Stocks Erase Losses As Bonds Flatline, Oil Slumps Ahead Of Friday's Jobs Report

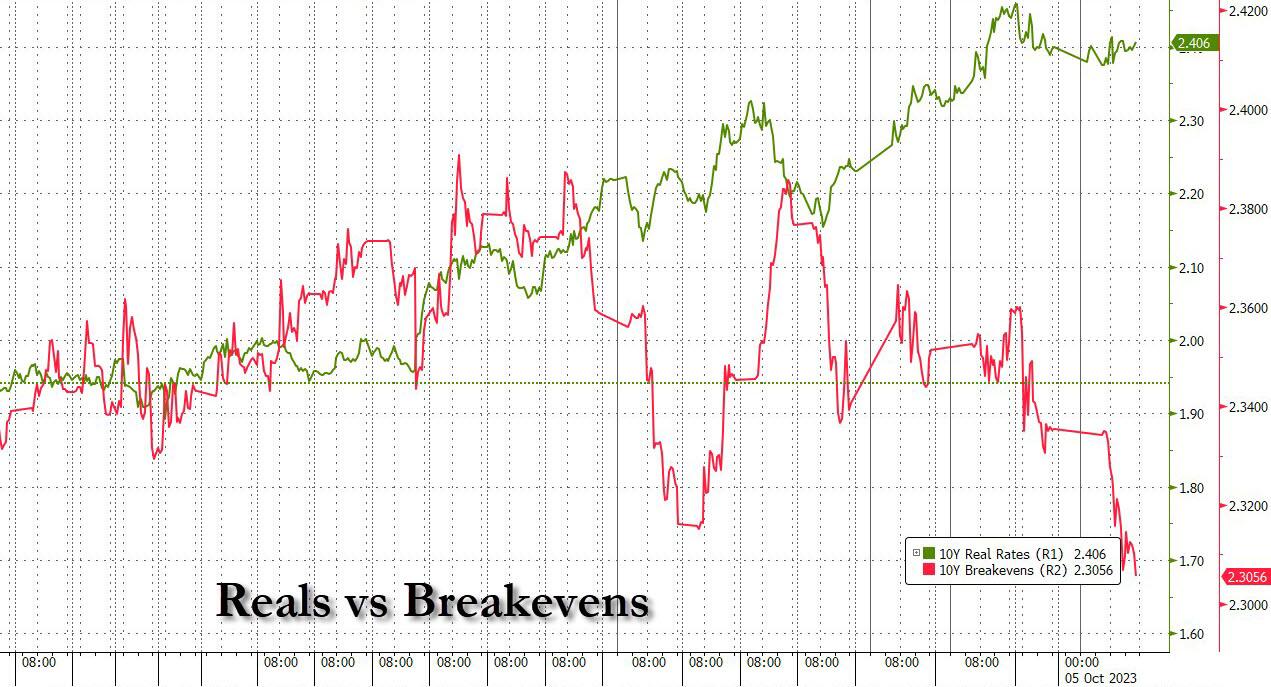

After a chaotic Tuesday and a Wednesday which Rabobank's Michael Every said was "Chaos On A Trampoline On Drugs", Thursday proved to be a rather calm day, in which 10Y rates did nothing for a welcome change after blowing out by almost 60 bps in the past two weeks, a move which the same Every said ahd made the world's most liquid security trade like a penny stock...

... which in turn was due to the plunge in oil, because as Every once again explained, oil "is still the lifeblood of the global economy, and again one perhaps dodgy data point from increasingly erratic US sources saw a staggering decline of $5 in one day. That, more than anything, is what brought down bond yields, not the ADP."

Indeed, looking at the component of the notional rate, Real rates were practically unchanged at the upper end of the range, while Breakevens tumbled, driven by the move in oil which they track tick for tick.

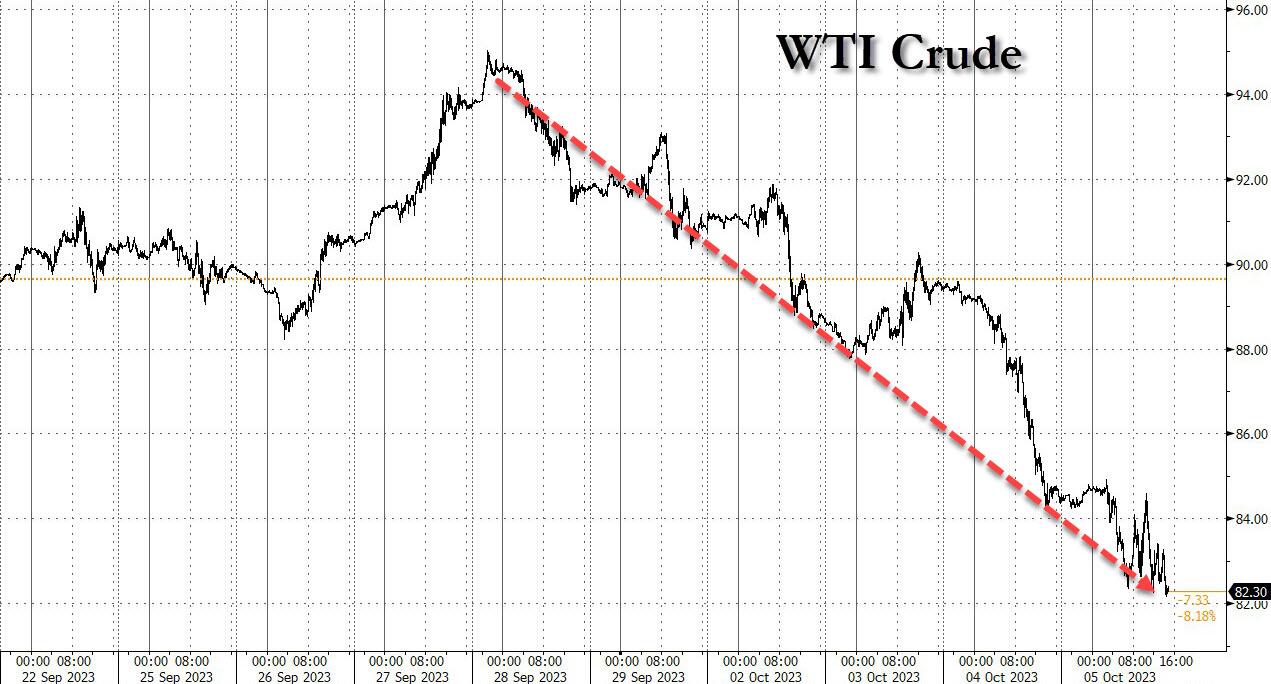

Going back to oil, the move in the past week has been an absolute clownshow, with WTI rising above $95 last Thursday only to plunge to $82 today, after crashing by more than 5% yesterday, the biggest one day move since last September's mini-budget freakout.

What was behind the plunge in oil? Here there are two camps on Wall Street, those who UBS' strategist Catherine Gordon, pretend they know the reason...

There are a few reasons I was hearing out there as to why oil has sold off so hard:

- Demand feels very shaky right now: Wednesday's Department of Energy data showed a large increase in US gasoline inventories and low implied demand. This, combined with recent weakness in refining margins, fueled demand concerns. This was on top of global broader market worries arising again around higher-for-longer global central bank policy;

- Extended / crowded positioning in oil: CTA allocations to oil that have risen to the highest level since 2018, while a Reuters column yesterday said that fund managers were net sellers for the first time in four weeks across the six most important petroleum-linked contracts last week. However, managers still added a net 16 mn barrels of long positions to WTI, driven by depleting inventories in Cushing; and

- Geopolitical concerns: Some folks were flagging a new report by Axios discussing a potential broad deal between the US and Saudi Arabia, including energy, possibly impacted sentiment too, even though such discussions had been reported earlier.

.... and then those who like Rabobank's Michael Every admit they have no idea:

So what actually happened? First, I don’t know. Second, nobody knows. That’s how markets work. We can all write clever analytical notes after the fact, but given we can’t write them in advance of facts tells you something about just how good our methodologies actually are.

To my mind, what we just saw speaks to the fact that with current volatility, market liquidity may have been lower than normal; that bond positioning had switched to net short from net long; that we may have seen intervention from a central bank (and the list of potential offenders is short, and starts with ‘B’); and that this required immediate short covering. Then the data gave some cover to ‘reassess’ a position they had been so sure of hours earlier.

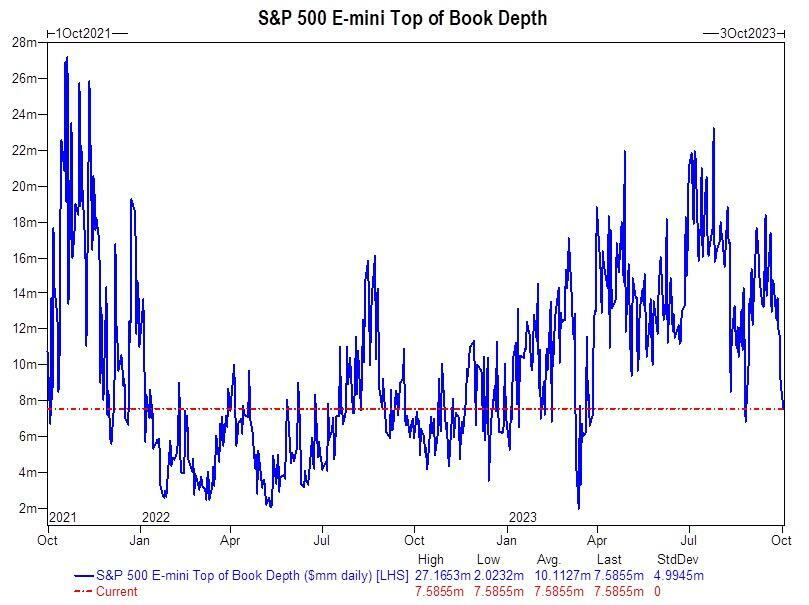

He's correct, of course, because as Goldman's Scott Rubner pointed out two days ago, "S&P 500 top book liquidity is currently $7.5M, or the ability to move risk quickly. This is a decline of -50% in the past 1 week, last week top of book was $15M."

Meanwhile, now that systematic funds (mostly CTAs) are done selling (with risk parity funds today also quiet thanks to the end of the bond liquidation) and are actually looking to buy back once volatility eases...

... stocks managed to contain the recent rout, barely budging after yesterday's reversal...

... in part thanks to a return of one key intraday supporter of risk: the 0DTE bid. Indeed, as shown below, despite some selling early in the session, 0DTE delta flow was bullish from the start, and helped stabilize and then push stocks higher for much of the session...

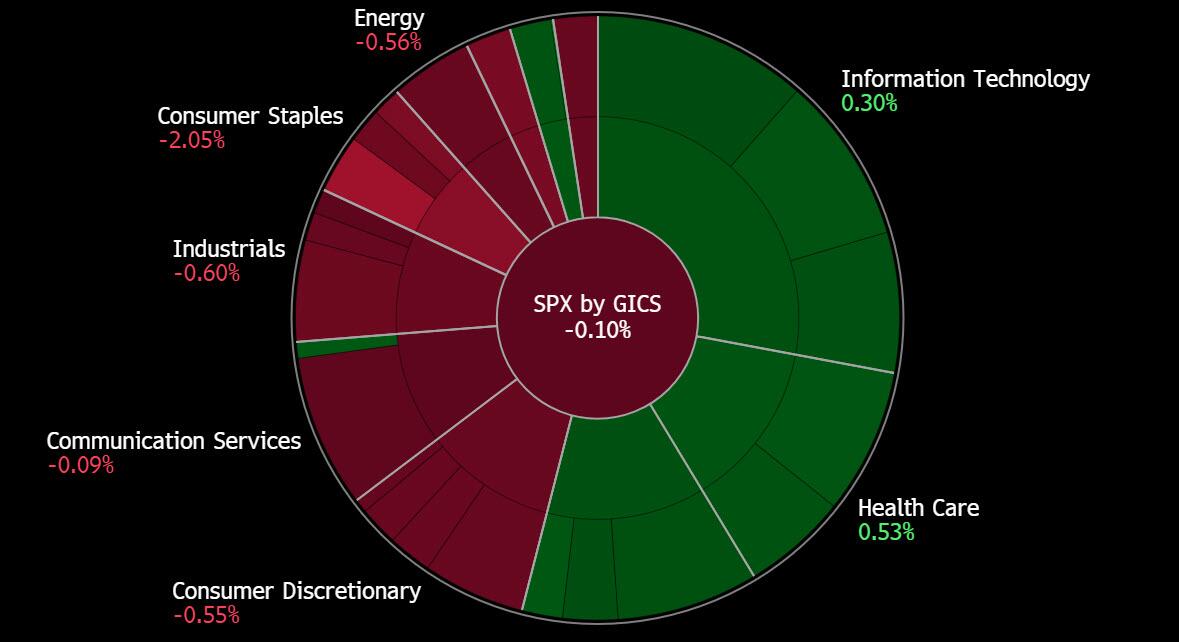

... even if the buying was anything but uniform with Energy and builders worst, while the bank index trading best despite an analysis by DB according to which banks stand to lose $140BN in unbooked losses in Q2.

There may be another reason why stocks barely budged today (spoos closed just barely in the red): tomorrow is payrolls day, and the day before the jobs report stocks usually avoid too much volatility. That said, unless we get a huge miss and drop tomorrow, it's difficult to see how stocks will how the S&P will be able to rise 0.7% on Friday and undo what is set to be yet another weekly drop for stocks, the fifth in a row, and the longest such stretch since May 2022.

https://ift.tt/J13TNnw

from ZeroHedge News https://ift.tt/J13TNnw

via IFTTT

0 comments

Post a Comment