Morgan Stanley: "In Hindsight, 2022 Is Kind Of Simple, It's Not Exactly Fermat's Last Theorem"

By Andrew Sheets, Chief Cross-Asset Strategist for Morgan Stanley

It’s a funny year. Returns are awful, with significant losses in almost every asset class not labelled 'commodities'. Investors still face wide-ranging uncertainties, from how fast the Fed tightens, to whether Europe sees an energy crisis, to how China addresses Covid, to the ongoing fall of the yen. Cross-asset performance feels confused, with defensive equities unusually strong while government bonds are unusually weak.

But step back a bit, and 2022, in hindsight, is also kind of simple. Valuations were high and policy is tightening and growth is slowing…and prices have fallen. Cheaper stocks are (finally) outperforming more expensive ones. Bond yields were very low and are (finally) rising. Credit and MBS spreads were tight, and have widened. The UK has weak growth, a large current account deficit and world-beating negative real yields, and has seen its currency weaken substantially. It’s not exactly Fermat’s Last Theorem.

So what should investors do, given a complex set of challenges, but also signs of underlying rationality? This can be a good time to step back and look at what rules-based indicators are telling us.

Let’s start by focusing on what these indicators say about where we are in the cycle, and what that means for investment strategy. Our cycle indicator looks at a range of economic indicators and tries to map them to historical patterns of cross-asset performance.

Our indicator sees the data as highly extended versus trend. We call this 'late cycle' because, historically, readings sharply above trend have often (but not always) occurred later in an economic expansion. This statement is not about predicting a recession, necessarily, but our economists are convicted that we are seeing a meaningful deceleration. And thinking probabilistically, that type of deceleration almost surely increases the chances of a downturn. Whether the contraction materializes or not, it will affect cross-asset performance today.

At present, the late-cycle indicator is consistent with underperformance of high yield credit relative to both equities and bonds, the outperformance of defensive equities, a flatter curve and fewer headwinds to long-end duration.

Of course, our cycle indicator isn’t alone in flagging caution. With the risks to the market so obvious, sentiment is negative. Which brings us to the next question – despite the macro challenges, is sentiment now extreme enough to boost markets?

It’s possible. But our best attempts to statistically quantify a sentiment signal say 'not yet'. In a recent report led by my colleague Naomi Poole, we explored the efficacy of different measures of 'sentiment' and turning them into a signal. We think that using a composite of sentiment indicators is most powerful, and that level and trend of sentiment matter for creating a signal with good returns and hit rates over time. Our indicator is not yet extreme, and has not yet turned (it is ‘neutral’). We are watching it closely.

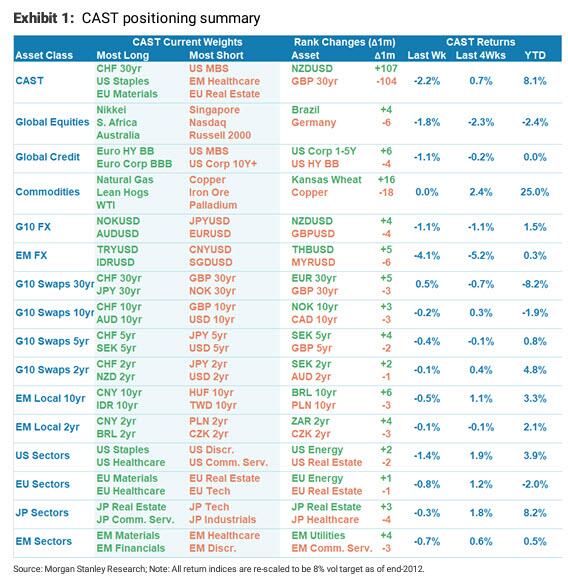

Given the swirling mix of storylines and volatility, a third related question is what would a fully rules-based cross-asset strategy do today? For that, we turn to CAST, our Cross-Asset Systematic Trading strategy, developed by my colleague Phani Naraparaju. CAST is the most powerful quantitative instrument in our cross-asset toolkit, evaluating ~1,500 factors across ~150 global assets. For all that complexity, it asks a simple question – what looks most attractive today based on what some of those factors (different measures of carry, valuation, momentum and fundamentals) have meant in the past?

CAST has helped our process so far this year. While it has certainly gotten things wrong, it has gotten more things right, especially a positive view on commodities, a defensive skew in US equities and a negative view on JPY, GBP and global 2yr rates. It has been most successful with cross-asset relative value, while struggling more with directional views, a not-so-subtle hint that this is a better market for alpha than beta. And while CAST is a completely rules-based tool, we pay special attention where its views align with the bottom-up, fundamental calls of our strategy colleagues. A few things stand out.

CAST is dialling back its beta, especially in commodities, where it has become more negative on copper (but still likes energy). Second, CAST is giving the same signals as our Asia macro strategists, who expect CNY weakness and like receiving CNY rates. And similar to views in equity strategy, it is positive on the Nikkei (FX-hedged) and Healthcare, and negative on the NASDAQ and Russell 2000. CAST has also unwound a large credit compression trade it had been running post-Covid, which lines up with the decompression and dispersion theme our credit strategists expect to be more prominent.

Rules-based tools help in markets that are volatile, emotional and present more storylines than a reasonable investor can process. For the moment, they suggest that cross-asset performance continues to follow the late-cycle playbook, sentiment has not yet given a conclusive tactical signal, and following historical factor-based patterns is helping to trade relative value. They won’t solve everything, but given the challenges of 2022 so far, every little bit helps.

https://ift.tt/nXxNi14

from ZeroHedge News https://ift.tt/nXxNi14

via IFTTT

0 comments

Post a Comment