Retired Or Retiring Soon? Yes, Worry About A Correction

Authored by Lance Roberts via RealInvestmentAdvice.com,

When I was growing up, my father used to tell me I should “never take advice from anyone who hasn’t succeeded at what they are advising.”

The most truth of that statement is found in the financial press, which consists mostly of people writing articles and giving advice on topics where they have little experience, and in general, have achieved no success.

The best example came last week in an email quoting:

“You recently suggested that you took profits from your portfolios; however, I read an article saying retirees shouldn’t change their strategies. ‘If you’ve got a thoughtful financial plan and a diversified investment portfolio, the general rule is to leave everything alone.'”

This seems to be an entirely different approach to what you are suggesting. Also, since corrections can’t be predicted, it seems to make sense.”

One of the biggest reasons why investors consistently underperform over the long-term is due to flawed investment advice.

Let me explain.

Corrections & Bear Markets Matter

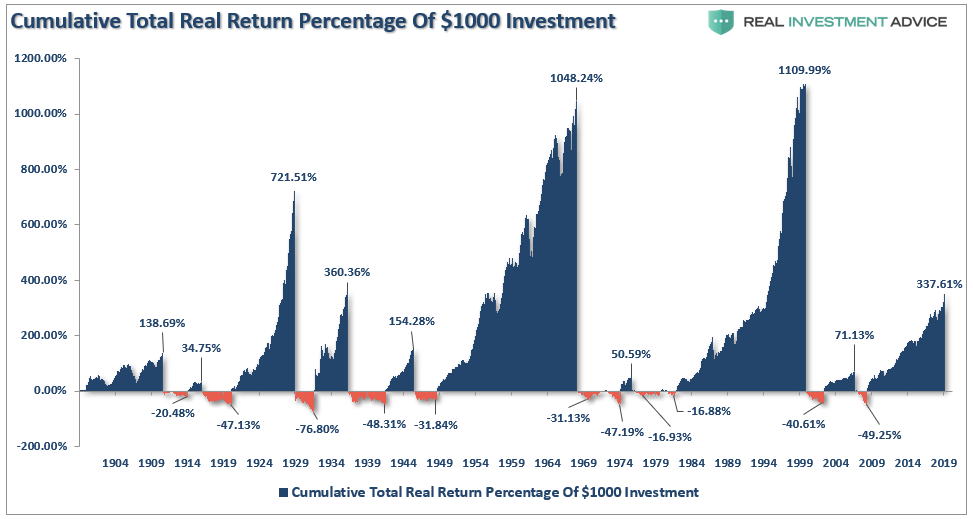

It certainly seems logical, by looking the 120-year chart of the market, that one should just stay invested regardless of what happens. Eventually, as the financial media often suggests, the markets always get back to even. One such chart is the percentage gain/loss chart over the long-term, as shown below.

This is one of the most deceptive charts an advisor can show a client, particularly one that is close to, or worse in, retirement.

The reality is that you DIED long before ever achieving that 8% annualized long-term return you were promised. Secondly, math is a cruel teacher.

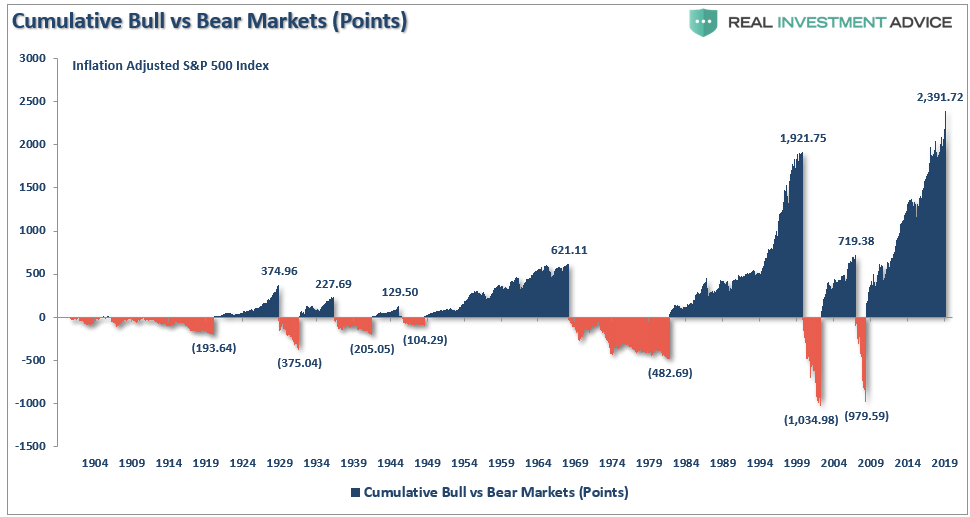

Visually, percentage drawdowns seem to be inconsequential relative to the massive percentage gains that preceded them. That is, until you convert percentages into points and reveal an uglier truth.

It is important to remember that a 100% gain on a $1000 investment, followed by a 50% loss, does not leave you with $1500. A 50% loss wipes out the previous 100% gain, leaving you with a 0% net return.

For retirees, this is a critically important point.

In 2000, the average “baby boomer” was around 45-years of age. The “dot.com” crash was painful, but with 20-years to go before retirement, there was time to recover. In 2010, following the financial crisis, the time to retirement for the oldest boomers was depleted, and the average boomer only had 10-years to recover. During both of these previous periods, portfolios were still in accumulation mode. However, today, only the youngest tranche of “boomers,” have the luxury of “time” to work through the next major market reversion. (This also explains why the share of workers over the age of 65 is at historical highs.)

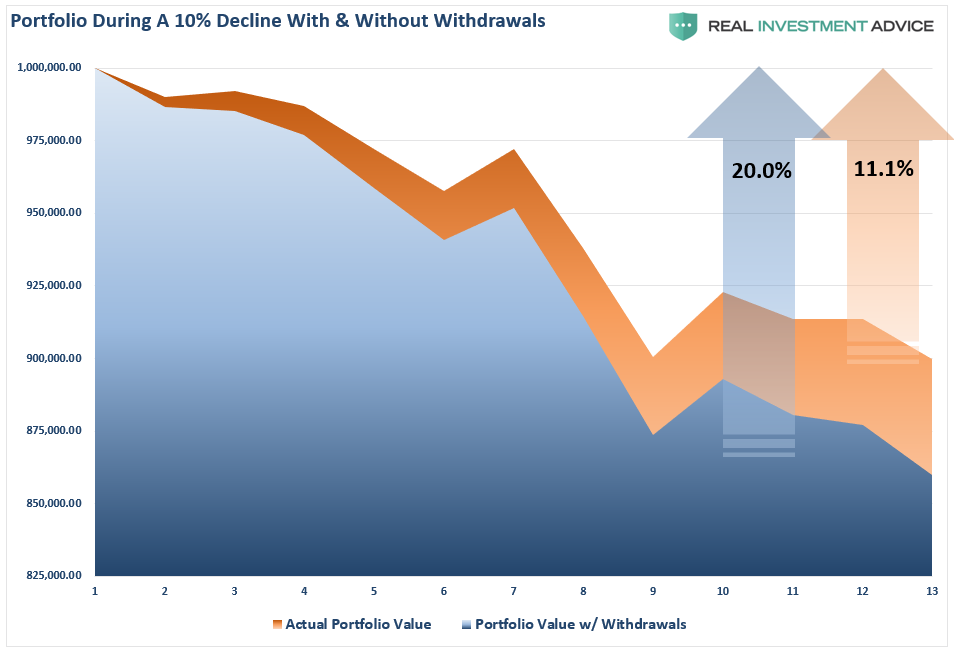

With the majority of “boomers” now faced with the implications of a transition into the distribution phase of the investment cycle, such has important ramifications during market declines. The following example shows a $1 million portfolio with, and without, an annualized 4% withdrawal rate. (We are going into much deeper analysis on this in a moment.)

While a 10% decline in the market will reduce a portfolio from $1 million to $990,000, when combined with an assumed monthly withdrawal rate, the portfolio value is reduced by almost 14%. This is the result of taking distributions during a period of declining market values. Importantly, while it ONLY requires a non-withdrawal portfolio an 11.1% return to break even, it requires nearly a 20% return for a portfolio in the distribution phase to attain the same level.

Impairments to capital are the biggest challenges facing pre- and post-retirees currently.

This is an important distinction. Most articles written about retirees, or those ready to retire, is an unrealized assumption of an indefinite timeline.

While the market may not be different than it has been in the past. YOU ARE!

Starting Valuations Matter

As I have discussed previously, without understanding the importance of starting valuations on your investment returns, you can’t understand the impact the market will have on psychology, and investor behavior.

Over any 30-year period, beginning valuation levels have a tremendous impact on future returns.

As valuations rise, future rates of annualized returns fall. This should not be a surprise as simple logic states that if you overpay for an asset today, the future returns must, and will, be lower.

This is far less than the 8-10% rates of return currently promised by the Wall Street community. It is also why starting valuations are critical for individuals to understand when planning for both the accumulation and distribution, phases of the investment life-cycle.

Let’s elaborate on our example above.

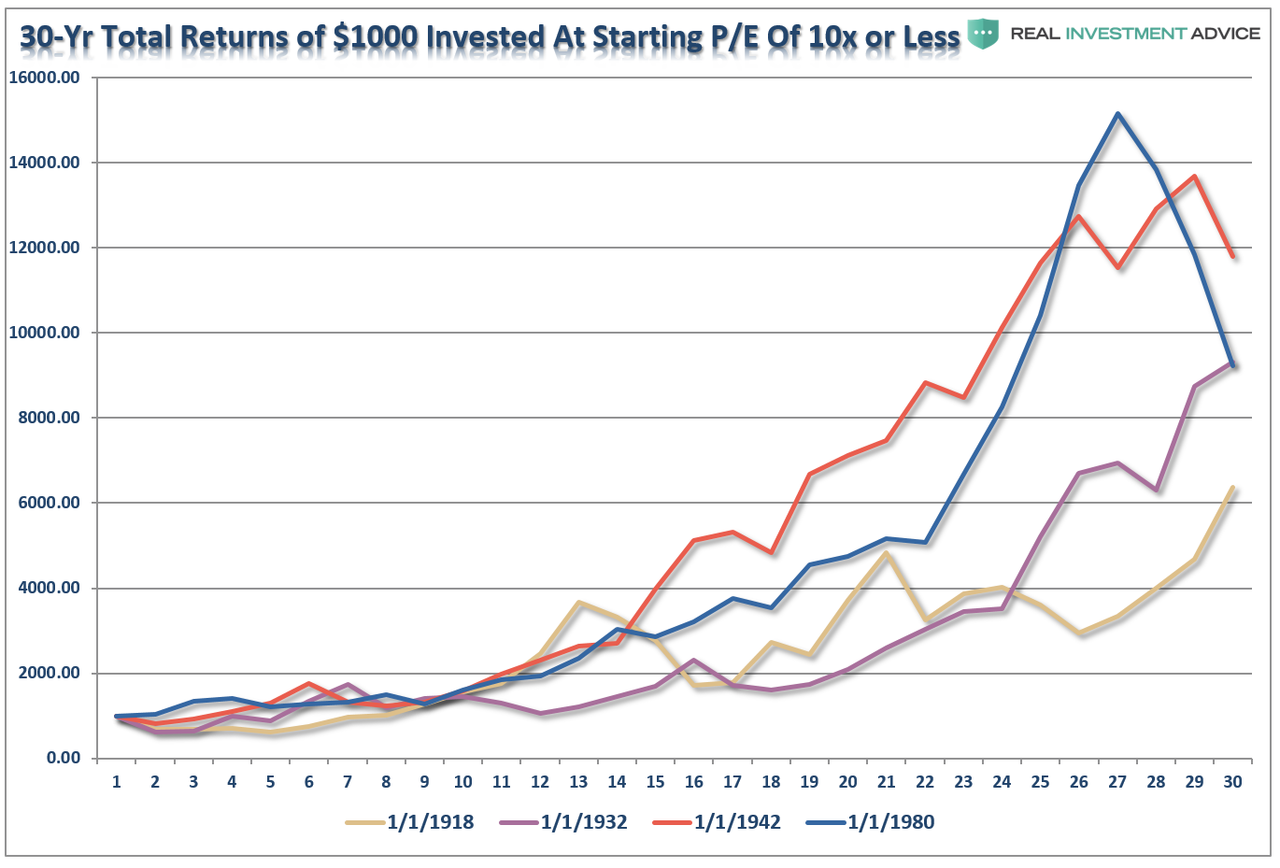

We know that markets go up and down over time, therefore when advisors use “average” or “annualized” rates of return, results often deviate far from reality. However, we do know from historical analysis that valuations drive forward returns, so using historical data, we calculated the 4-periods where starting valuations were either above 20x earnings, or below 10x earnings. We then ran a $1000 investment going forward for 30-years on a total-return, inflation-adjusted, basis.

The results were not surprising.

At 10x earnings, the worst performing period started in 1918 and only saw $1000 grow to a bit more than $6000. The best performing period was actually not the screaming bull market that started in 1980 because the last 10-years of that particular cycle caught the “dot.com” crash. It was the post-WWII bull market that ran from 1942 through 1972 that was the winner. Of course, the crash of 1974, just two years later, extracted a good bit of those returns.

Conversely, at 20x earnings, the best performing period started in 1900, which caught the rise of the market to its peak in 1929. Unfortunately, the next 4-years wiped out roughly 85% of those gains. However, outside of that one period, all of the other periods fared worse than investing at lower valuations. (Note: 1993 is still currently running as its 30-year period will end in 2023.)

The point to be made here is simple and was precisely summed up by Warren Buffett:

“Price is what you pay. Value is what you get.”

To create our variable return assumption model, we averaged each of the 4-periods above into a single total return, inflation-adjusted, index. We could then see the impact of $1000 invested in the markets at both valuations BELOW 10x trailing earnings, and ABOVE 20x. Investing at 10x earnings yields substantially better results.

Starting Valuations Are Critical To Withdrawal Rates

With a more realistic return model, the impact of investing during periods of high valuations becomes more evident, particularly during the withdrawal phase of retirement.

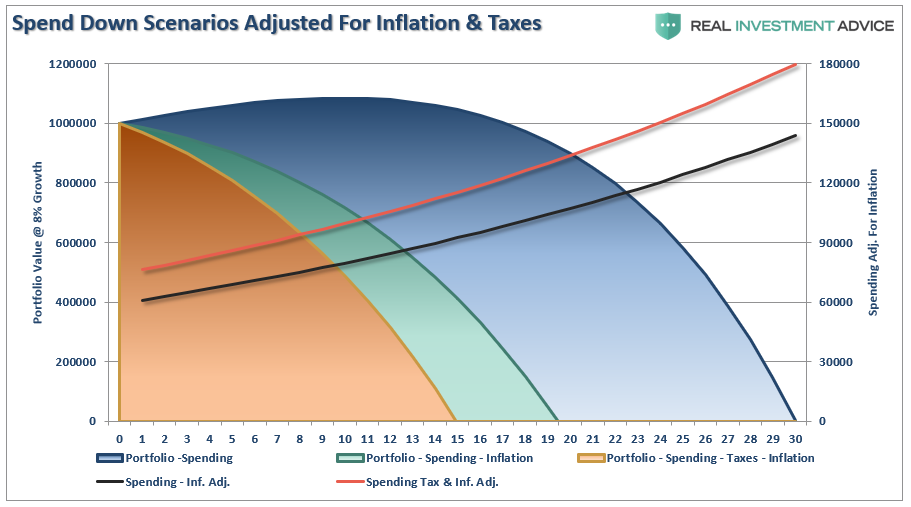

Let’s start with our $1 million retirement portfolio. The chart below shows various “spend down” assumptions of a $1 million retirement portfolio adjusted for an 8% annualized return, the impact of inflation at 3%, and the effect of taxation on withdrawals.

By adjusting the annualized rate of return for the impact of inflation and taxes, the life expectancy of a portfolio grows considerably shorter. Unfortunately, this is what “really happens” to investors over time, but is never discussed in mainstream analysis.

To understand “real outcomes,” we must adjust for variable rates of returns. There is a significant difference between 8% annualized rates of return and 8% real rates of return.

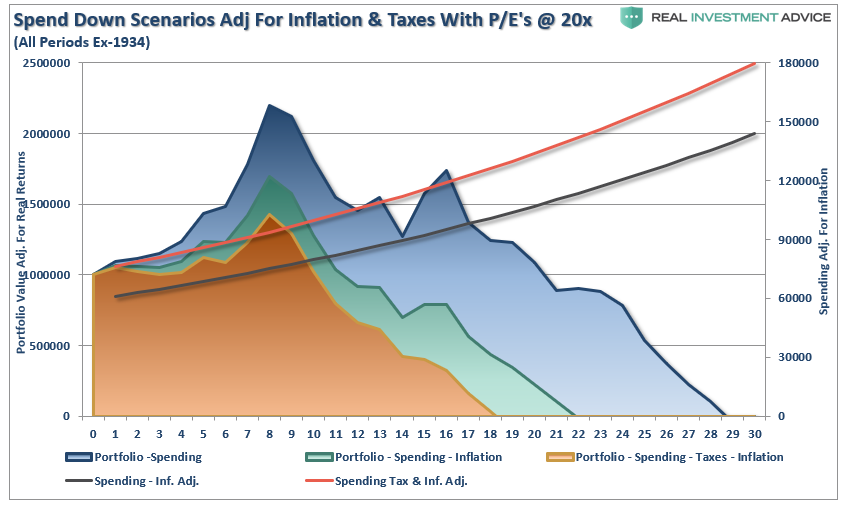

When we adjust the spend down structure for elevated starting valuation levels, and include inflation and taxes, a far different, and less favorable, outcome emerges. Retirees will run out of money not in year 30, but in year 18.

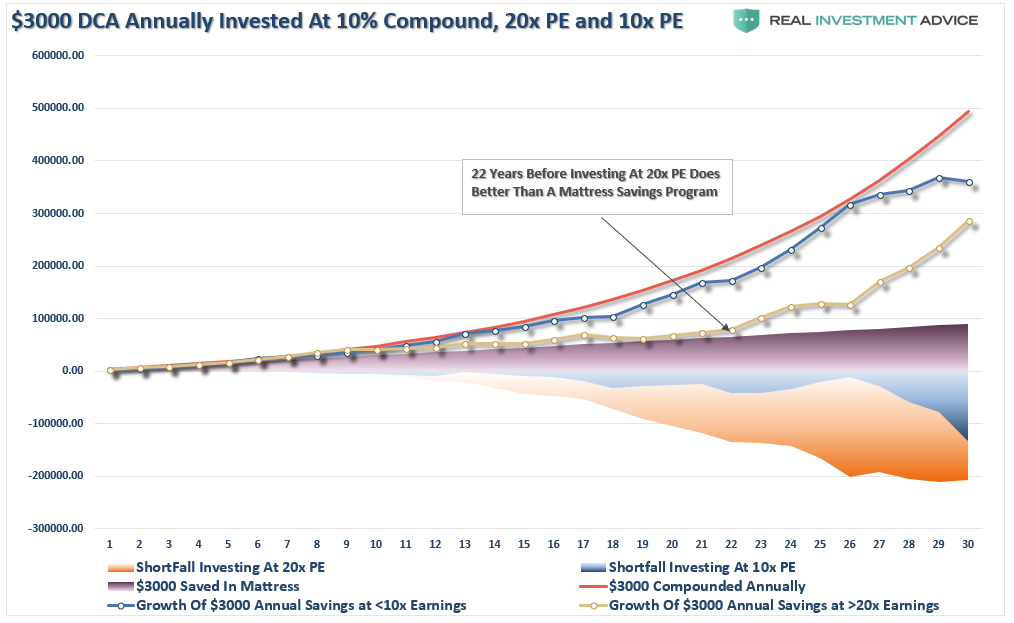

With this understanding, let’s revisit what happens to “buy and hold” investors over time. The chart below shows $3000 invested annually into the S&P 500 inflation-adjusted, total return index at 10% compounded annually, and both 10x and 20x valuation starting levels. I have also shown $3000 saved annually and “stuffed in a mattress.”

The red line is 10% compounded annually. While you don’t get compounded returns, it is there for comparative purposes to the real returns received over the 30-year investment horizon starting at 10x and 20x valuation levels. The shortfall between the promised 10% annual rates of return and actual returns are shown in the two shaded areas. In other words, if you are banking on some advisor’s promise of 10% annual returns for retirement, you aren’t going to make it.

Questions Retirees Need To Ask About Plans

What this analysis reveals is that “retirees” SHOULD be worried about bear markets.

Taking the correct view of your portfolio, and the risks being undertaken is critical when entering the retirement and distribution phase of the portfolio life cycle.

Most importantly, when building and/or reviewing your financial plan, these are the questions you must ask and have concrete answers for:

-

What are the expectations for future returns going forward given current valuation levels?

-

Should the withdrawal rates be downwardly adjusted to account for potentially lower future returns?

-

Given a decade long bull market, have adjustments been made for potentially front-loaded negative returns?

-

Has the impact of taxation been carefully considered in the planned withdrawal rate?

-

Have future inflation expectations been carefully considered?

-

Have drawdowns from portfolios during declining market environments, which accelerates principal bleed, been considered?

-

Have plans been made to harbor capital during up years to allow for reduced portfolio withdrawals during adverse market conditions?

-

Has the yield chase over the last decade, and low interest rate environment, which has created an extremely risky environment for retirement income planning, been carefully considered?

-

What steps should be considered to reduce potential credit and duration risk in bond portfolios?

-

Have expectations for compounded annual rates of returns been dismissed in lieu of a plan for variable rates of future returns?

If the answer is “no” to the majority of these questions. then feel free to contact one of the CFP’s in our office who take all of these issues into account.

With debt levels rising globally, economic growth on the long-end of the cycle, earnings growth weak, valuations high, and potential risk of a recession, the uncertainty of retirement plans has risen markedly. This lends itself to the problem of individuals having to spend a bulk of their “retirement” continuing to work.

Yes, not only should you worry about bear markets, you should worry about them a lot.

https://ift.tt/2TVlL7Q

from ZeroHedge News https://ift.tt/2TVlL7Q

via IFTTT

0 comments

Post a Comment