"The Next Leg Lower Is Coming": Mike Wilson Says Stocks Have Already Discounted The Fed Pivot Which Is Probably Not Even Coming

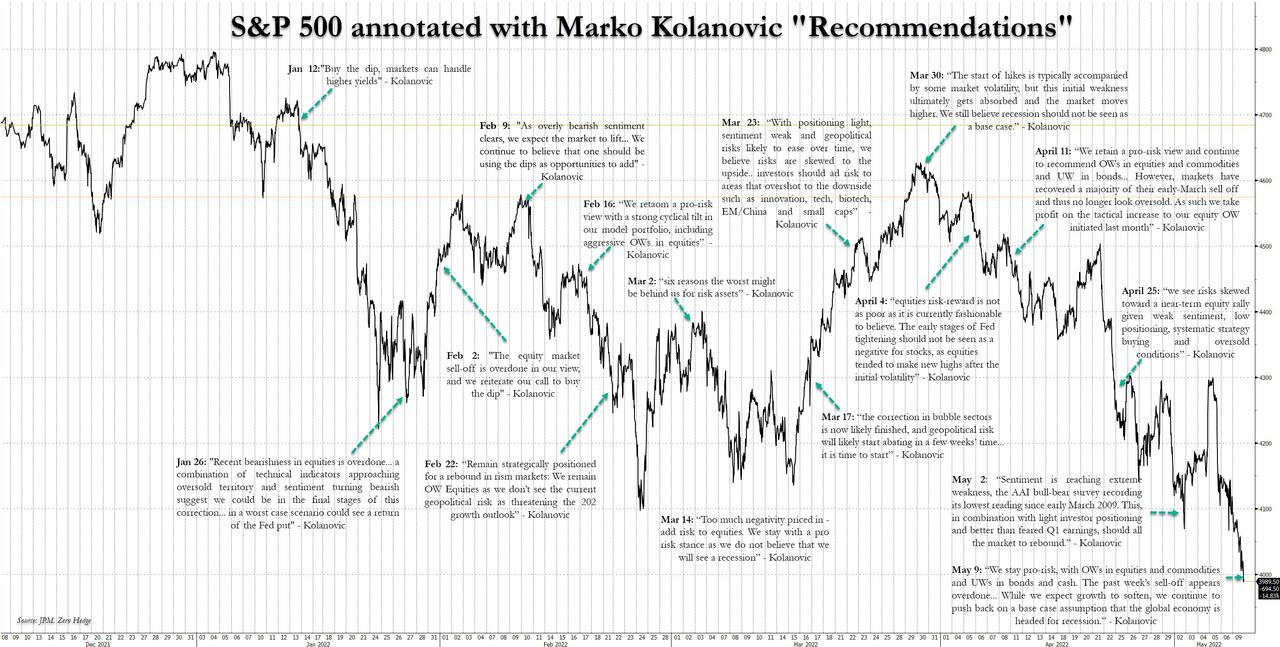

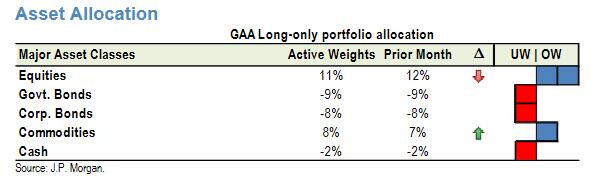

It's not an exaggeration to say that JPMorgan's now grotesquely absurd market cheerleaders haven't spent one week in 2022 without relentless pumping this bloated stock bubble, telling their clients to buy the rip, buy the dip, or otherwise, just buy. In fact the closet to a bearish capitulation, ironically, came last week when the biggest market cheerleader, Marko Kolanovic told clients that it's time to shift away from stocks to commodities...

... yet even so he was terrified of being accused of not being bullish enough for JPM's C-suite standards, and despite telling clients he would "some of our risk allocation from equities to commodities", he still kept stocks at the highest reco rating possible.

Fast forward today when in the latest example of just how absurd the Cover Your Asset mentality across wall street's terrified strategist pool has become, one week after Kolanovic said to shift (gently) away from stocks, his Croatian JPM colleague, Mislav Matejka, who is also the bank's chief equity strategist, said the rally -- which has pushed up the tech-heavy Nasdaq 100 index by over 20% -- could run through the end of the year. So shift away from stocks...but just keep buying stocks? Got it.

“Is the rebound getting overdone and should one go back into value style? Not yet, in our view,” JPMorgan strategists led by Mislav Matejka wrote.

Like we said, grotesque and absurd - not least because JPM is now directly fighting the Fed which will not allow stocks to close the year at all time highs - but that's what happens when you are wrong for so long, you have dug in so deep the hole below you is about 6 feet deep.

Neither grotesque nor absurd was the latest note from Morgan Stanley's Michael Wilson, who continues to be the bearish foil to JPM's ridiculous permabullishness, but more importantly, he continues to remain correct... well with one exception: the current non-fundamental demand driven rally (which we warned premium readers would take place more than a month ago).

In any case, far from conceding that the current bear market rally is officially a plain vanilla rally - now that the S&P has risen above the 50% fib retracement level - Wilson writes that the powerful CTA/buyback/retail/squeeze-driven meltup since June is just a pause in the bear market, and he once again predicts that share prices will slide in the second half of the year (two weeks ago he timed the date of the reversal as some time in September/October) as profits weaken, interest rates keep rising and the economy slows.

In other words, one of these two banks - JPM vs Morgan Stanley - will be terribly wrong, and their recos will cost their clients lots of money. And since we will continue to ignore the broken record from JPM, which really has had the same handful of bullet points since January and now is even barely passable for fundamental analysis, we will focus on Wilson's latest red alert, which boils down to the following: the equity market has front-run a durable Fed pause, "the odds of which are low to begin with", which leaves valuation significantly disconnected from economic/earnings reality. Risk/reward remains unattractive.

Starting at the top, Wilson starts off with a mea culpa, admitting that "the magnitude of this bear market rally has surprised many, including us", but not ZH readers who have been duly warned about what is coming since early July.

While he was unable to predict it, Wilson is quick to "explain" what happened (in retrospect, of course), and believes that the rally was been driven by a combination of better than feared 2Q earnings (although revisions/price came down into the quarter), light positioning and continued hope for a less hawkish Fed path.

Referring to his personal experience, Wilson warns that the last catalyst is "historically the one capable of driving significant late cycle rallies even amid deteriorating fundamentals" and the most recent example of this occurred in 2019 when "a durable pause in the Fed Funds Rate and then a series of cuts amid a still tight labor market catalyzed a ~40% rally in the S&P 500." This rebound came despite a severe negative earnings revisions cycle and significant margin headwinds, and culminated with the completely accidental and not at all premeditated global covid implosion which unleashed a liquidity tsunami across the globe.

Looking back at the 2019 period, Wilson notes that late-cycle earnings growth headwinds were apparent and the bank's leading earnings model pointed to negative growth 12 months out (like it does today), yet equities brushed off fundamental risks, and the market multiple expanded some 5 turns!

Not surprisingly, the leadership alone over the past 2 months is reminiscent of that 2019 period according to Wilson, who points to the first chart below which shows the performance rank of industry groups in the 2019 Fed pause rally and in the current bear market rally post mid-June. He finds it interesting that the rank order correlation is quite high as the exhibit shows, and that the majority of the leading (Tech) / lagging (Commodities, Staples) cohorts are the same. Further, Wilson also finds that factor leadership is also quite similar between the 2 periods as the second chart shows.

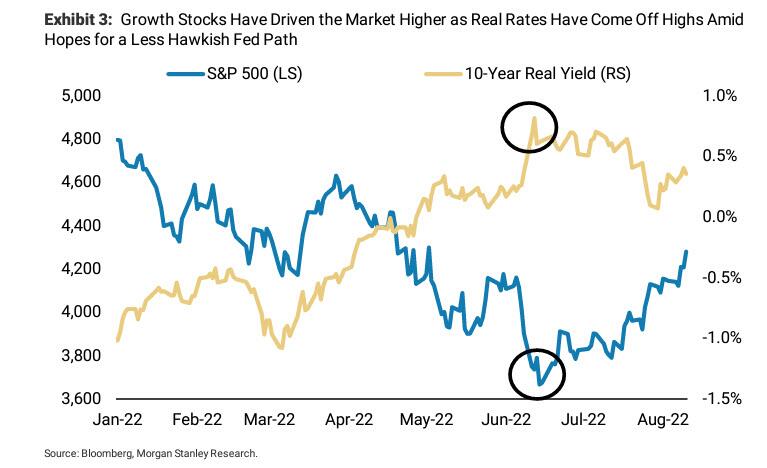

Said otherwise, with value stocks sinking (amid the recent slump in commodities and the near-record yield curve inversion), growth-oriented factors (high top line/EPS realized and forecasted growth) have outperformed significantly and have driven benchmark performance as real rates have come off recent highs amid hope for a less hawkish Fed, as markets increasingly price in Powell's capitulatory pivot (which we previewed back in June).

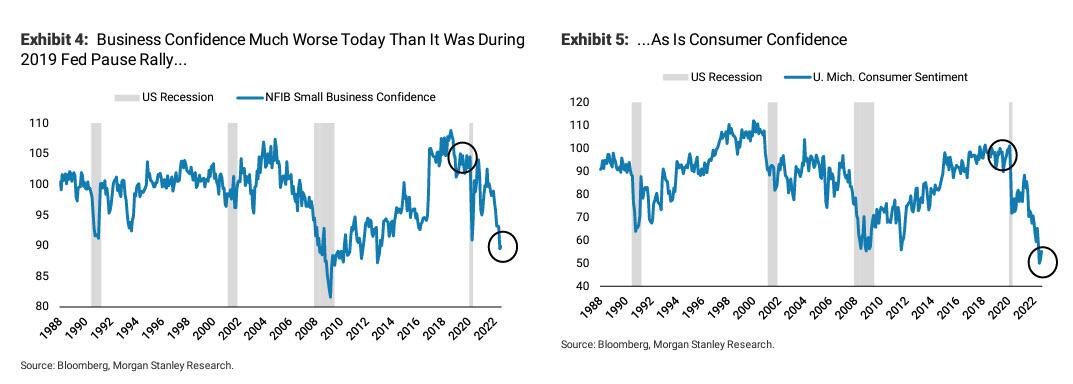

That being said, the MS strategist argues that the macro, policy, and earnings set-up is much less favorable for equities today than it was in that period, with business and consumer sentiment much more depressed today than it was then.

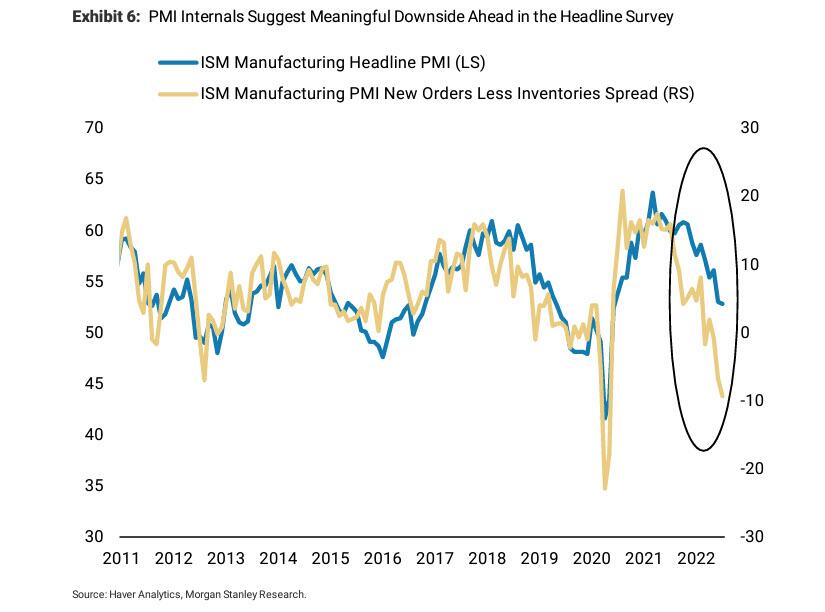

Further, going back to a point he has made repeatedly in the past, Wilson observes that leading internals within the ISM PMI survey point to continued deceleration that appears to be steeper/more severe than what we saw in 2019.

Finally, and importantly, we're in a much different cycle from an inflation standpoint: while inflation appears to be peaking (at least absent another major commodity shock like the one which the refill of the US SPR will unleash in 2 months time, or whatever Putin and Xi have up their sleeve), it's not likely to come off at a pace fast enough to spur the type of sustained Fed pause the equity market is already discounting, according to Wilson who echoes what Goldman wrote over the weekend, and warns that in reflexive fashion, easing financial conditions and a strong July labor report likely further dampen the prospects for a more dovish policy path, a reality that has been alluded to this past week by hawkish comments from Fed officials.

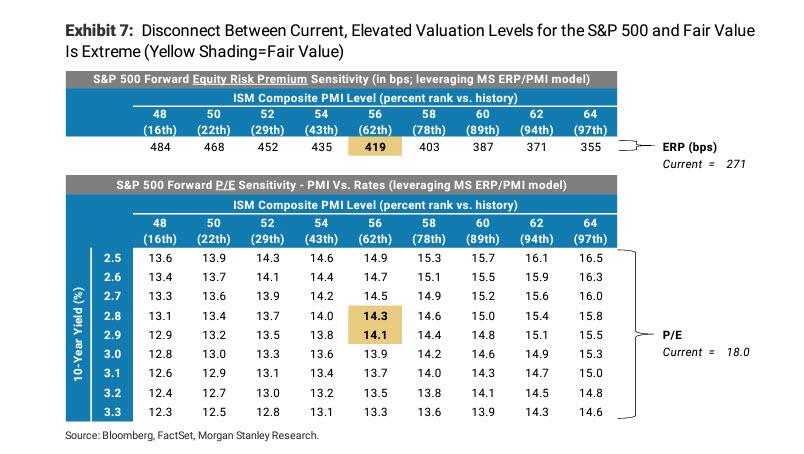

Wilson's bottom line: "the equity market has already discounted a durable Fed pause, the likelihood of which is low to begin with. That development leaves equity multiples significantly disconnected from fundamentals, which continue to suggest we're in a late cycle, slowing growth environment." In practical terms, Wilson's fair value framework which leverages the ISM PMI to project a fair value equity risk premium for the S&P 500 suggests the market's ERP is ~150 basis points too low based on current data. In multiple terms, accounting for where the US 10-year Treasury yield is today, the market trades a surprising 3.5-4 turns rich vs. fair value, or call it overvalued by about 750-1000 points.

Looking ahead, while Wilson would not rule out another couple of percentage points of upside at the S&P 500 level "tactically", the message from the Morgan Stanley strategist for the next several months remains: risk/reward is unattractive, and this bear market remains incomplete.

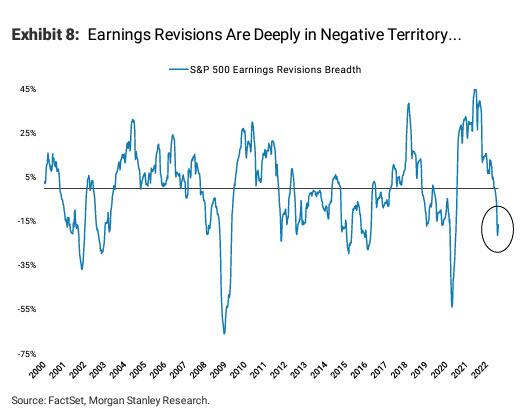

Next, addressing the question on every trader's mind, namely "what's likely to drive the next leg lower in stocks?", Wilson thinks the catalyst will end up centering around earnings disappointment. To be sure, while 2Q earnings came in far stronger than many had expected, Wilson believes that the reason we saw relief was that expectations fell significantly into the quarter, a dynamic that the equity market discounted ahead of reporting season. This is confirmed by the next chart which shows that EPS revisions began their latest leg lower well ahead of earnings season.

A similar dynamic is likely to play out ahead of 3Q earnings season (i.e., September). The chart below offers further support to this thesis by showing that seasonals for earnings revisions worsen materially over the next 2 months, and that this year's revisions have followed the historical seasonal pattern quite closely.

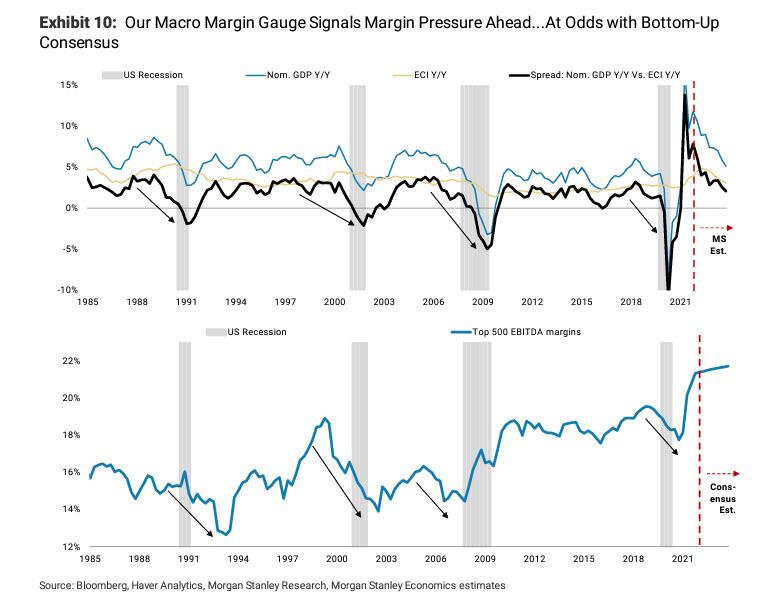

What will be the specific driver of the next leg lower in earnings expectations? Wilson thinks it will be margins: as he wrote last week, margin expectations for the out quarters/2023 appear overly optimistic as cost pressures remain sticky and demand slows. While many focused on the impact of the recent jobs and CPI prints from a Fed policy standpoint, Wilson came away with some fundamental takeaways as well: the combination of sustained, higher wage costs and slowing end market/consumer pricing loudly signals margin pressure. The next chart illustrates this dynamic simplistically, showing the spread between nominal GDP growth (a macro proxy for top line growth) and wage growth (the most pervasive cost pressure companies face; based on the Employment Cost Index) over time.

Perhaps unsurprisingly, this macro gauge tends to track operating margins pretty well over time, and is pointing to a deceleration in margins from here. This dynamic is at odds with bottom-up consensus, which is still calling for all-time high operating margins next year. Morgan Stanley is naturally skeptical, and foresees downward estimate revisions with respect to margins over the coming months.

There is much more in the full Wilson note available to pro subscribers in the usual place

https://ift.tt/D5QmN9L

from ZeroHedge News https://ift.tt/D5QmN9L

via IFTTT

0 comments

Post a Comment