Nava Capital: Fasten Your Seat Belts

Submitted by Damien Cleusix of NAVA Capital

Why we have never felt more bearish in our 25 years career.

The background:

-

The US stock market is more overvalued than it has ever been (https://research.nava.capital/market-valuations/) which in itself has little influence on short-term market gyrations. To this we must add that the Grantham behavioral PE ratio (trying to justify higher PE ratios by low volatility, macro and ROE volatility) is now indicating that the markets are way too high as well.

-

Debt level around the world is the highest it has even been (https://blogs.imf.org/2021/12/15/global-debt-reaches-a-record-226-trillion/) and much of this debt has been raised for unproductive use (buyback of existing capital, fiscal largess for short term consumption,…) while the stock of capital has failed to raise as much, by a wide margin (https://www.linkedin.com/pulse/central-bank-enablers-global-instability-damien-cleusix).

-

Central Banks uber-expansive monetary policies have failed to see the imbalance develop and are over-confident on the strength of the financial system. They think that because banks, especially in the US are better capitalized, because household and non-financial companies balance sheet appear strong, that everything will be fine.

-

Banks are stronger but this time the lending spree is occurring elsewhere, in less regulated entities and that can only end badly (https://www.ft.com/content/7bd7a109-2dd5-4d3b-ba7a-5fb8ad25ed45).

Households and non-financial companies’ health are deceiving. First you must analyze the distribution. Few households own an incommensurate share of assets and few companies earn an incommensurate share of profits. The asset side of both balance sheet contain many items whose valuation are in unchartered territory so every debt to asset ratios looks good by definition. Don’t be fooled.

One of the poster children of increasing debt for the purchase of existing capital is buybacks and M&A. While both can be justified when they are done in a price sensitive, opportunistic way, today’s binge buying cannot be justified (https://corpgov.law.harvard.edu/2020/10/23/the-dangers-of-buybacks-mitigating-common-pitfalls/).

Buybacks and dividends are not yet siphoning 100 % of operating earnings (https://www.yardeni.com/pub/bbdivepsyield.pdf) but remember that earnings have been pushed way above trend thanks to the huge recent fiscal deficits which are now waning (https://twitter.com/hussmanjp/status/1500947365620027393?s=20&t=4xkKStm0GGef6Ti-62KgRA).

Buybacks are one of the current best example of passive, value agnostic, buying activity pushing the markets higher.

To the Passive, value agnostic buying and selling, we also have to had risk-parity and other target volatility strategies and trend following. All of them also bolstered by the rise of the robot advisors.

The explosion of option trading where the notional traded in options is now surpassing the trading in the stock markets has add also profound implications in sustaining the current boom (https://www.zerohedge.com/markets/shocked-goldman-trader-admits-after-following-market-18-years-i-could-never-imagine-typing) If buying such large amount of extremely short-term options is not market manipulation then what is?

A final point to consider (and we are not exhaustive we know…) is the fact that households have embraced the stock market again, big ways. Households have increased their share of the overall stock market by USD 1.6 Trillion in 2021 (in comparison the whole Hedge Fund US equity holding is 2.3 trillion)!

Some people (SPACs?) have taken advantage (literally) of this.

OK now enough for the background and let’s look at what has been happening recently

-

In November, our LT warning models (we have many of them) triggered sell signal one after the other. We ended up with a total which was making the other historical precedent (beginning of 2000, Summer 2007, Spring 2015, September 2018 and December 2019) look trivial.

-

Since the start of the year we have witnessed a flurry of +1% and -1% days. When we see such concentration of volatility after a long period of calm, the probability is high that we have entered a cyclical bear market.

-

The Fed which has been the chief enabler of the current massive bubble seems to understand that it is now cornered and won’t be able, as long as inflation remains high, to offer the now expected Fed put anytime soon. J. Powell even said that it could continue to raise rate in a recession if inflation remains sticky. The Fed restrictive policy will not be limited to aggressively raise rate but with an accelerated Quantitative Tightening. We doubt that it will deliver everything the market expect if a cyclical bear market materialize but the damage to investors psychology would be large enough that even a reversal would not save the market immediately.

-

This brings us to the recession debate. While our recession indicators have yet to flash a definitive signal, most of them are very close to trigger. Given what we have said about the Fed above and the fragility of the markets, our guess is that the lead time of those indicators will be shorter than what they have been historically and the recession could well start in 2022 in the US. It is significant because bear markets tend to be much more severe when a recession occurs (https://www.yardeni.com/pub/stmktsp500recess.pdf)

We have now entered the buyback blackout period where opportunistic buybacks are not allowed.

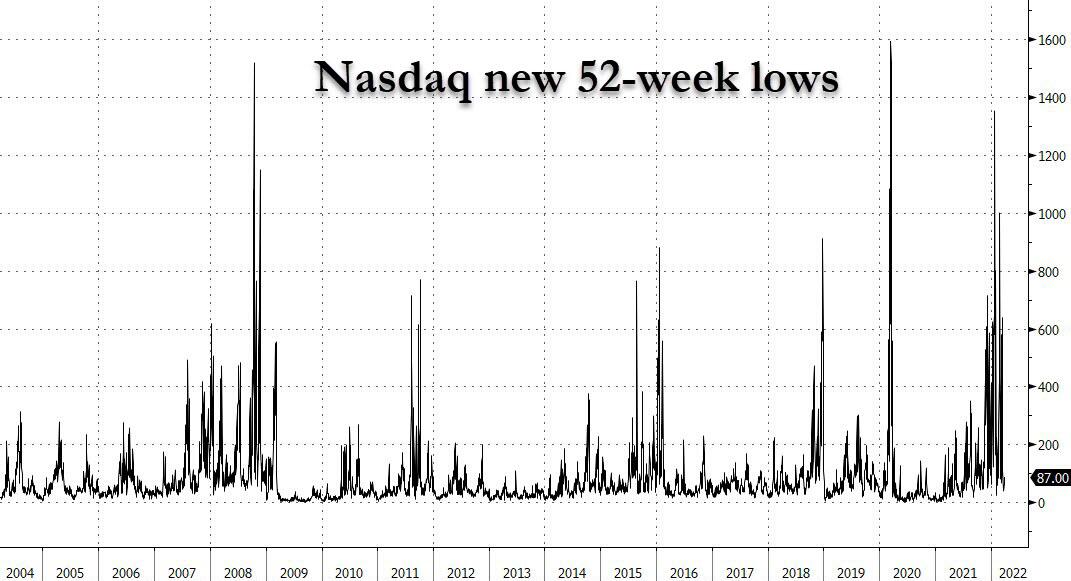

At the same time the S&P 500 has staged an impressive rebound from last week low and yet we are still seeing more 52 weeks new lows than highs. This (almost) only happen in bear markets.

Given the quarterly bonds and equities relative performance we should witness some sizable rebalancing towards bonds (even if bonds increased volatility could make it less sizable than some commentators are expecting).

With the S&P 500 slightly more than 5% below its all time high we see it as a perfect opportunity for those who haven’t yet done so to aggressively de-risk their portfolio.

https://ift.tt/KncmWtv

from ZeroHedge News https://ift.tt/KncmWtv

via IFTTT

0 comments

Post a Comment