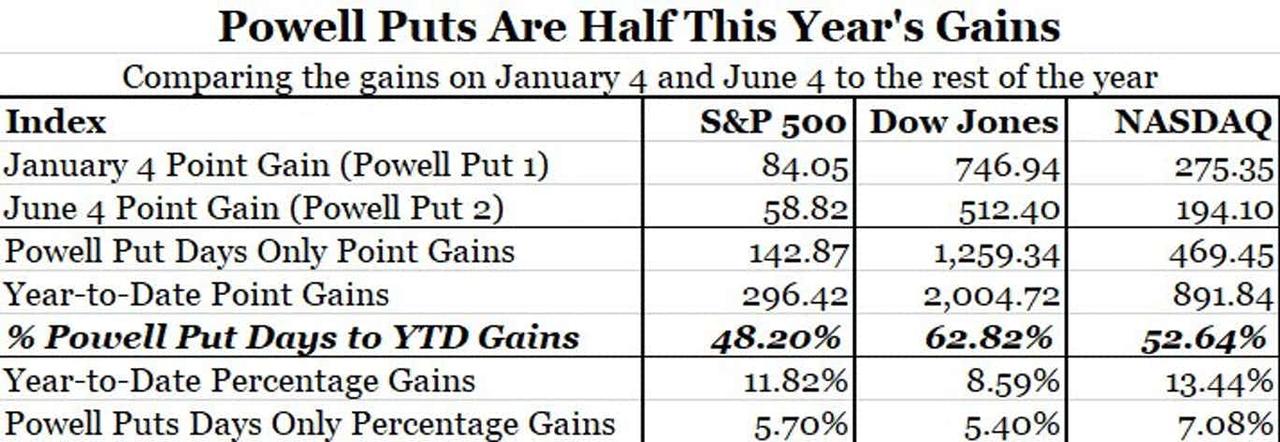

During the Fed’s Dec 19, 2018 presser, the stock market collapsed when Powell said the balance sheet was on “automatic pilot.” It soared almost a 1,000 DJIA points on January 4 when he said the Fed would be “patient and flexible.” On June 4, when he said the Fed would “act as appropriate,” stocks continued higher. Again, no single measure can predict the stock market, but these were clear signs that the size of the Fed’s balance sheet and policy matter.

The following table highlights this. Through June 5, half the gains to that point came on the two days Powell commented on policy.

Powell PUTs are Half This Year's Gains

Another 9% of the stock market’s gains came after October 11, when the Fed announced its T-bill purchase problem. So, a big part of this year nearly 30% stock market gain has come on the heels of Fed moves, much like last year’s 20% decline was coincident with the Fed’s hawkish rhetoric.

Given all this, the big question is, what happens when the Fed ends T-bill purchases and repo support in Q2 (the current projected end date)? Will the April 2000 analogy apply?

* * *

The above was a guest post generously provided by James Bianco.

It was part of his proprietary research.

I asked Bianco if he would make that post public, and he did.

Free Trial

Those wishing a Free Trial to Bianco Research can click on that link.

Final Thought

Although the point about Y2K is clear, I asked Jim explicitly if this was QE.

He replied:

By saying it is “Not QE” they are arguing it is not impacting financial markets. By detailing the Y2K “Not QE” episode, I’m arguing that not only is is QE, but we also have a historical example of how it has worked previously.

In retrospect, it is not important how one labels this.

My friend Pater Tenebrarum at the Acting Man Blog pinged me with this comment on Hussman's thoughts.

Who cares what it is called, the result is an explosive increase in the money supply!! And it's not bank lending that's behind that, because bank lending growth continues to slow down. So the economic effect is exactly the same as with "QE". It walks like a duck, quacks like a duck, guess what: it's a duck!

Thanks to all for the discussion.

https://ift.tt/37vv4yX

from ZeroHedge News https://ift.tt/37vv4yX

via IFTTT

0 comments

Post a Comment