Banks Report Tighter Standards, Weaker Loan Demand But Some Improvement As Financial Conditions Ease

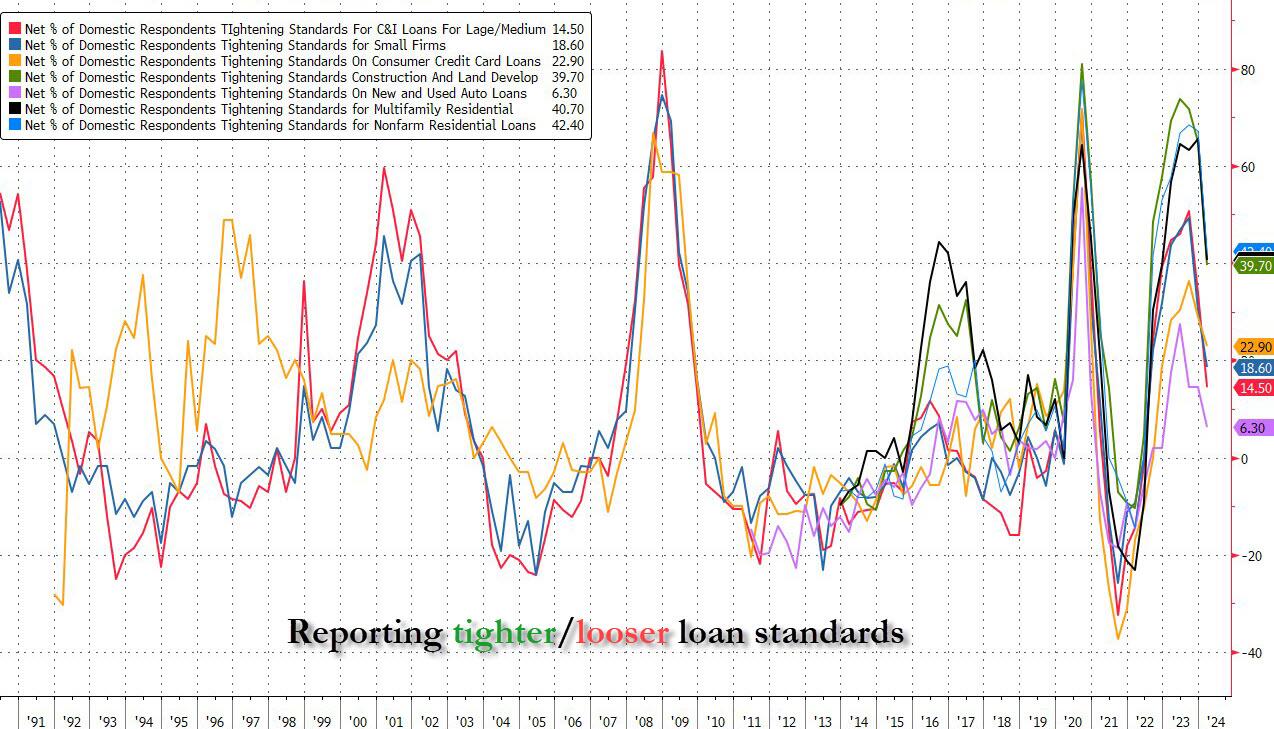

The last time we looked at the senior loan officer survey in November, we found "tighter standards and weaker demand for commercial and industrial (C&I) loans to firms of all sizes over the third quarter" in addition to tighter standards and less demand for most other loan categories. So fast forward to today when the latest closely watched SLOOS report for Q1 was published, and which found that, once again banks "reported tighter standards and weaker demand for commercial and industrial (C&I) loans to firms of all sizes over the fourth quarter. Furthermore, banks reported tighter standards and weaker demand for all commercial real estate (CRE) loan categories."

For loans to households, banks "reported that lending standards tightened across all categories of residential real estate (RRE) loans other than government residential mortgages and government-sponsored enterprise (GSE)-eligible residential mortgages, for which standards remained basically unchanged." Meanwhile, demand weakened for all RRE loan categories.

In addition, banks reported tighter standards and weaker demand for home equity lines of credit (HELOCs). Moreover, for credit card, auto, and other consumer loans, standards reportedly tightened, and demand weakened on balance.

In short, less demand, tighter supply.

The silver lining is that while banks reported having tightened lending standards further for most loan categories in Q4, "lower net shares of banks reported tightening lending standards than in Q3 across all loan categories." And for those who bother to look at the actual numbers, only 14.5% of respondents reported tightening standards for large/medium sizes commercial loans, the lest since Q3 2022. In other words, just like inflation where prices are still going up but not at the previous torrid pace, so here standard continue to tighten, but ever so slower.

Same thing with demand: while demand remained negative for all loan types, the rate of contraction is moderating a bit, which while a good sign, is a far cry from actually growing loan demand which we haven't seen in over a year... because 4% GDP (according to the Atlanta Fed GDPNow)...

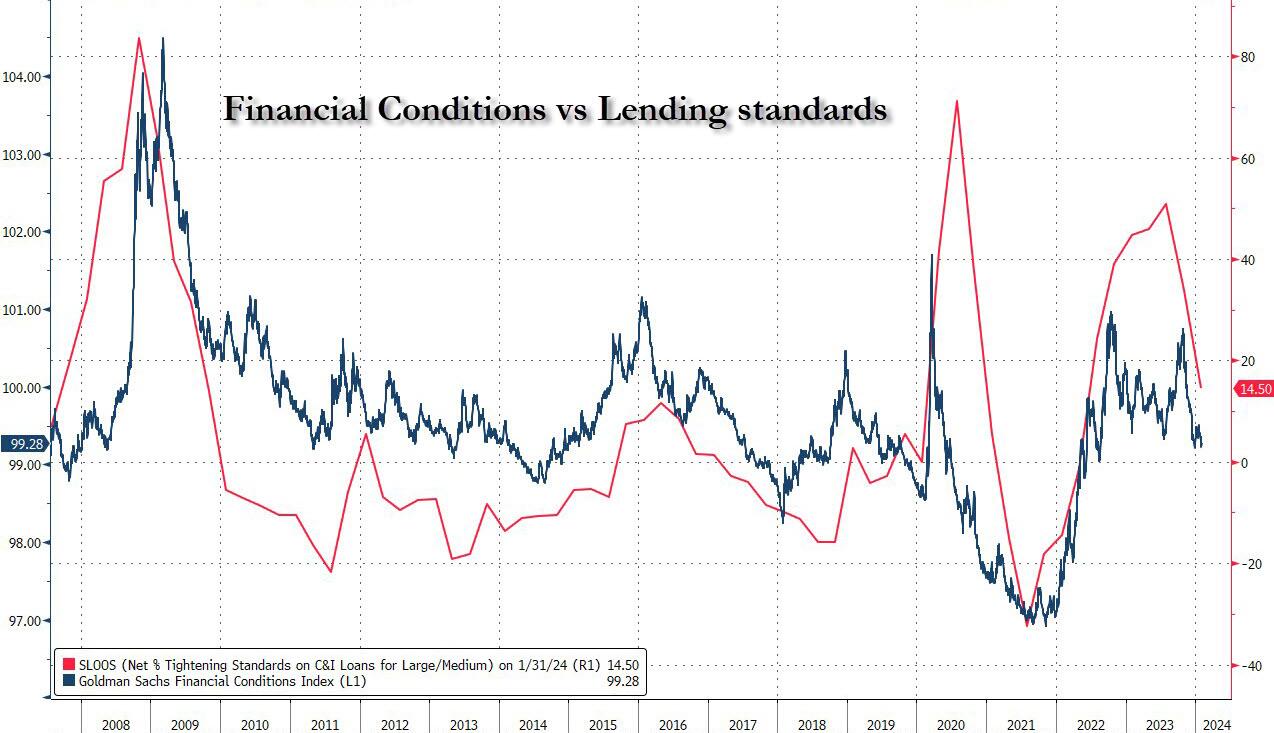

And yes, for those wondering, loan tightness is almost entirely a function of financial conditions: as the next chart shows, financial conditions have become far less tight in the past two quarter, tracking the sharp easing in financial conditions.

The January SLOOS also included a set of special questions inquiring about banks’ expectations for changes in lending standards, borrower demand, and loan performance over 2024. Banks, on balance, reported expecting lending standards to remain basically unchanged for C&I and RRE loans, but to tighten further for CRE, credit card, and auto loans. In addition, banks reported expecting loan demand to strengthen across all loan categories, and loan quality to deteriorate across most loan types.

In other words, banks anticipate further tightening lending standards across most categories, even as consumer fight with each other for what little loan availability exists (all of this, of course, is moot once the next round of the regional bank crisis arrive in March when the Fed's BTFP program expires, and when most lending once again grinds to a halt).

Source: Fed

https://ift.tt/LhtO7qQ

from ZeroHedge News https://ift.tt/LhtO7qQ

via IFTTT

0 comments

Post a Comment