Black Gold, Bond Yields, & The Buck Tumble Amid Macro Miasma

Weak European retail sales overnight (worse then expected decline), Ugly mortgage apps data (very bad news), Dismal jobs data (bad news but wage growth slowing), Strong factory orders (good news, thanks to war), Disappointing Services surveys (with stagflationary signals), and Disastrous gasoline demand (seasonally lowest since 1997). Hard data keeps falling as soft data holds all the hope...

Source: Bloomberg

Not much to cheer on the soft-landing-believers and as such, rate-change expectations slipped (dovishly) lower...

Source: Bloomberg

But it was oil that made the headlines as OPEC+'s JMMC reaffirmed their planned production goals for the rest of the year and economic malaise out-feared supply tightness. WTI collapsed almost 5%, dropping back below $85. This is the biggest drop in oil since last September UK gilt implosion contagion...

...testing its 50DMA ($84.86)...

Source: Bloomberg

As soaring pump prices appear to have punctured the strong consumer narrative as gasoline demand collapsed (to its lowest since 1997 for this time of year)...

Source: Bloomberg

And the gasoline crack has all but collapsed (but jet fuel and diesel still paying well)...

Source: Bloomberg

And oil volatility is dragging volatility higher across all the other asset classes...

Source: Bloomberg

Just one more thing, as we noted above, the last time oil dropped like this, UK gilts imploded on the mini-budget fiasco which sent sterling to a 37 year low and multiple UK financial institutions were on the verge of blowing up (the BOE restarted QE). Who is blowing up today?

Source: Bloomberg

Treasury yields plunged (for a change) with the short-end outperforming, 2Y Yields down 10bps on the day (biggest drop since August), and down 14bps from intraday highs...

Source: Bloomberg

Which steepened the yield curve (2s30s) further...

Source: Bloomberg

The relationship between 2Y Yields and oil has been 'complicated' recently but today it was one-way traffic...

Source: Bloomberg

While the absolute spread between US and Japan 10-year yields has ballooned to more than 400bps (holding near levels not seen since 2001), when adjusted for the JPY-hedging costs, USTs are at their most expensive for Japanese investors since 2000 (though we note that the last few weeks have seen the richness relived a little as UST yields have soared). Across the pond, German investors can earn 12bps over Bunds (hedged), meaning there is an incentive for them to be buying USTs (from the Japanese maybe?)...

Source: Bloomberg

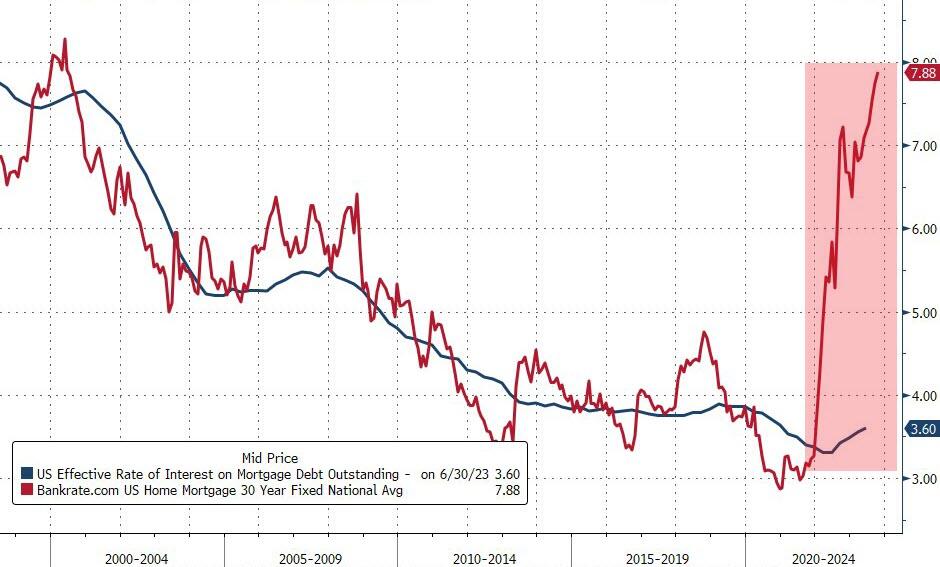

Mortgage rates just won't stop, now at multi-decade highs and massively decoupled from the rate at which the average homeowner's mortgage is currently set at...

Source: Bloomberg

Most notably - thanks in large part to QT - the mortgage spread to 10Y TSY is extremely high (Lehman and COVID lockdown crisis highs)...

Source: Bloomberg

Breakevens are diverging aggressively with short-dated inflation expectations at their lowest since Dec 2020 while longer-dated BEs are at the highest in a year...

Source: Bloomberg

Bond vol is now notably higher than equity vol...

Source: Bloomberg

And after all that, US equity indices were mixed on the day with Nasdaq soaring and Small Caps lagging, just red after ramping up to unch.

Notably, Bespoke pointed out that the S&P has made lower lows on 33 of the past 50 trading days.

The dollar ended marginally lower, much less impacted than bonds or crude...

Source: Bloomberg

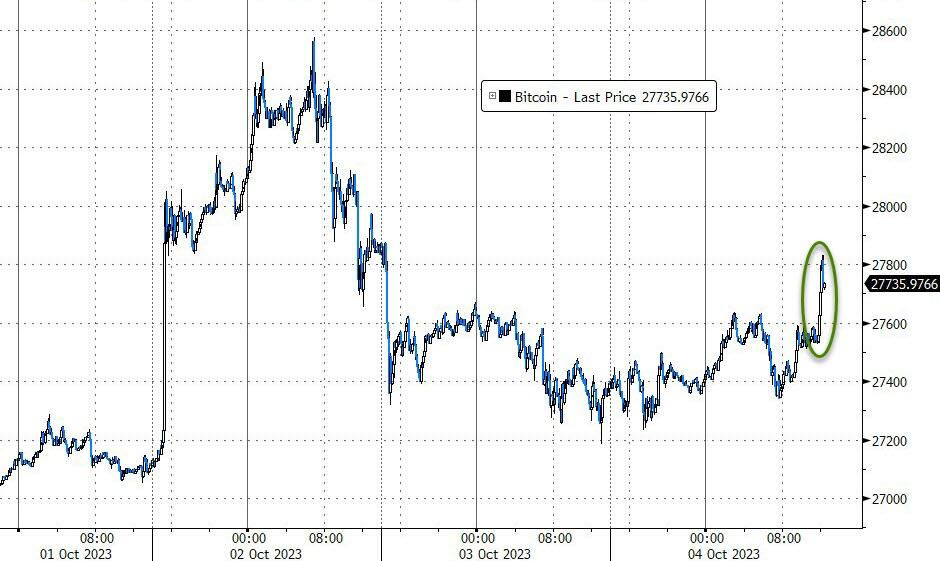

Bitcoin managed modest gains on the day...

Source: Bloomberg

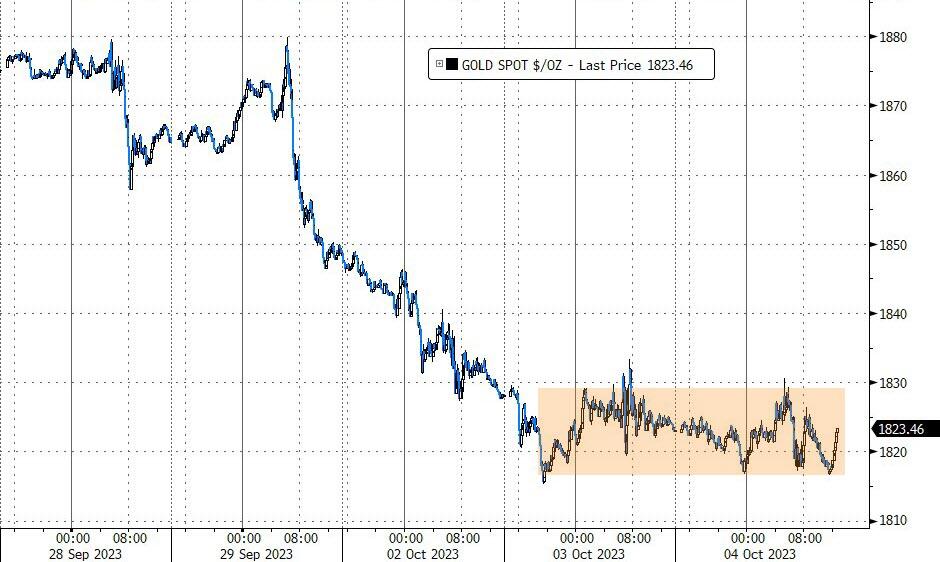

Gold went nowhere, holding above $1800 and the March dip lows...

Source: Bloomberg

Finally, if financial conditions hold this tightness, we can't help but think the AI-bubble won't be able to keep Nasdaq so rich relative to Small Caps...

Source: Bloomberg

And we're seeing echoes of 1987 (and 1929) being MSG'd across desks... for stocks...

Source: Bloomberg

...And bonds...

Source: Bloomberg

Albert Edwards had some thoughts:

The equity market’s current resilience in the face of rising bond yields reminds me very much of events in 1987, when equity investors’ bullishness was eventually squashed.

And in a further parallel, currency turbulence in 1987 played a key role in exacerbating recession worries for an equity market priced for the start of a new economic cycle.

Just like in 1987, any hint of recession now would surely be a devastating blow to equities.

Brace!

https://ift.tt/xN0HVQv

from ZeroHedge News https://ift.tt/xN0HVQv

via IFTTT

0 comments

Post a Comment