Goldman Slams Omicron Panic: "This Mutation Is Unlikely To Be More Malicious; No Reason For Portfolio Changes"

One look at the ridiculous plunge across asset markets on Friday, which sent oil into one of its biggest tailspins in history (which as Goldman calculated would only make sense if the Omicron lockdowns are twice as bad as anything observed so far), and one would think that the Omicron variant - which as Edward Snowden so aptly put it "sounds like the name of an 80s movie's evil Robot King" (of course, the WHO had no choice but to skip the Xi variant, located right before Omicron in the Greek alphabet for obvious propaganda reasons) - is several times more aggressive and far more deadly than the Delta or any other Covid variant to date. Neither is the case, and in fact, as even Tom Peacock, one of the original Imperial College narrative-setters admitted, "it may turn out to be an odd cluster that is not very transmissable."

Alas, that would not help politicians who kill a lot of birds with just one brand new and "horrifying" variant, including getting a carte blanche for trillions in new vote-buying stimmies, enforcing even more ruthless and authoritarian government restrictions a dream come true for all liberal fans of big government, and most importantly forcing another round of mail-in ballot elections one year from today.

And yet, perhaps the pandemic apocalypse is not just around the corner. On one hand, Angelique Coetzee, the chairwoman of the South African Medical Association said today that “the new Omicron variant of the Coronavirus results in MILD disease, WITHOUT prominent symptoms.” On the other, none other than the most important bank on Wall Street - Goldman "Vampire Squid" Sachs - which sets the narrative that all other banks dutifully follow, has decided that it's not worth starting a panic crash over this mutation and in a note published late on Friday writes that "this mutation is unlikely to be more malicious and that the existing vaccines will most likely continue to be effective in preventing hospitalizations and deaths" and as a result, while Goldman "would monitor the situation in Gauteng closely over the next month, we do not think that the new variant is sufficient reason to make major portfolio changes."

Translation: brace for a face-ripping rally come Monday when carbon-based traders finally take over from the idiot algos.

Below are more details from Goldman's London trader Borislav Vladimirov who penned his "Initial thoughts on risks from the B.1.1.529 variant and market implications."

Main points

- While we do not have sufficient information to forecast a global B.1.1.529 wave, a high rate of transmission almost inevitably leads to a variant’s dominance.

- Nevertheless, the South Africa NICD (link to their Q&A here) note that this mutation is unlikely to be more malicious and that the existing vaccines will most likely continue to be effective in preventing hospitalizations and deaths. The current PCR and antigen tests are expected to continue to identify the mutation.

- As such, while we would monitor the situation in Gauteng closely over the next month, we do not think that the new variant is sufficient reason to make major portfolio changes.

- Having said that, given the time of the year and liquidity as well as policy risks in December, investors could consider short term hedges for growth sensitive risky assets.

We would start from what we know:

- The variant has a large number of mutations

- It has the P681 H spike protein mutation associated with the higher transmissibility of Delta

- Currently no unusual symptoms have been reported following infection with the B.1.1.529 variant and as with other variants some individuals are asymptomatic.

- It is easy to identify and hence monitor - The B.1.1.529 lineage has a deletion (△69-70) within the S gene that allowed for rapid identification of this variant in South Africa and will enable continued monitoring of this lineage irrespective of available sequence data.

- Most likely current PCR and Antigen test will continue to identify it well.

Potentially high transmissibility has triggered market concern:

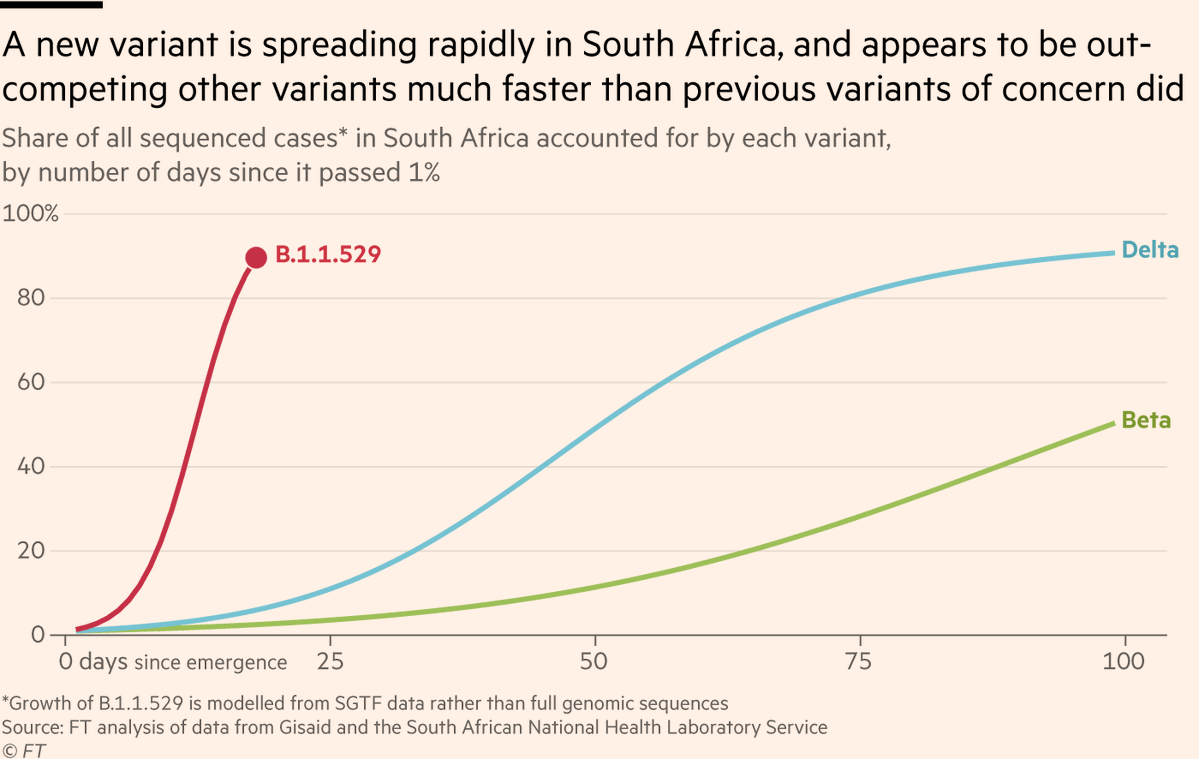

- It is gaining pace rapidly sequencing 90% of new cases just 2 weeks since emergence. For comparison the Delta needed 3 months to reach that intensity. This is the most concerning data point that has attracted market attention.

- One caveat is that the fast acceleration data could be skewed by location. The virus is spreading in Gauteng which is the largest and most densely populated province of SA. (15.2mio people with population density that is 17.3x higher than the country average)

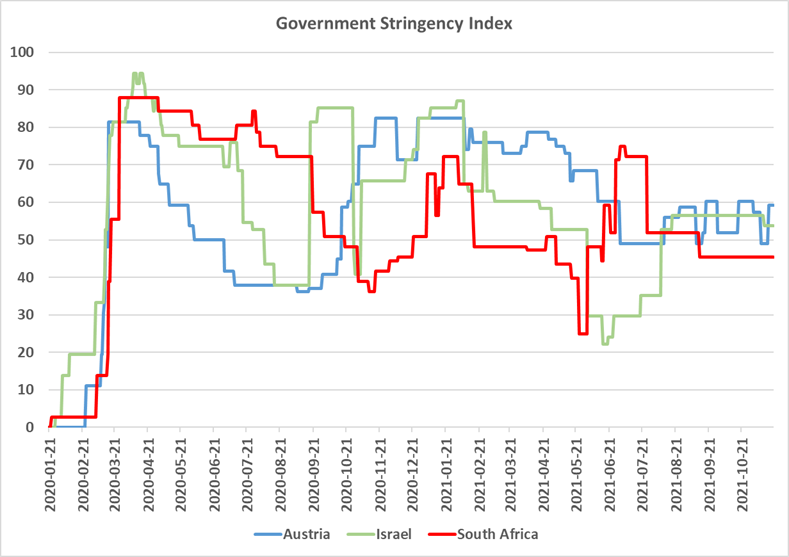

- The level of restrictions in SA at the moment (measured by the government stringency index) is low (relative to Israel or Austria for example, see chart below). This can be helping faster spread that isn’t necessarily driven exclusively by the virus characteristics

- Cases of B.1.1.529 have been identified in Botswana, Israel and Hong Kong. If the variant is highly transmissible, it is most likely that it will eventually spread despite travel restrictions.

What we still do not know...

- We have no information on the variant’s impact on hospitalizations and mortality. A careful monitoring of the Gauteng data over the next two weeks is essential.

- There are reports that two of the cases were fully vaccinated. This is a very small sample to make any conclusions and we do not know for how long the patients were vaccinated. What we know from Delta is that antibody levels wear off between 6 and 9 months after the second vaccine and that while the vaccines are less effective in preventing infection, they are still highly effective in preventing hospitalization and death. For the time being there is no reason to believe that this variant will be different in that respect.

- Will the Pfizer pill be effective against the new mutation?

- Is the European wave driven by the new variant?

- While the new variant could be present in Europe, the rapid rise in cases is driven by the Delta variant (see information below)

- The European data comes with about a month delay from sequencing time so we should know more by the third week of December (unless the process accelerates due to the attention on the new variant)

- Efforts to limit the current Delta wave in a number of European countries could help preventing the spread of B.1.1.529, if already present.

Is the above a reason to be concerned?

- A very broad press focus in the past 24h has received high market attention.

- It will take weeks before we get additional official information and scientific evidence about the potential risks.

- This comes at a time when investors have been surprised by some of the lockdown measures announced in Europe

- And also when real growth is likely to fall meaningfully on higher inflation (even though nominal growth is likely to stay well above average)

- At this time of the year positions in risky assets, especially after strong YTD gains, could be vulnerable to short term corrections (ie 2018 template)

- Travel restrictions will delay the process of logistics network normalization which would imply that the supply capacity constraints easing anticipated for H2-2022 might take longer to materialize.

- Meanwhile, monetary policy has recently shifted gears to signal faster removal of accommodation which could add to a short-term risk aversion into the December FOMC.

Conclusion: while we do not have sufficient information to forecast a global B.1.1.529 wave, a high rate of transmission almost inevitably leads to a variant dominance. Nevertheless, we can have reasonable degree of confidence that this mutation is unlikely to be more malicious and that the existing vaccines will most likely continue to be effective in preventing hospitalizations and deaths. As such, while we would monitor the situation in Gauteng closely over the next month, we do not think that the new variant is sufficient reason to make major portfolio changes.

https://ift.tt/3rdsDhk

from ZeroHedge News https://ift.tt/3rdsDhk

via IFTTT

0 comments

Post a Comment