US Consumers Hit A Brick Wall: December Credit Growth Craters As Interest Rates Soar

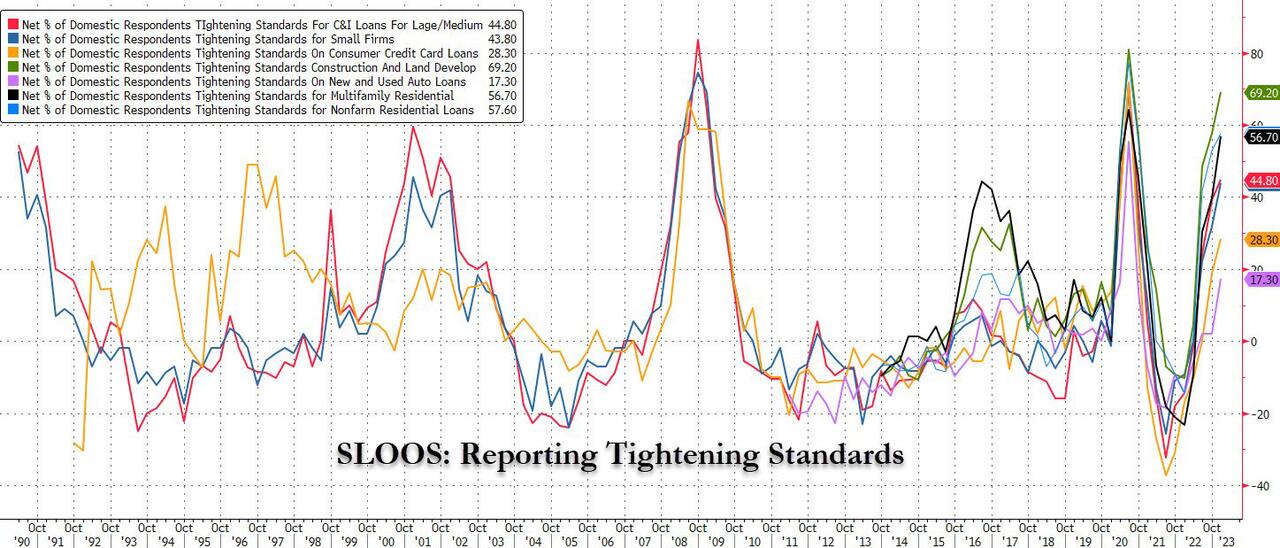

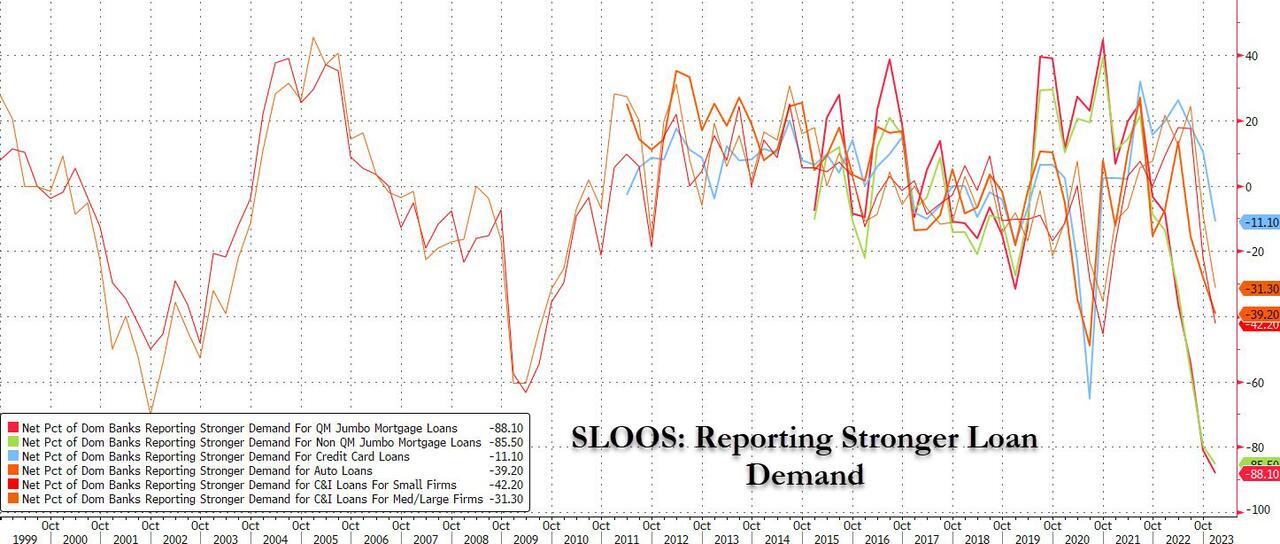

Yesterday we showed the latest confirmation that the US economy was sliding into a recession: according to the January Senior Loan Officer Opinion Survey held by the Fed, the economic situation in the US had gotten especially dire in the past few months as on one hand, banks have sharply tightened lending standards for commercial, mortgage and credit card loans, making credit - that beating heart that sustains the US economy - scarce...

... while on the other, demand for credit - a function of soaring interest rates - also collapsed.

But where is the evidence, the skeptics asked, and rightfully so: after all, the recent monthly consumer credit reports showed near record increases in both revolving (credit card) and non-revolving (student and auto loan) credit.

We didn't have long to wait for Exhibit A that the US consumer appears to have finally hit a brick wall.

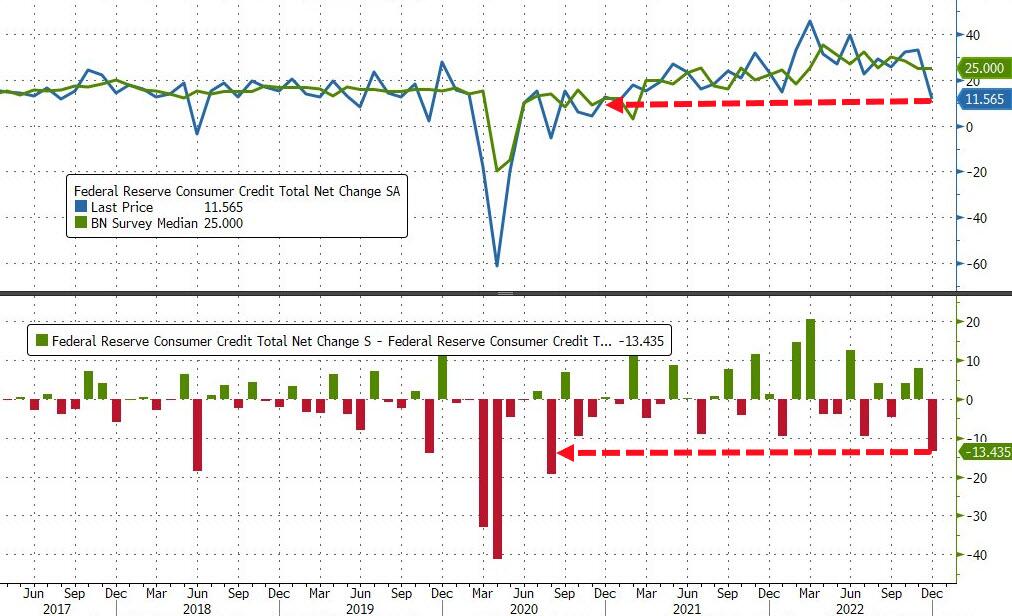

Late on Tuesday, the Fed published the latest, December consumer credit report, which found that in December, total US consumer credit increased by just $11.565Bn, which was not only a huge, 65% drop from November's upward revised $33.1Bn print, but also a huge, 50%+ miss relative to consensus expectations of $25BN, the biggest miss since August 2020!

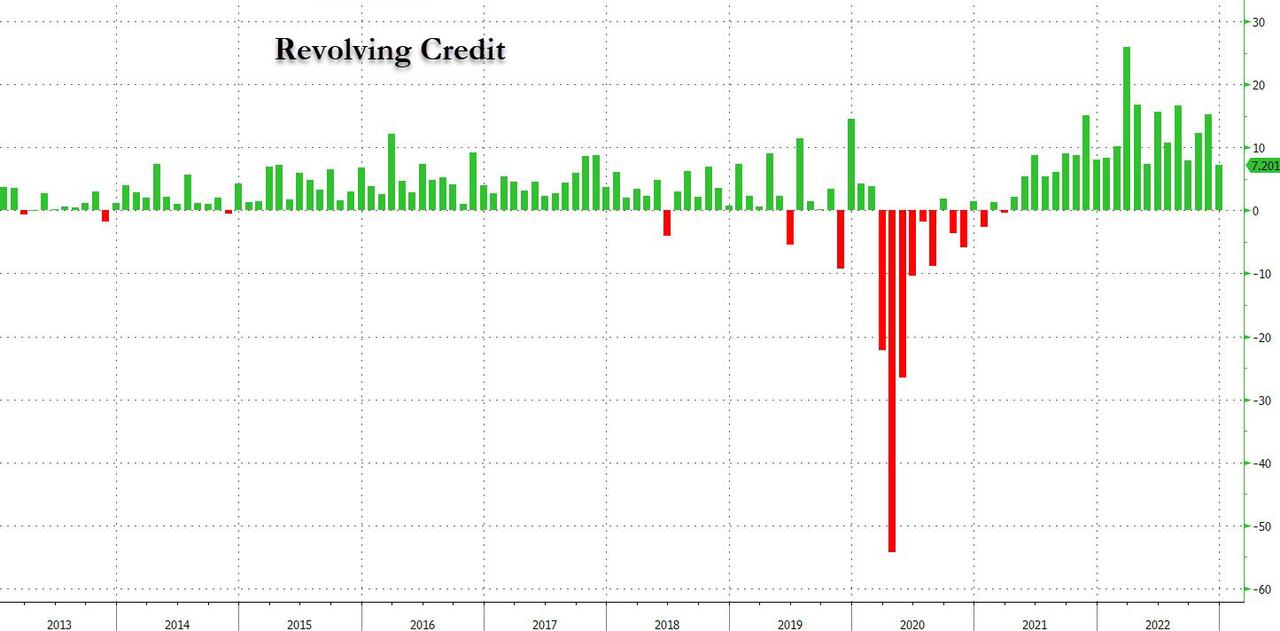

What caused the sharp slowdown in consumer credit which has traditionally increased by anywhere between $20BN and $30BN, come rain or shine? Well, there was a sharp slowdown in revolving, or credit card debt, which increased just $7.2BN in Dec, a drop of more than half vs the revised November print of $15.3BN...

... but the real driver behind the shocking hit was non-revolving credit, which rose by just $4.4 BN, a huge drop compared to the $17.8BN in November, and the $16.8BN LTM average!

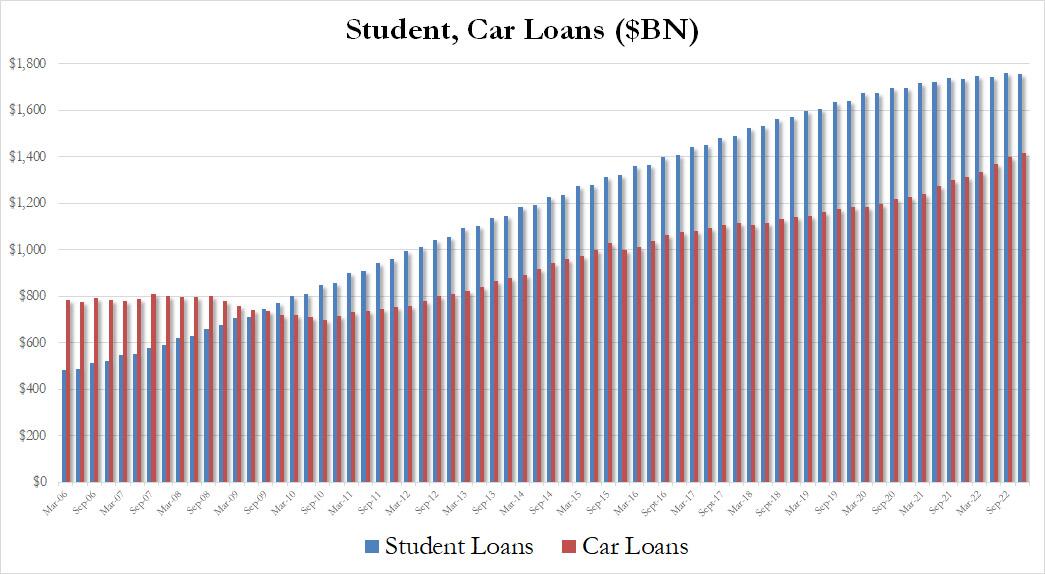

Drilling a bit deeper into this number, we find that the non-revolving slowdown was largely due to big slowdown in student loans, which actually contracted by $4.5BN in Q4, and increased just $23.8BN in 2022, even as auto loans continued to grow apace, and increased by $18BN in Q4, and a record $101BN in 2022.

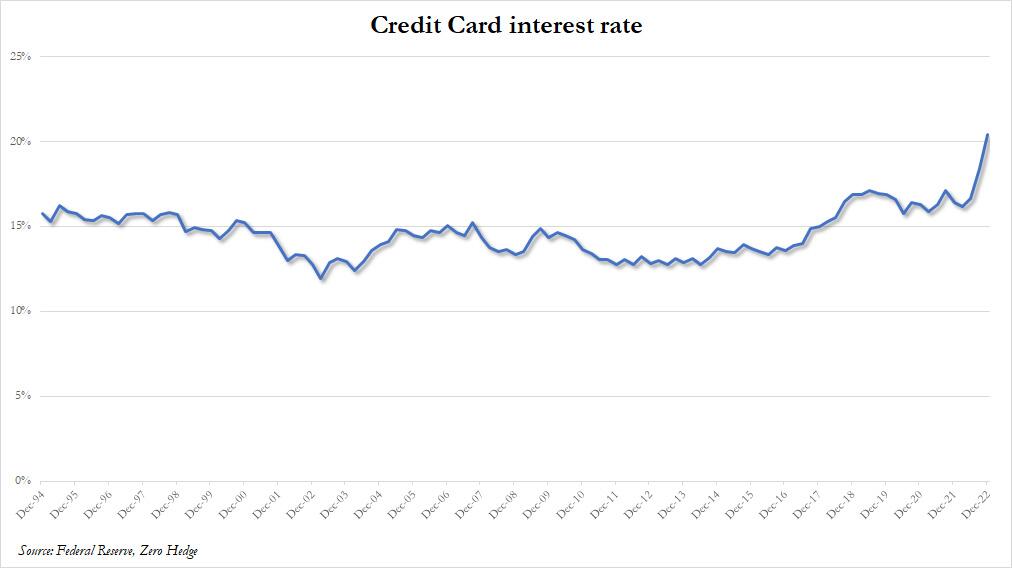

Finally, for those asking if the surge in interest rates in Q3 and Q4 had anything to do with it, the answer is a resounding yes: as of Dec 2022, the average credit card rates according to the Fed, was 20.40%, the highest on record in the Fed's database.

Bottom line is simple: while US savings (especially excess covid savings) were spent long ago and flatlined near record lows in recent months, it was all up to credit cards and other sources of (repurposed) credit - like pretending one's student loans are actually going to, you know, studying when instead they were used to buy iPhones, TVs, booze and onlyfans subs - to drive consumers.

However, the recent surge in rates has meant that even the indomitable US addiction to credit may be coming to an end, and the result is a sharp slowdown in credit-funded purchases, alongside an upward inflection in savings as US consumers are once again realizing the good old stimmy days are gone and more money has to be set side, and thus not spent. And since the US consumer is 70% of US GDP, this may be the clearest sign yet that 2023 GDP is about to hit a similarly sized brick wall. Which is great news for the Fed: after all, a recession is precisely what Powell wanted... and is about to get it.

https://ift.tt/CXwYUgv

from ZeroHedge News https://ift.tt/CXwYUgv

via IFTTT

0 comments

Post a Comment