Today's Energy Crisis Is Very Different From The Energy Crisis Of 2005

Authored by Gail Tverberg via Our Finite World blog,

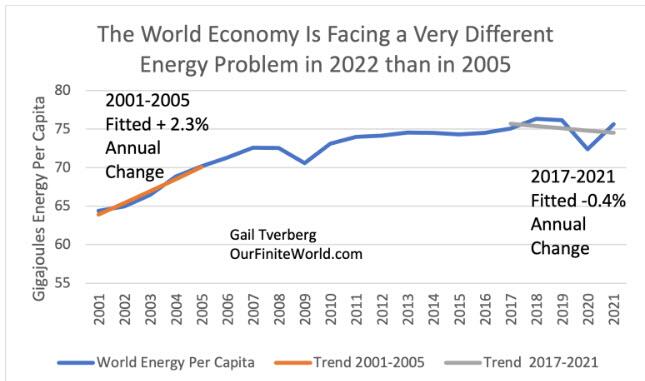

Back in 2005, the world economy was “humming along.” World growth in energy consumption per capita was rising at 2.3% per year in the 2001 to 2005 period. China had been added to the World Trade Organization in December 2001, ramping up its demand for all kinds of fossil fuels. There was also a bubble in the US housing market, brought on by low interest rates and loose underwriting standards.

Figure 1. World primary energy consumption per capita based on BP’s 2022 Statistical Review of World Energy.

The problem in 2005, as now, was inflation in energy costs that was feeding through to inflation in general. Inflation in food prices was especially a problem. The Federal Reserve chose to fix the problem by raising the Federal Funds interest rate from 1.00% to 5.25% between June 30, 2004 and June 30, 2006.

Now, the world is facing a very different problem. High energy prices are again feeding over to food prices and to inflation in general. But the underlying trend in energy consumption is very different. The growth rate in world energy consumption per capita was 2.3% per year in the 2001 to 2005 period, but energy consumption per capita for the period 2017 to 2021 seems to be slightly shrinking at minus 0.4% per year. The world seems to already be on the edge of recession.

The Federal Reserve seems to be using a similar interest rate approach now, in very different circumstances. In this post, I will try to explain why I don’t think that this approach will produce the desired outcome.

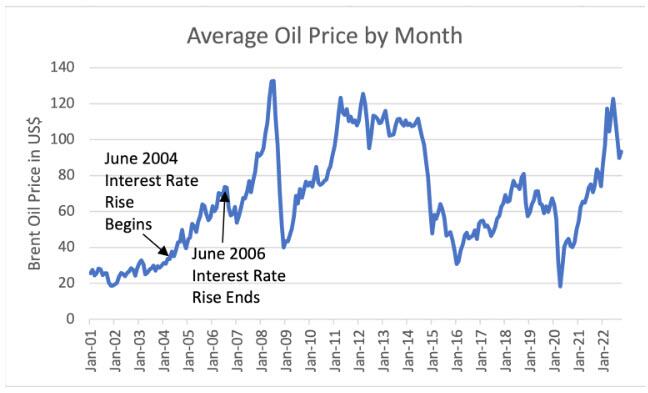

[1] The 2004 to 2006 interest rate hikes didn’t lead to lower oil prices until after July 2008.

It is easiest to see the impact (or lack thereof) of rising interest rates by looking at average monthly world oil prices.

Figure 2. Average monthly Brent spot oil prices based on data of the US Energy Information Administration. Latest month shown is July 2022.

The US Federal Reserve began raising target interest rates in June 2004 when the average Brent oil price was only $38.22 per barrel. These interest rates stopped rising at the end of June 2006, when oil prices averaged $68.56 per barrel. Oil prices on this basis eventually reached $132.72 per barrel in July 2008. (All of these amounts are in dollars of the day, rather than being adjusted for inflation.) Thus, the highest price was over three times the price in June 2004, when the US Federal Reserve made the decision to start raising target interest rates.

Based on Figure 2 (including my notes regarding the timing of the interest rate rise), I would conclude that raising interest rates didn’t work very well at bringing down the price of oil when it was tried in the 2004 to 2006 period. Of course, the economy was growing rapidly, then. The rapid growth of the economy likely led to the very high oil price shown in mid-2008.

I expect that the result of the US Federal Reserve raising interest rates now, in a low-growth world economy, might be quite different. The world’s debt bubble might pop, leading to a worse situation than the financial crisis of 2008. Indirectly, both assets prices and commodity prices, including oil prices, would tend to fall very low.

Analysts looking at the situation from strictly an energy perspective tend to miss the interconnected nature of the economy. Factors which energy analysts overlook (particularly debt becoming impossible to repay, as interest rates rise) may lead to an outcome that is pretty much the opposite result of the standard belief. The typical belief of energy analysts is that low oil supply will lead to very high prices and more oil production. In the current situation, I expect that the result might be closer to the opposite: Oil prices will fall because of financial problems brought on by the higher interest rates, and these lower oil prices will lead to even lower oil production.

[2] The purpose of the US Federal reserve raising target interest rates was to flatten the growth rate of the world economy. Looking back at Figure 1, the growth in energy consumption per capita was much lower after the Great Recession. I doubt that now in 2022, we want even lower growth (really, more shrinkage) in energy consumption per capita for future years.*

Looking at Figure 1, growth in energy consumption per capita has been very slow since the Great Recession. A person wonders: What is the point of governments and their central banks pushing the world economy down, now in 2022, when the world economy is already barely able to maintain international supply lines and provide enough diesel for all of the world’s trucks and agricultural equipment?

If the world economy is pushed downward now, what would the result be? Would some countries find themselves unable to afford fossil fuel energy products in the future? This might lead to problems both in growing and transporting food, at least for these countries. Would the whole world suffer a major crisis of some sort, such as a financial crisis? The world economy is a self-organizing system. It is difficult to forecast precisely how the situation would work out.

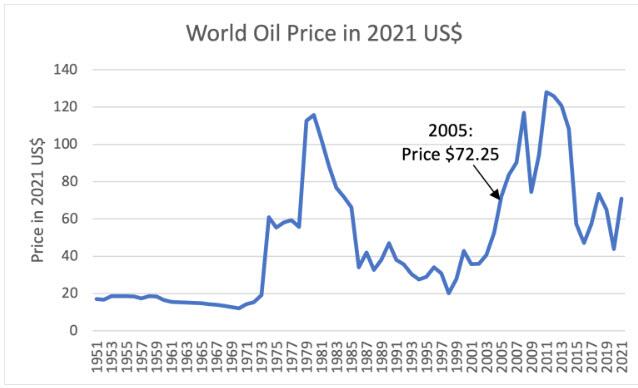

[3] While the growth rate in energy consumption per capita was much lower after 2008, the price of crude oil quickly bounced back to over $120 per barrel in inflation-adjusted prices.

Figure 3 shows that oil prices immediately bounced back up after the Great Recession of 2008-2009. Quantitative Easing (QE), which the US Federal Reserve began in late 2008, helped energy prices to shoot back up again. QE helped keep the cost of borrowing by governments low, allowing governments to run larger deficits than might otherwise have been possible without interest rates rising. These higher deficits added to the demand for commodities of all types, including oil, thus raising prices.

Figure 3. Average annual oil prices inflation-adjusted oil prices based on data from BP’s 2022 Statistical Review of World Energy. Amounts shown are Brent equivalent spot prices.

The chart above shows average annual Brent oil prices through 2021. The above chart does not show 2022 prices. The current Brent oil price is about $91 per barrel. So, oil prices today are a little higher than they have been recently, but they are nowhere nearly as high as they were in the 2011 to 2013 period or in the late 1970s. The extreme reaction we are seeing is very strange. The problem seems to be much more than oil prices, by themselves.

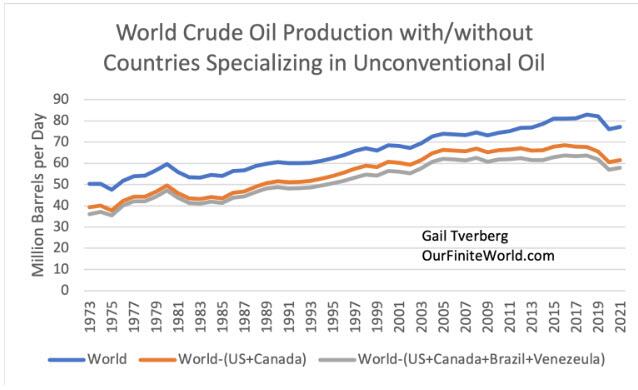

[4] High prices in the 2006 to 2013 period allowed the rise of unconventional oil production. These high oil prices also helped keep conventional oil production from falling after 2005.

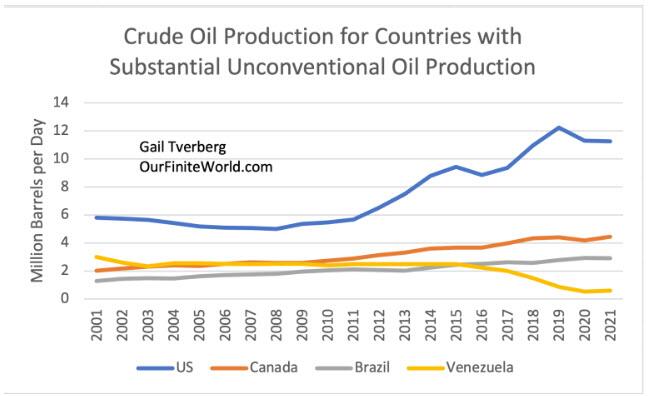

It is difficult to find detail on the precise amount of unconventional oil, but some countries are known for their unconventional oil production. For example, the US has become a leader in the extraction of tight oil from shale formations. Canada also produces a little tight oil, but it also produces quite a bit of very heavy oil from the oil sands. Venezuela produces a different type of very heavy oil. Brazil produces crude oil from under the salt layer of the ocean, sometimes called pre-salt crude oil. These unconventional types of extraction tend to be expensive.

Figure 4 shows world oil production for various combinations of countries. The top line is total world crude oil production. The bottom gray line approximates world total conventional oil production. Unconventional oil production has been rising since, say, 2010, so this approximation is better for years 2010 and subsequent years on the chart, than it is for earlier years.

Figure 4. Crude and condensate oil production based on international data of the US Energy Information Administration. The lower lines subtract the full amount of crude and condensate production for the countries listed. These countries have substantial amounts of unconventional oil production, but they may also have some conventional production.

From this chart, it appears that world conventional oil production leveled off after 2005. Some people (often referred to as “Peak Oilers”) were concerned that conventional oil production would reach a peak and begin to decline, starting shortly after 2005.

The thing that seems to have kept production from falling after 2005 is the steep rise in oil prices in the 2004 to 2008 period. Figure 3 shows that oil prices were quite low between 1986 and 2003. Once oil prices began to rise in 2004 and 2005, oil companies found that they had enough revenue that they could start adopting more intensive (and expensive) extraction techniques. This allowed more oil to be extracted from existing conventional oil fields. Of course, diminishing returns still set in, even with these more intensive techniques.

These diminishing returns are probably a major reason that conventional oil production started to fall in 2019. Indirectly, diminishing returns likely contributed to the decline in 2020, and the failure of the oil supply to bounce back up to its 2018 (or 2019) level in 2021.

[5] A better way of looking at world crude oil production is on per capita basis because the world’s crude oil needs depend on world population.

Everyone in the world needs the benefit of crude oil, since crude oil is used in farming and in transporting goods of all kinds. Thus, the need for crude oil rises with population growth. I prefer analyzing crude oil production on a per capita basis.

Figure 5. Per capita crude oil production based on international data by country from the US Energy Information Administration.

Figure 5 shows that on a per capita basis, conventional crude oil production (gray bottom line) started declining after 2005. It was only with the addition of unconventional oil that crude oil production per capita could remain fairly level between 2005 and 2018 or 2019.

[6] Unconventional oil, if analyzed by itself, seems to be quite price sensitive. If politicians everywhere want to hold oil prices down, the world cannot count on extracting very much of the huge amount of unconventional oil resources that seem to be available.

Figure 6. Crude oil production based on international data for the US Energy Information Administration for each of the countries shown.

On Figure 6, crude oil production dips in 2016 and 2017 and also in 2020 and 2021. Both the 2016 the 2020 dips are related to low price. The continued low prices in 2017 and 2021 may reflect start-up problems after a low price, or they may reflect skepticism that prices can stay high enough to make continued extraction profitable. Canada seems to show similar dips in its oil production.

Venezuela shows a fairly different pattern. Information from the US Energy Information Administration mentions that the country started having major problems once the world oil price started falling in 2014. I am aware that the US has had sanctions against Venezuela in recent years, but it seems to me that these sanctions are closely related to Venezuela’s oil price problems. If Venezuela’s very heavy oil could really be extracted profitably, and the producers of this oil could be taxed to provide services for the people of Venezuela, the country would not have the many problems that it has today. The country likely needs a price between $200 and $300 per barrel to allow sufficient funds for extraction plus adequate tax revenue.

Brazil’s oil production seems to be relatively more stable, but its growth has been slow. It has taken many years to get its production up to 2.9 million barrels per day. There is also some pre-salt oil production just now getting started in Angola and other countries of West Africa. This type of oil requires a high level of technical expertise and imported resources from around the world. If world trade falters, this type of oil production is likely to falter, as well.

A large share of the world’s oil reserves are unconventional oil reserves, of one type or another. The fact that rising oil prices are a real problem for citizens means that these unconventional reserves are unlikely to be tapped. Instead, we may be dealing with seriously short supplies of products we need for operating our economy, including diesel oil and jet fuel.

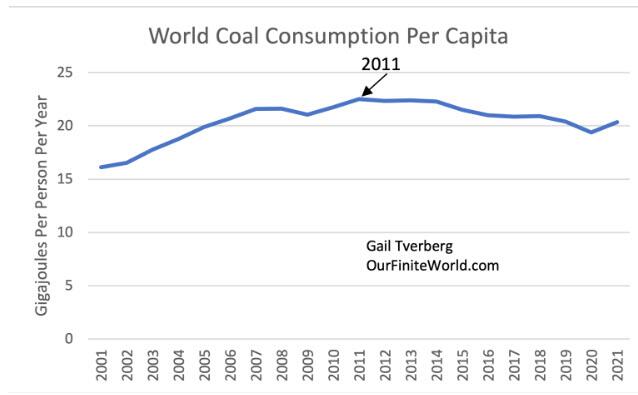

[7] Figure 1 at the beginning of this post indicated falling primary energy consumption per capita. This problem extends to more than oil. On a per capita basis, both coal and nuclear energy consumption are falling.

Practically no one pays any attention to coal consumption, but this is the fuel that allowed the Industrial Revolution to start. It is reasonable to expect that since the world economy started using coal first, it might be the first to deplete. Figure 7 shows that world coal consumption per capita hit a peak in 2011 and has declined since then.

Figure 7. World coal consumption per capita, based on data from BP’s 2022 Statistical Review of World Energy.

Many of us have heard about Aesop’s Fable, The Fox and the Grapes. According to Wikipedia, “The story concerns a fox that tries to eat grapes from a vine but cannot reach them. Rather than admit defeat, he states they are undesirable. The expression ‘sour grapes’ originated from this fable.”

In the case of coal, we are told that coal is undesirable because it is very polluting and raises CO2 levels. While these things are true, coal has historically been very inexpensive, and this is important for people buying coal. Coal is also easy to transport. It could be used for fuel instead of cutting down trees, thus helping local ecosystems. The negative things that we are being told about coal are true, but it is hard to find an adequate inexpensive substitute.

Figure 8 shows that world nuclear energy per capita is also falling. To some extent, its fall has stabilized since 2012 because China and a few other “developing nations” have been adding nuclear capacity, while developed nations in Europe have tended to remove their existing nuclear power plants.

Figure 8. World nuclear electricity consumption per capita, based on data from BP’s 2022 Statistical Review of World Energy. Amounts are based on the amount of fossil fuels that this electricity would theoretically replace.

Nuclear energy is confusing because experts seem to disagree on how dangerous nuclear power plants are, over the long term. One concern relates to proper disposal of spent fuel after its use.

[8] The world seems to be at a difficult time now because we don’t have any good options for fixing our falling energy consumption per capita problem, without greatly reducing world population. The two choices that seem to be available both seem to be far higher-priced than is feasible.

There are two choices that seem to be available:

[A] Encourage large amounts of fossil fuel production by encouraging very high fossil fuel prices. With such high prices, say $300 per barrel for oil, unconventional crude oil in many parts of the world would be available. Unconventional coal, such as that under the North Sea, would also be available. With sufficiently high prices, natural gas production could be raised. This natural gas could be shipped as liquefied natural gas (LNG) around the world at great cost. Additionally, many processing plants could be built, both for supercooling the natural gas to allow it to be shipped around the world and for re-gasification, when it arrives at its destination.

With this approach, food costs would be very high. Much of the world’s population would need to work in the food industry and in fossil fuel production and shipping. With these priorities, citizens would not have time or money for most things we buy today. They likely could not afford a vehicle or a nice home. Governments would need to shrivel in size, with the usual outcome being government by a local dictator. Governments wouldn’t have sufficient funds for roads or schools. CO2 emissions would be very high, but this likely would not be our biggest problem.

[B] Try to electrify everything, including agriculture. Greatly ramp up wind and solar. Wind and solar are very intermittent, and their intermittency does not match up well with human needs. In particular, the world’s big need is for heat in winter, while solar energy comes in summer. It cannot be saved until winter with today’s technology. Spend enormous amounts and resources on electricity transmission lines and batteries to try to somewhat work around these problems. Try to find substitutes for the many things that fossil fuels provide today, including paved roads and chemicals used in agriculture and in medicine.

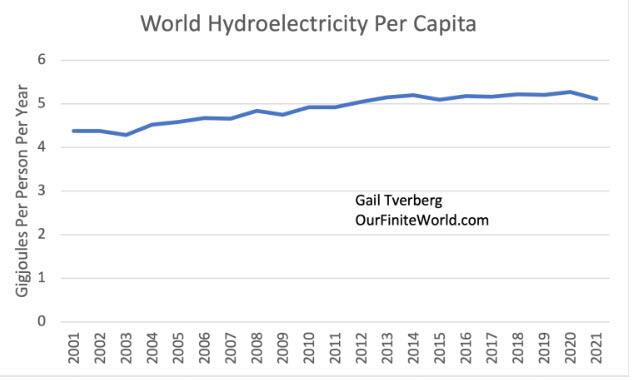

Hydroelectricity is also a renewable form of electricity generation. It cannot be expected to ramp up much because it has mostly been built out already.

Figure 9. World consumption of hydroelectricity per capita, based on data from BP’s 2022 Statistical Review of World Energy.

Even if greatly ramped up, wind and solar electricity production would likely be grossly inadequate by themselves to try to operate any kind of economy. At a minimum, natural gas, at very high cost, shipped as LNG around the world, would likely be needed in addition. A huge quantity of batteries would be needed, leading to a short supply of materials. Huge quantities of steel would be needed to make new electrical machines to try to replace current oil-power machines. A minimum 50-year transition would likely be needed.

I am doubtful that this second approach would be feasible in any reasonable timeframe.

[9] Conclusion. Figure 1 seems to imply that the world economy is headed for a troubled times ahead.

The world economy is a self-organizing system, so we cannot know precisely what form changes in the next few years will take. The economy can be expected to shrink back in an uneven pattern, with some parts of the world and some classes of citizens, such as workers versus the elderly, doing better than others.

Leaders will never tell us that the world has an energy shortage. Instead, leaders will tell us how awful fossil fuels are, so that we will be happy that the economy is losing their usage. They will never tell us how worthless intermittent wind and solar are for solving today’s energy problems. Instead, they will lead us to believe that a transition to vehicles powered by electricity and batteries is just around the corner. They will tell us that the world’s worst problem is climate change, and that by working together, we can move away from fossil fuels.

The whole situation reminds me of Aesop’s Fables. The system puts a “good spin” on whatever frightening changes are happening. This way, leaders can convince their citizens that everything is fine when, in fact, it is not.

NOTE

*If the US Federal Reserve raises its target interest rate, central banks of other countries around the world are forced to take a similar action if they do not want their currencies to fall relative to the US dollar. Countries that do not raise their target interest rates tend to be penalized by the market: With a falling currency, the local prices of oil and other commodities tend to rise because commodities are priced in US dollars. As a result, citizens of these countries tend to face a worse inflation problem than they would otherwise face.

The country with the greatest increase in its target interest rate can, in theory, win, in what is more or less a competition to move inflation elsewhere. This competition cannot go on indefinitely, however, because every country depends, to some extent, on imports from other countries. If countries with the weaker economies (i. e. those that cannot afford to raise interest rates) stop producing essential goods for world trade, it will tend to bring the world economy down.

Raising interest rates also raises the likelihood of debt defaults, and these debt defaults can be a huge problem, especially for banks and other financial institutions. With higher interest rates, pension funding becomes less adequate. Businesses of all kinds find new investment more expensive. Many businesses are likely to shrink or fail completely. These indirect impacts are yet another way for the world economy to fail.

https://ift.tt/5Y7MAyJ

from ZeroHedge News https://ift.tt/5Y7MAyJ

via IFTTT

0 comments

Post a Comment