The final day of April was really ugly: ECI way hotter than expected (spooked markets), Case-Shiller home prices soared far more than expected (spooked markets more), Chicago PMI puked (while prices paid increased), Consumer Confidence crashed, and Dallas Fed Services slumped... all of which left stocks, bonds, gold, crude oil, and bitcoin all languishing into month-end while the dollar rallied.

Stocks puked into the month-end close today ahead of AMZN earnings...

April was a disaster from a macro perspective...

Source: Bloomberg

...with soft survey data collapsing while 'hard' data limped modestly higher...

Source: Bloomberg

...and worse still growth surprises slumped as inflation surprises soared - screaming stagflation so loud no one could ignore it...

Source: Bloomberg

Against the backdrop of US 10Y yields up ~45 bps in the month of April...

Source: Bloomberg

... and the market taking another rate-cut off the board...

Source: Bloomberg

...price action in April is perhaps not overly surprising with Equities broadly lower, albeit, with NDX / Quality / Mag7 continuing to outperform.

Source: Bloomberg

Goldman's Peter Callahan notes that since 2006, the S&P 500 has fallen by an avg of 4% when real yields rose by more than 2 stdev in a month.

April was the first down-month for stocks since The Fed Pivot (Oct 2023). This was the worst month for The Dow since Sept 2022. Nasdaq suffered its worst month since Sept 2023.

Interestingly, while US majors and sectors were red (broadly speaking) in April, Chinese Internet stocks soared back to life (+9.5% vs US MegaCap -2%)...

Source: Bloomberg

Sectors were very mixed in April with Energy and Utilities outperforming (the latter on AI energy use, since its typical relationship to rates decoupled) and Real Estate lagged (along with Tech)...

Source: Bloomberg

The basket of Magnificent 7 stocks saw red in April for its first monthly loss since October and worst monthly loss since September. The last week has been tempestuous to say the least as TSLA (win), META (lose), MSFT and GOOGL (win) all hit...

Source: Bloomberg

Still, stocks have a long way to catch down to the new reality priced into the short-end of the bond market...

Source: Bloomberg

As we noted above, the TSY curve was up relatively uniformly on the month, but perhaps most notably was the 2Y yield which tested 5.00% numerous times and broke out today...

Source: Bloomberg

One more notable event in April was the tightening of financial conditions (admittedly only marginally), but definitely more what The Fed wants relative to the extreme 'easiness' that had been priced in after Powell's pivot...

Source: Bloomberg

The dollar rallied for the fourth month in a row with the big gains coming mid-month....

Source: Bloomberg

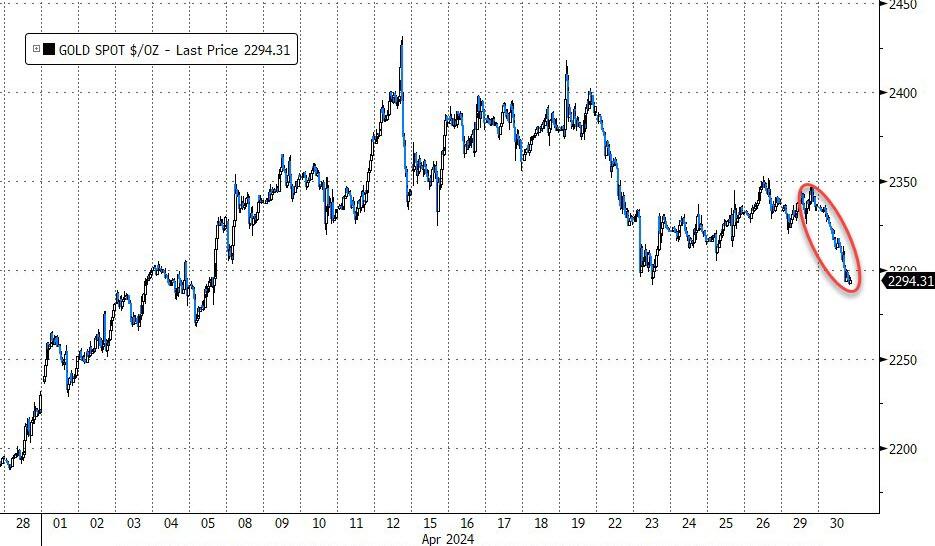

Despite taking a battering today, Gold managed solid gains on the month, topping $2400 at its record highs...

Source: Bloomberg

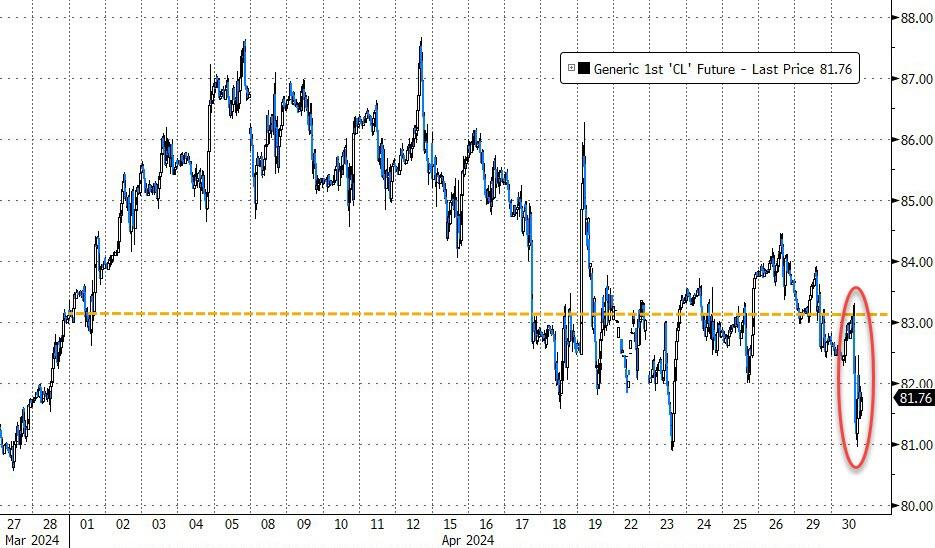

Oil prices ended the month marginally lower, thanks to today's selloff...

Source: Bloomberg

Copper was the outstanding commodity in April, soaring around 14% to two year highs with practically no drawdown as the reflation trade came back to life (on the back of AI demand)...

Source: Bloomberg

Bitcoin had an ugly month, down 15% after seven straight months of gains...

Source: Bloomberg

As BTC ETF flows started to ebb - Net Flows (including GBTC): April -$183mm, March +$4.62bn, February +$6.03bn, January +1.47bn...

Source: Bloomberg

Finally, the ultimate analog remains in play...

Source: Bloomberg

...with NVDA bouncing back, just like CSCO did.

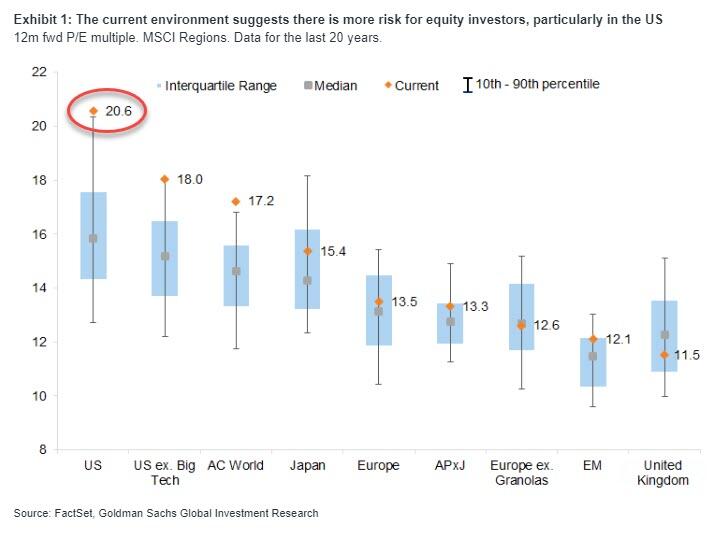

And bear in mind, as Goldman's Peter Oppenheimer points out, US equity market valuation is currently at an extreme level relative to history...

...also a condition that typically means higher rates weigh more heavily on stocks.

And while April showers are over...

The S&P 500's vol term structure suggests the storm is not over yet.

You realize, don’t you, that what’s going on in our country is the collapse not just of an empire, or an economy, but a comprehensive paradigm of human progress. The hallmark of post-war life in Western Civ was supposed to be a return to sanity after the mid-twentieth century fugue of mass psychotic violence. The wish for just and rational order was not entirely pretense. But that was then. Now that we are going medieval on ourselves, the not-so-ironic result will be our literally going medieval, sinking back into a pre-modern existence of darkness, superstition, and penury, grubbing for a mere subsistence in the shadow of scuffling hobgoblins, our achievements lost and forgotten.

What’s most appalling is that our governing apparatus is visibly willing that to happen. When Barack Obama warned America to not underestimate Joe Biden’s ability to fuck things up, was that some kind of joke? After all, it was Mr. Obama and his fellow blobsters — the cabal of Intel spooks, covert Marxist bureaucrats, lawfare ninjas, globalist megalomaniacs, post-liberal think tankers, weapons grifters, degenerate billionaires, and assorted mentally-ill camp followers — who inflicted Joe Biden on the body politic. And then ran him on the country like some demon algorithm designed to wreck the USA as fast as possible.

The source of anguish in all that is the struggle to understand why they would want that to happen. What debauched sense of history would drive anyone to such lunatic desperation? It’s a cliché now to say that the Democratic Party has turned its traditional moral scaffold upside down and inside out. It acts against the kitchen table interests of the working and middle classes. It’s against civil liberties. It demands mental obedience to patently insane policy. It’s avid for war, no matter how cruelly pointless. It’s deliberately stirring up racial hatred. It despises personal privacy. It feeds a rogue bureaucracy that has become a veritable Moloch, an all-devouring malevolent deity. And now, rather suddenly, it aligns itself with a faction that seeks to exterminate the Jews.

And how did the opposition to that epic divergence into bad faith turn so flabby? How did the Republican Party roll over and wheeze so feebly while the FBI ran amok swatting grandmothers in dawn raids, and the US attorney general made justice a whore, and a Republican Congress allowed the Frankenstein agency of Homeland Security to flood the country with its enemies and give them gobs of operational cash? If Mr. Trump was unappetizing to them as a leader, why were they unable to produce an alternative figure of standing and stature at least equally resolute? They look like traitors and cowards.

For the moment, the country lies mired, inert, and demoralized in the face of in those terrible mysteries. But events are still tending and the hidden hand of emergence still operates backstage, preparing surprises for us. You are necessarily aware that the center did not hold. It’s even hard to locate where the center used to be with the action so heavy on the far-out margins. You’re watching drag queens importune young children to shove all the Jews into the sea. And the kids are sitting next to their mommies. What happened to the mommies’ brains that permits them to think this spectacle is okay? How will the mommies ever get their minds right?

In some quarters, a great rage is building. Not a few resent the overthrow of common sense, common law, and common decency. You better believe they will be aiming to do something about it. They will stand up for their dignity, their culture, their history. Virtue isn’t dead; it’s just broke down on a lonely highway waiting to hitch a ride back to where the lights are still on. Don’t forget that this really is the land of the free and the home of the brave.

Meanwhile, prepare for action. It’s obvious that the enemies of the people don’t intend to rest. They are going to try to play out this string to the last move because otherwise a lot of them will be going to jail, or might even hang for their wickedness. Once they turned criminal, there was no turning back. They have dishonored themselves and they’re trying to dishonor their country.

It’s true nonetheless that we’re moving into a new disposition of the human project. It’s going to be smaller and leaner, and not nearly as complex as the tottering Rube Goldberg apparatus we’re currently trapped in. We don’t know yet what the shape and texture of that America is going to be. As the sage Yogi Berra observed, our whole future is ahead of us. If you’re not among the insane, have faith. We’ll get there and everything is going to be all right.

I’ve been thinking a lot about one of the first lessons I was taught as a junior trader. We were warned that when something happens, say a piece of economic data comes out, and the market doesn’t respond as you expected, to cut positions and be very careful. It is a sign that “something” is wrong in how you are thinking.

On Friday, Treasuries rallied strongly on data that didn’t seem that great for rates. But the reality is (or so I believe) that Thursday’s sell-off was overdone, the “whisper” number was much worse than what came out, there are no longer term Treasury auctions, and the month-end index “extension” is usually good for bonds. So that doesn’t bother me much. What bothers me is that we had:

NVDA, a $2.2 trillion market cap company, drop 10% last Friday.

TSLA, a $500 billion market cap company, rise 10% on Wednesday.

META, a $1.1 trillion market cap company, drop 10% on Thursday.

GOOG, a $2.1 trillion market cap company, rise 10% on Friday.

Four "megacap" companies moved around 10% (or more) in a day!

I understand small cap companies do that. I understand that periodically something happens that is highly unusual – M&A, a scientific breakthrough, FDA approval, fraud, or something so unusual (but so profound) that a well-followed company gaps by that much. This was “just” earnings. Maybe I’m being overly dramatic? Maybe I haven’t adjusted my thought process to how large companies really are (probably part of the issue)? In any case it feels completely strange (even unnatural) for such large companies to move so much in a single session (let alone seeing it occur 4 times in 6 days)!

I am willing to believe that this is just my perception, and maybe it is more common than I perceive, but it is so different than how I’ve been thinking, that I have to respect it. As a “macro” strategist, I think about broad indices. Normally that is quite “macro,” but when some of the largest components of these indices (and associated ETFs) move so much more than I tend to think they can, then I need to question if it is still macro.

I can hear my first boss telling me that it is time to cut, sit back with less risk on the table, and think about what is going on. Maybe it is nothing. Maybe it is the new norm? Maybe 10% is the new 1%? Maybe moves close to 10% have always happened with market leaders and I just failed to notice that? I find it hard to believe, but knowing the T-Report audience, someone will likely send me a chart showing how common it is and that I need to “get over it.”

But I don’t think in terms of megacaps moving like that. To me, it reduces the macro, and is highly relevant as we have some other megacaps reporting this week. Should I assume 10% in either direction is a valid range? MSFT, for example, followed a more “normal” pattern. Some wild swings post-earnings in the after-market and pre-market. Stops getting triggered. Options at play. Digesting the first headlines, reading the details, listening to the call. All things that have conditioned me to see reasonably large moves in after-hours sometimes continuing into the next day of trading, typically ending with a meaningful change, but not a 10% change – especially for megacaps.

If this T-Report sounds like a broken record fixating on something that maybe isn’t important, I apologize, but it is bothering me a lot.

China

For the past 3 months, the CSI 300 (one measure of Chinese stocks) is up 8.5% versus 3.5% for the S&P 500 and 2% for the Nasdaq Composite.

One could look at this and say that:

The Chinese economy has turned the corner, helping stocks.

If China is doing better, it should help the global economy and sales into China, which should be good for all markets.

I remain firmly in the camp that:

Investors were too pessimistic on the Chinese market and positioning was too underweight or short. The unwind of structured notes sold to retail (that had leverage) was happening, but that has slowed.

It hasn’t taken much on the economic side to help the stock market (and there are some direct intervention techniques being used to help the stock market, without doing much for the economy). Less about the market.

Some of this is also linked to the performance of Chinese companies. Some are selling more products (Huawei phones in China, for example).

Since I think:

The reasons for the Chinese market rise have little to do with the economy (and I have recommended to clients to cut exposure here to FXI/KWEB).

The Threat of Made By China 2025 is real, so any rebound in China is not going to benefit global companies as much as it would have in prior years.

I have to caution against betting on global stocks because of what we are seeing in China.

Geopolitics

The pressure from global leaders calling on Israel to be cautious is mounting.

Iran, assuming they had hoped for a modicum of success with their 300+ missile and drone strike, is unlikely to do anything while they figure out why their attack was such a failure. See my base case in Should I Stay or Should I Go.

It would be a surprise if a geopolitical event caused problems for the markets this week, but then that is often the case. It is interesting that last weekend’s question of “Should I Stay or Should I Go” is as relevant as before, with some new factors added to the mix.

Bottom Line

Rates.

I am most comfortable with my view on rates.

We will get some “soft” data and Powell won’t be hawkish enough to convince the market that we are only going to get 1 cut (basically what is currently priced in). I do not see how we get to 0 and think that we could see the case for 2 to 3 (what the dots had, depending on whether you use median or average). Buy 2s at 5% (or 4.98% as the case may be).

While I expect fears of the deficit, supply, etc. to push us higher at some point, I like owning 10s above 4.6% and think that 4.45% is a reasonable near-term target. As mentioned earlier, there are a number of factors that could take us there as early as this week.

Equities

Since I’m bullish on Treasuries, should I in theory be bullish on equities? Maybe, but that correlation has been weak to nonexistent of late. We’ve addressed this in Changing Times Impacting Signals and Correlations and Rorschach Test. I’m hesitant to be bearish stocks, but bullish on Treasuries. More importantly, I’m reluctant to be too committed in any direction until I can make better sense of these large, single day moves for megacaps. When something is bothering me and I should have a better idea of what is going on (but I don’t), then it is prudent to be cautious.

So, I will remain bearish on equities and expect us to break the lows set on April 19th. It briefly looked like that was possible as recently as Thursday morning, but it seems less realistic now as the S&P gained 2.7% and the Nasdaq rallied 4.2%. I just cannot be too aggressive on this because I could easily see some additional 10% moves, which I’ve never really accounted for. Those moves could go in either direction.

The one thing that does make some sense about 10% moves is that if we really are on the cusp of a viable revolution in technology, the entire market seems cheap. But, if the cost/benefit ratio is not great right now (less than revolutionary improvements at rapidly rising prices), then we could move down rapidly. So maybe 10% moves, even in megacaps, is normal when we are at an inflection point in technology and potential valuations? That is plausible, though I’m not sure how to incorporate that into my framework, other than moving more and more into options to express long and short bets.

Credit.

Yawn. Not a lot of room to tighten. Can widen a bit more, but primarily as a function of stocks going down than any obvious change in fundamentals. With supply likely slowing, relative to cash earmarked for new issues, I’m biased to be mildly bullish credit spreads, even while moderately bearish equities.

May the stocks you own all go up 10% every day. I don’t completely understand it, but cannot ignore it, and might as well hope people benefit!

The Republican establishment doesn’t know it yet, but last weekend was a watershed moment for their party.

On April 20, House Republican leadership facilitated passage of a foreign-aid package that sends roughly $60 billion to Ukraine, $26 billion to Israel and Gaza, $8 billion to Taiwan, and exactly zero dollars to the southern border. The bill has since passed the Democrat-led Senate and was signed by President Joe Biden.

The vote will be remembered for the choice Republican leadership made to brazenly reject its own voters in favor of the “uniparty” in Washington, DC.

In a move that can only be described as “McConnell-esque,” House Republican leadership teamed up with Democrats to overrule the position of their own conference, their voters, and the will of the American people. Democrats on the House Rules Committee made an unprecedented move by crossing the party line and overruling Republican opposition in committee, signaling an end to the typically Democrat versus Republican battle and the beginning of the conservative versus “uniparty” war.

The disconnect between the Swamp and small-town America could not be more profound. How can a political party be so tone-deaf to the plight of the everyday American suffering under inflation, crime, and societal rot? How can a Republican-led House prioritize the borders of another country over our own border, even as American citizens are killed by illegal immigrants? How can so-called fiscally responsible Republicans sign off on what is now $174 billion in direct Ukraine aid with a national debt of $34 trillion, more than $250,000 for every American household? And how can House Speaker Mike Johnson, who had pledged repeatedly that no foreign-aid legislation would advance without first securing the border, so quickly be steamrolled by the Establishment?

In their desire to send billions of dollars to a conflict that our commander-in-chief has still, to this day, offered no plan for winning, the GOP’s leadership not only spurned their party’s own supporters but overlooked an opportunity to appeal to independent Americans frustrated by both political parties.

According to recent polling that The Heritage Foundation conducted with RMG Research, an overwhelming three out of four swing voters opposed sending any additional aid to Ukraine without also allocating funds for our own border. A majority (56 percent) of swing voters in key battleground states thought that the $113 billion the United States had already committed to Ukraine was too much.

The entire Heritage enterprise fought for over a year and half on this issue. Heritage Action engaged our millions of grassroots members to voice their concerns to their representatives. Scholars at The Heritage Foundation presented a national security alternative package that included limited military aid to Ukraine but made border security the central focus. In an unprecedented move, we even issued a “key vote” on our legislative scorecard against Speaker Johnson’s convoluted rule, which was a gimmick that lowered the threshold to a simple majority (not a supermajority under suspension) and provided political cover for members to vote against individual pieces without jeopardizing the package.

Powerful interests were aligned against us, however, and we lost on the day. Though we lost this battle, all signs indicate that we are winning the war for the soul of the GOP. A majority (112) of Republicans voted against Ukraine aid on April 20. Younger and newer members are particularly fed up with leadership’s conciliatory approach and manipulative tactics that have led us to this point. The average age of the Senate Republicans who voted “nay” is 59, while the average age of those who voted “yea” is 66. The average “nay” vote has been in office since just 2016, while the average “yea” vote has been in Washington since 2010. The same dynamic was true with the recent $1.2 trillion omnibus spending bill.

This generational shift can be ignored by the “uniparty,” but it’s not going away. Newer, younger representatives want a choice, not an echo, and increasingly they’re adopting a populist form of conservatism that champions “government of the people, by the people, and for the people” above all else. In other words, they want a GOP that puts America first, something a government in any healthy republic would do. They want a GOP that acknowledges the reality that America is a nation in decline but is not yet too late to save.

As Ronald Reagan said in his 1980 address accepting the presidential nomination at the Republican National Convention, “For those who have abandoned hope, we'll restore hope and we’ll welcome them into a great national crusade to make America great again!”

And that brings us to the importance of this year’s election.

In 2016, despite staunch opposition from the GOP leadership, Donald Trump rejected the Washington consensus and initiated a generational realignment in American politics. If the conservative movement leans into the politics and policies President Trump made successful, the American people will again have the opportunity this fall to accelerate a new consensus in Washington, DC. This is why I remain optimistic about the future of our great nation.

The GOP establishment’s actions this past week portend the end of the GOP establishment, not its survival. Conservatives will win the soul of the GOP and with it the hearts of the American people.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

NY Judge Claims '2nd Amendment Doesn't Exist In Her Courtroom' In Case Against Gunsmith

Dexter Taylor, a software engineer and resident of Brooklyn, NY, took on gunsmithing as a hobby during the Covid-19 lockdowns. He was already familiar with machining and found himself fascinated by the project, so he set out to learn the skills needed. Taylor researched ATF rules regarding the building of firearms and wanted to follow them carefully. Sadly, however, the state of New York has its own laws which leftist governments believe supersede federal law and the Constitution.

Because Taylor was apparently not officially licensed as a gunsmith in NY, authorities decided to raid his home and arrest him for possession of gun parts (including 80% lowers) which are legal federally but require a smithing certificate in the state (a legal gray area which is being contested). Taylor was easy to find because he purchased all the parts with his own credit cards thinking he was protected under ATF rules.

ATF rules state that the building of guns for personal use including 80% lowers and related parts is legal as long as the person does not build those weapons to sell.

Taylor's lawyer, Vinoo Varghese, noted that the case is a difficult one in New York, hinting at the leftist bias within NY courtrooms when it comes to the 2nd Amendment. In fact, Varghese suggested that when Judge Abena Darkeh took over the case she was oddly hostile towards the defense. He mentions that she interrupted his opening statements multiple times, claiming that he could not use 2nd Amendment arguments in her courtroom:

"She told us, ‘Do not bring the Second Amendment into this courtroom. It doesn’t exist here. So you can’t argue Second Amendment. This is New York.'"

Of course, the 2nd Amendment and the Bill of Rights surpasses the authority of the State of New York and the courtroom of Judge Abena Darkeh. New York progressives might like to think their state is a separate country from the US with its own rules, but it's not. It's clear that this is a situation in which an activist judge is seeking to make an example out of a law abiding citizen with no previous criminal record. The goal is to send a message that blue states are going to fabricate their own rules when it comes to gun rights regardless of constitutional precedent.

Varghese hints in a recent interview that the Judge is married to the "biggest fundraiser" for the Brooklyn DA, which may present a conflict of interest. Also, Joe Biden has made the issue of "Ghost Guns" a primary target for his administration the past few years. To date, the use of ghost guns in criminal acts in the US is statistically negligible. It's simply not a problem that needs the attention of the White House.

NEW: Brooklyn man convicted over his gunsmithing hobby after the judge says that the 2nd Amendment 'doesn't exist in this courtroom'

‘Do not bring the Second Amendment into this courtroom. It doesn’t exist here. So you can’t argue Second Amendment. This is New York.' - Judge… pic.twitter.com/cgfPO4ANnm

The defense also asserted that the Judge pressured the jury to come back with a guilty verdict, which they did, convicting Taylor of a list of offenses including:

Second-degree criminal possession of a loaded weapon, four counts of third-degree criminal possession of a weapon, five counts of criminal possession of a firearm, second-degree criminal possession of five or more firearms, unlawful possession of pistol ammunition, violation of certificate of registration, prohibition on unfinished frames or receivers. Two lesser charges, including third-degree criminal possession of three or more firearms and third-degree possession of a weapon, were not voted on.

Keep in mind that in the vast majority of states in the US all of these charges sound ridiculous. Possession of a loaded weapon? Unlawful possession of pistol ammunition? What?

Taylor now faces 10-18 years in prison and he awaits sentencing in Rikers Island, one of the worst prisons in the country. The case is expected to be appealed to the Supreme Court, where a number of gun cases involving 80% lowers are awaiting decision. New York's habit of punishing good people while letting criminals go free is becoming an epidemic, and it's likely a primary reason why the state is now suffering a net loss of hundreds of thousands of residents every year.

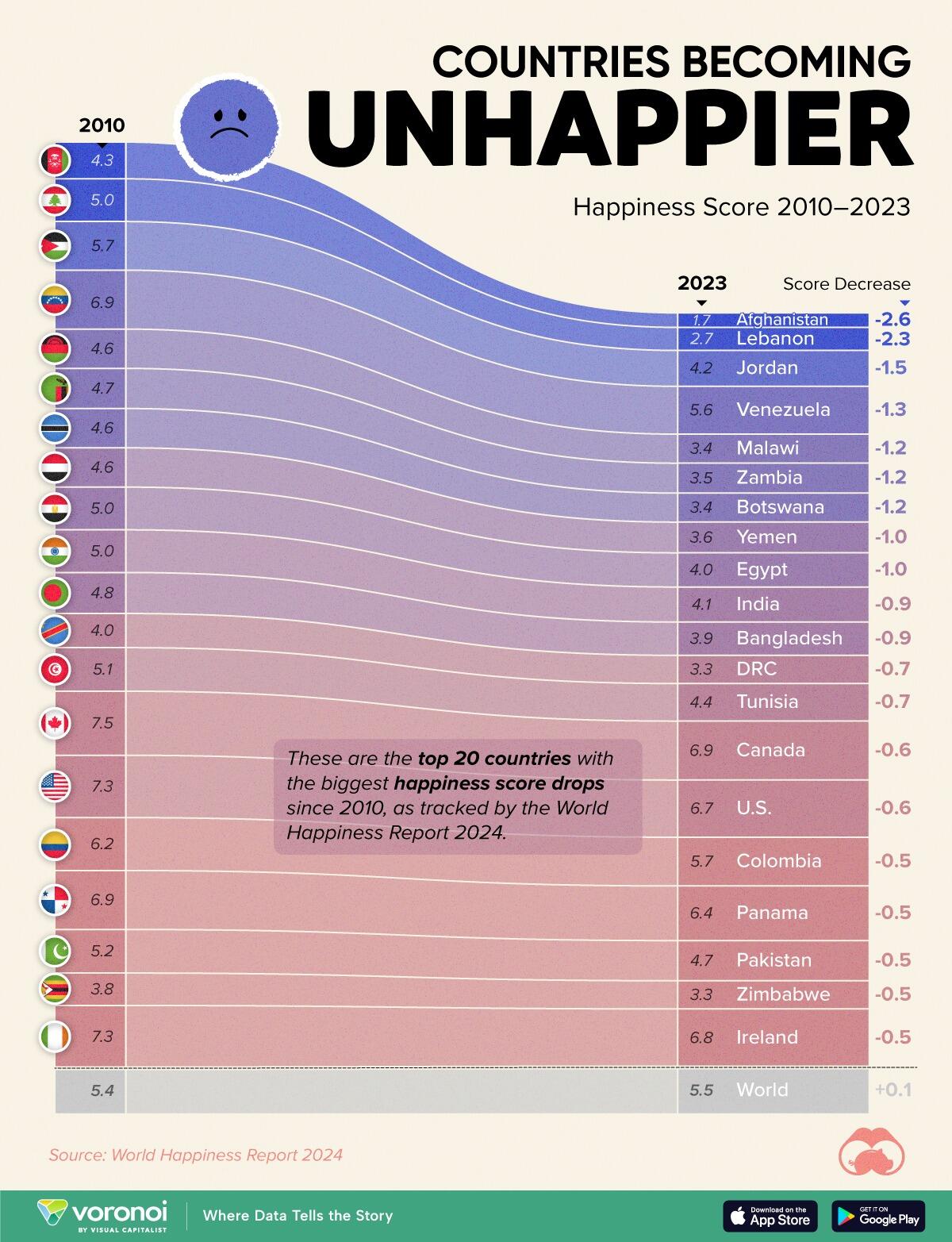

These Are The Countries That Have Become 'Sadder' Since 2010

Can happiness be quantified?

Some approaches that try to answer this question make a distinction between two differing components of happiness: a daily experience part, and a more general life evaluation (which includes how people think about their life as a whole).

The World Happiness Report - first launched in 2012 - has been making a serious go at quantifying happiness, by examining Gallup poll data that asks respondents in nearly every country to evaluate their life on a 0–10 scale. From this they extrapolate a single “happiness score” out of 10 to compare how happy (or unhappy) countries are.

Afghanistan is the unhappiest country in the world right now, and is also 60% unhappier than over a decade ago, indicating how much life has worsened since 2010.

In 2021, the Taliban officially returned to power in Afghanistan, after nearly two decades of American occupation in the country. The Islamic fundamentalist group has made life harder, especially for women, who are restricted from pursuing higher education, travel, and work.

On a broader scale, the Afghan economy has suffered post-Taliban takeover, with various consequent effects: mass unemployment, a drop in income, malnutrition, and a crumbling healthcare system.

Nine countries in total saw their happiness score drop by a full point or more, on the 0–10 scale.

Noticeably, many of them have seen years of social and economic upheaval. Lebanon, for example, has been grappling with decades of corruption, and a severe liquidity crisis since 2019 that has resulted in a banking system collapse, sending poverty levels skyrocketing.

In Jordan, unprecedented population growth—from refugees leaving Iraq and Syria—has aggravated unemployment rates. A somewhat abrupt change in the line of succession has also raised concerns about political stability in the country.

A confluence of factors continues to impact San Francisco’s office market, with vacancy and availability rates reaching record highs in the first quarter of 2024, according to commercial real estate analysts at global companies Avison Young and CBRE.

Availability - the combination of vacancy and sublease opportunities in the market - reached 36.7 percent of all office square footage from January to April, according to recently released market analyses from the leading commercial real estate firms.

“We’re at mostly record levels, and I say that kind of cautiously optimistic,” Dina Gouveia, west region market intelligence manager for Avison Young, told The Epoch Times April 25.

According to Ms. Gouveia vacancies only saw a “slight uptick” during the first quarter which might mean such is slowing.

“[I]f we can continue that slower velocity of additional vacancies ... then it would be a very good indicator of us being near a bottom,” she said.

Much of the issue, experts say, is the city’s reliance on the tech industry, with more than 44 percent of its office space housing technology companies.

Additionally, tech firms lead the list of upcoming lease expirations—accounting for 45.8 percent, according to Avison Young.

San Francisco’s office market was deeply affected as the number of work-from-home employees skyrocketed during the pandemic, though recent trends show a slight return to the office.

Remote job postings fell more than 5 percent to 22.2 percent in the first quarter compared to the end of last year, according to the Avison Young report.

Job postings increased 22.7 percent in the first quarter following seven consecutive quarters of decline. The listings were led by legal services, engineering, consulting, research, accounting, and recruiting companies. Media and tech industries, however, both experienced declines, according to the report.

Unemployment, however, ticked up to 4.4 percent in the first quarter, a sharp increase from its low of 2.3 percent in June 2022.

According to the report, slightly less than 1 million total square footage was leased in the first quarter—a 63.3 percent drop from the five-year pre-pandemic average.

Analysts noted signs they deemed optimistic, including Netherlands-based payment company Adyen’s sublease of space at 505 Brannan Street—in the city’s South of Market district—and multinational accounting company KPMG’s lease renewal at 55 2nd Street, in the city’s financial district. Combined, those leases total 300,000 square feet, experts said.

Sublease opportunities offer lower rents than signing new leases that require build outs and significant capital to develop properties, which is spurring the sector of the market, while also allowing businesses with existing leases to rent out some of their vacant space.

“The amount of sublease activity that we’ve seen has increased a lot because tenants are looking for plug-and-play opportunities,” Ms. Gouveia said. “A lot more activity is happening because tenants ... want to take advantage of pre-built spaces and lower rents.”

High interest rates are making it harder for companies with limited cash to refinance loans. At the same time, rates are also slowing down new purchases, according to analysts.

With an uncertain market—in part due to conflicting signals from the Federal Reserve about the future of interest rates—prospective tenants are seeking flexibility when looking to renew leases or relocate.

“Interest rates are a huge catalyst,” Ms. Gouveia said. “We’re hearing a little bit of two different stories that interest rates are going down and then they’re not. If the interest rates do come down ... that will stimulate the commercial market quite a bit.”

In response, the highest quality properties have seen lease term lengths decrease from quarter-to-quarter to make them less risky.

Such wariness from tenants is forcing some landlords to lower rents and offer concession packages to attract business, though a disparity still remains between what tenants want to pay and what landlords can offer given their current debt load.

Many landlords are working with their lenders to restructure debt before loans come due, and analysts expect rent prices to become more favorable for tenants once such is realized.

“Rents will definitely come down,” Ms. Gouveia said. “And once that debt workout happens, there’s going to be a larger reset.”

Distressed properties at risk of default are creating buying opportunities of which private buyers are increasingly taking advantage. Industrial investors and real estate investment trusts, however, are on the sidelines, with 100 percent of all investment activity coming from private buyers in the first quarter, according to the report.

On the other hand, the percentage of private sellers also increased to begin the year compared to prior years, with analysts pointing to uncertainty that their debt can be restructured due to high interest rates and limited financing opportunities.

Refinancing has proven challenging because lenders are reluctant to write loans for office buildings because defaults are looming and valuations are plummeting, with true market values unclear, according to analysts.

A pending election is also slowing activity, as many firms want more certainty before making large capital decisions.

“Because we’re coming up on an election year, a lot of companies go dormant on their expansion plans, and servicers are also in that wait-and-see mode,” Ms. Gouveia said.

Another global commercial real estate leader, CBRE, found that San Francisco’s office market is facing unique challenges given crime and homelessness impacting the city.

According to Colin Yasukochi, executive director of CBRE’s Tech Insights Center, more office tenants are signing new leases, showing a willingness to recommit to the city, but are still somewhat tentative when doing so.

“This dynamic is still somewhat tenuous as employers and their employees still have concerns about public safety and the cost of doing business,” he told The Epoch Times by email.

Noting that some workers are returning to the office for more days a week he suggested such is not enough for a recovery, which, he said, will require a desire to compete in a robust economic environment.

“Additional mandates are unlikely to increase office attendance materially at this point, but rather a booming economy will compel more people to want to be in the office and be better connected to the next growth cycle,” Mr. Yasukochi said.

While artificial intelligence could play a significant role in buoying the tech sector that the city relies on, a fast recovery, he said, is not anticipated.

“The San Francisco office market is beginning to transition out of its four-year downturn,” Mr. Yasukochi said. “While it will take many years to rebalance supply and demand, we are starting to see positive signs.”

Seasoned veterinarians and livestock producers alike have been scratching their heads trying to understand the media’s response to the avian flu.

Headlines across every major news outlet warn of humans becoming infected with the “deadly” bird flu after one reported case of pink-eye in a human.

The entire narrative is predicated upon a long-disputed claim that Covid-19 was the result of a zoonotic jump—the famed Wuhan bat wet-market theory.

While the source of Covid is hotly contested within the scientific community, the policy vehicle at the center of this dialectic began years prior to Sars-CoV-2 and is quite resolute in force and effect.

In 2016, the Gates Foundation donated to the World Health Organization to create the OneHealth Initiative. Since 2020, the CDC has adopted and implemented the OneHealth Initiative to build a “collaborative, multisectoral, and transdisciplinary approach—working at the local, regional, national, and global levels—with the goal of achieving optimal health outcomes recognizing the interconnection between people, animals, plants, and their shared environment.”

In the aftermath of Covid-19, the OneHealth Initiative began taking shape, due largely in part to millions of tax dollars appropriated through ARP (American Rescue Plan) funding.

Through its APHIS (Animal and Plant Health Investigation System) the USDA (United States Department of Agriculture) was given $300 million in 2021 to begin implementing “a risk-based, comprehensive, integrated disease monitoring and surveillance system domestically…to build additional capacity for zoonotic disease surveillance and prevention,” globally.

“The One Health concept recognizes that the health of people, animals, and the environment are all linked,” said USDA Under Secretary for Marketing and Regulatory Programs Jenny Lester Moffitt.

According to the USDA’s press release, the Biden-Harris administration’s OneHealth approach will also help to ensure “new markets and streams of income for farmers and producers using climate smart food and forestry practices,” by “making historic investments in infrastructure and clean energy capabilities in rural America.”

In other words, the federal government is using regulatory enforcement to intervene in the marketplace, in addition to subsidizing corporations with tax dollars to direct a planned economic outcome—ending meat consumption.

Climate-Smart Commodities – Planning the Economy through Subsidized Intervention

Under the recently announced Climate-Smart Commodities program, the USDA has appropriated $3.1 billion in tax subsidies to one hundred and forty-one new private Climate-Smart projects, ranging from carbon sequestration to Climate-Smart meat and forestry practices.

Private investors such as Amazon founder Jeff Bezos – who just committed $1 billion to the development of lab cultured meat-like molds, and meat grown in petri dishes, to

Ballpark, formerly known for its hot dogs but is now harvesting python meat, is rushing to cash in on this new industry, and the OneHealth/USDA certification program.

Culling The Herd – Regulatory Intervention in the Marketplace

Meanwhile, the last vestiges of America’s food freedom and decentralized food sources are quietly being targeted by the full force of the federal government.

The once voluntary APHIS System is poised to become the mandatory APHIS-15, which among many other changes, “the system will be renamed Animal Health, Disease, and Pest Surveillance and Management System, USDA/APHIS-15. This system is used by APHIS to collect, manage, and evaluate animal health data for disease and pest control and surveillance programs.”

Among those “many changes” that APHIS-15 is undergoing, one should be of particular interest to the public—the removal of all references to the voluntary* Bovine Johne’s Disease Control Program.

“Updating the authority for maintenance of the system to remove reference to the Bovine Johne’s Disease Control Program.”

According to the USDA/APHIS-15, expanded authority places disease tracing in their jurisdiction and the radio frequency ear tags are necessary for the “rapid and accurate recordkeeping for this volume of animals and movement,” which they say “is not achievable without electronic systems.”

The notice clearly spells out that RFID tags “may be read without restraint as the animal goes past an electronic reader.”

“Once the reader scans the tag, the electronically collected tag number can be rapidly and accurately transmitted from the reader to a connected electronic database.”

However, industry leaders and lawmakers alike have said the database will be used to track vaccination history and movement, and that this data may be used to impact the market rate of cattle and bison at the time of processing.

Centralized Control of Processing/Production via Public-Private Partnership Agreements

In addition to the vast new authority of the USDA funded through the OneHealth Initiative, and the ARP, the EPA has also created its own unique set of regulatory burdens upon the entire meat industry.

On March 25, 2024, the EPA finalized a new set of Clean Water Act rule changes to limit nitrogen and phosphorus “pollutants” in downstream water treatment facilities from processing facilities. While the EPA’s interpretation of authority and jurisdiction over wastewater is concerning long-term, the broader context of consolidated processing under four multinational meat-packing companies is of much greater concern for the immediate future.

With few exceptions, in the United States it is illegal to sell meat without a USDA certification. Currently, the only way to access USDA certification is through a USDA-certified processing facility.

According to the EPA, the new rules will impact up to 845 processing facilities nationwide, unless facilities drastically limit the amount of meat they process each year.

With processing capabilities being the number one barrier to market for livestock producers, and billions of dollars in grants being awarded to Climate-Smart food substitutes, the amount of government intervention into the marketplace becomes very clear.

The Rise of Authoritarianism and Economic Fascism – Control the Supply

The United States, once a consumer-demand free market society, is currently witnessing the use of government force, and intervention tactics to steer and manipulate the marketplace. Similar to 1930’s Italy, this is being achieved by the state within the state, through the use of selectionism, protectionism, and economic planning between public-private partnership agreements.

The long-term and unavoidable problem with economic fascism is that it leads to authoritarian and centralized control, from which escape is impossible.

As each industry becomes centralized and consolidated under the few, consumer choice simultaneously disappears. As choice disappears, so does the ability of the individual to meet their specific and unique needs.

Eventually, the individual no longer serves a role outside of its usefulness to the state—the final exhale before the last python squeeze.

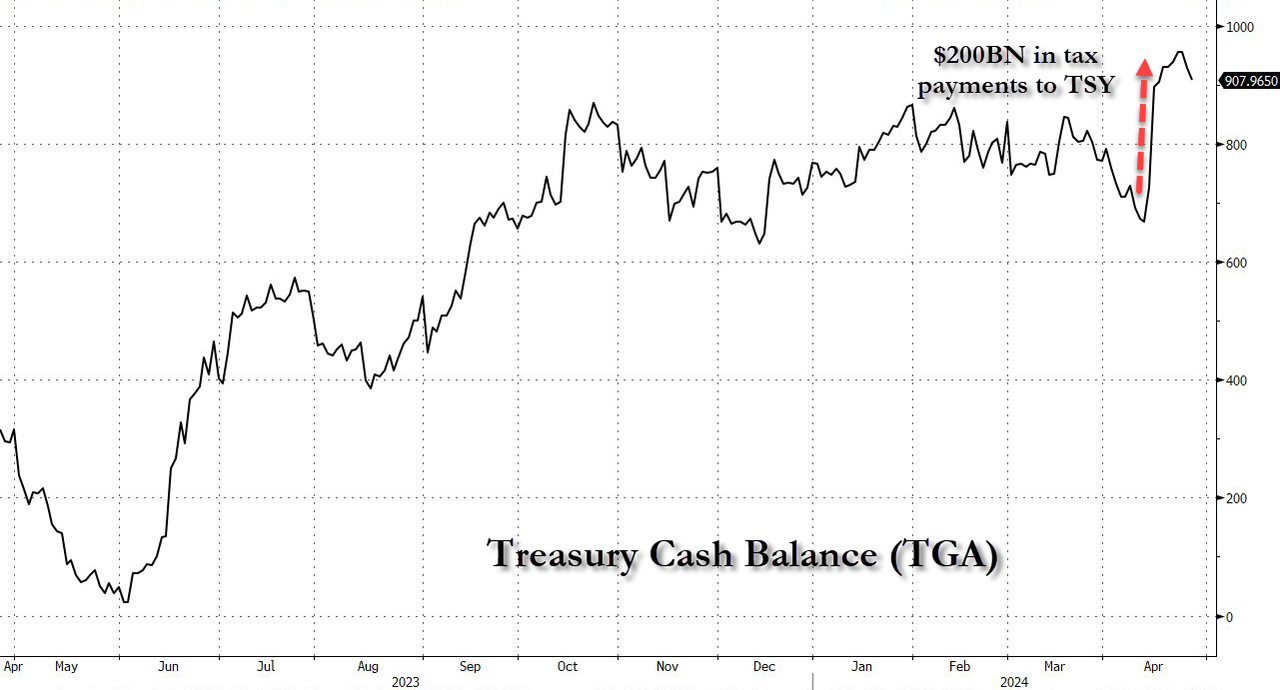

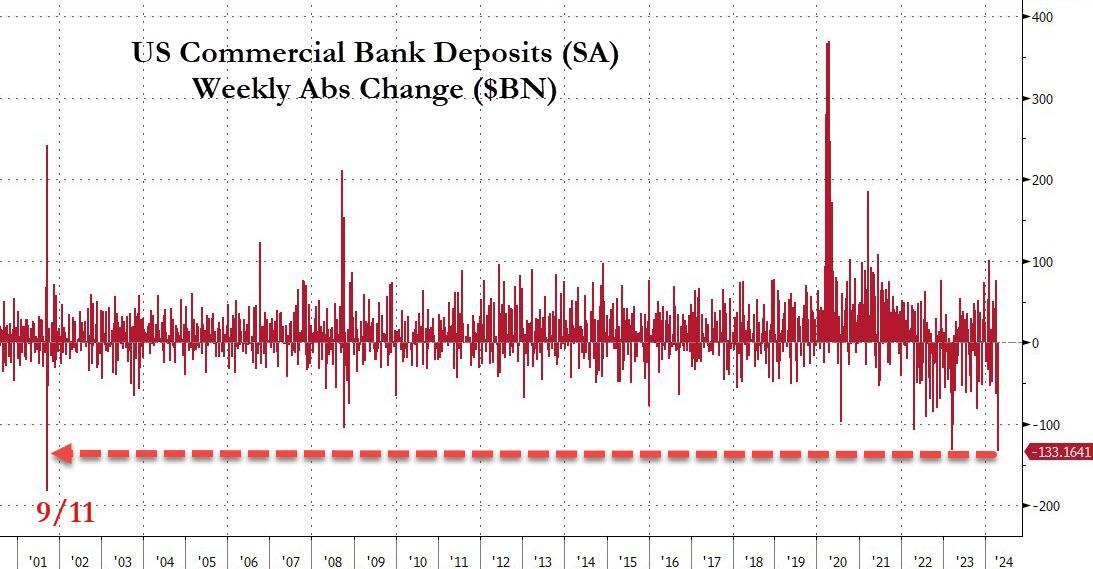

US Bank Deposits Suffer Biggest Weekly Decline Since 9/11 As Tax Man Cometh

It's that time of year again and US bank deposits sure showed it...

While money-market funds' total assets fell over $100BN,on a non-seasonally-adjusted (NSA) basis, total bank deposits crashed by a stunning $258BN as Tax-Day cometh. That is considerably more than the $152BN decline last year but less than the $336BN plunge in 2022...

Source: Bloomberg

This makes some sense though as the Treasury Cash Balance rose by around the same amount as taxpayers did their duty and paid their 'fair share'...

Source: Bloomberg

However, on a seasonally-adjusted (SA) basis (i.e. adjusted by the PhDs for the fact that we get large deposit outflows at this time of year to pay taxes), total deposits dropped $133BN - the biggest weekly plunge (SA) since 9/11!

Source: Bloomberg

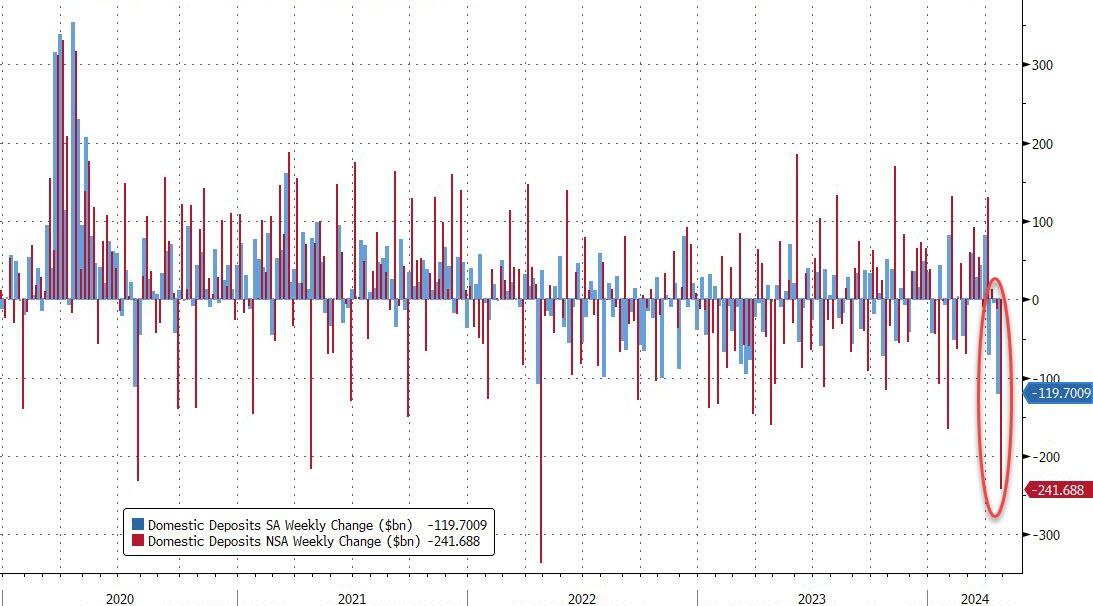

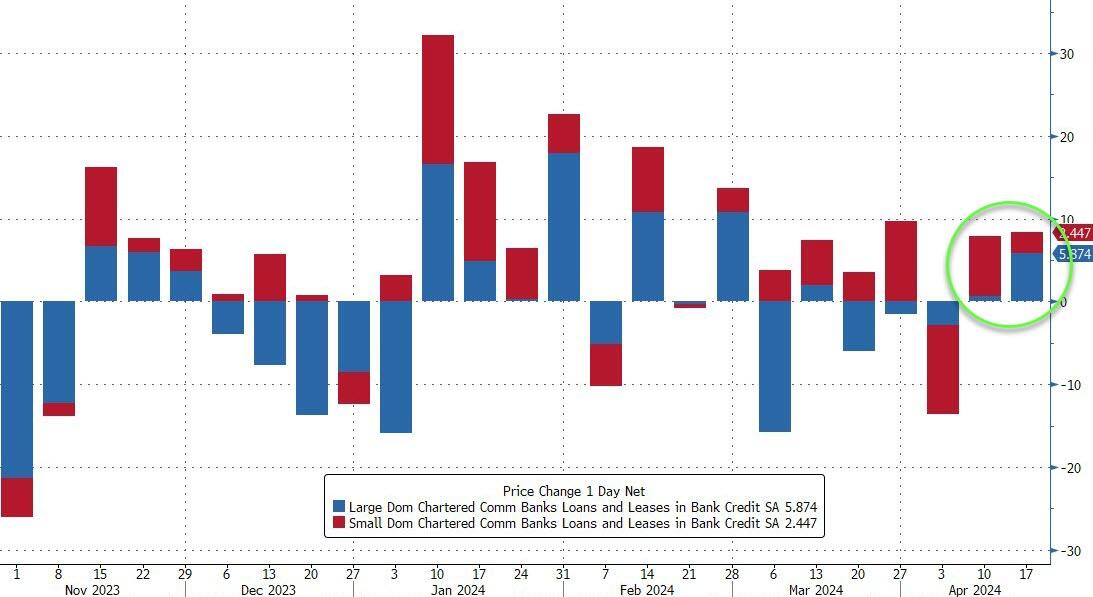

Excluding foreign deposits, domestic bank deposits plunged on both an SA (-$119BN: Large banks -$99BN, Small banks -$21BN) and NSA (-$241BN: Large banks -$188BN, Small banks -$53BN) basis...

Source: Bloomberg

For context, that is the largest weekly drop in SA deposits since 9/11 and the largest NSA deposit drop since April 2022 (Tax Day).

Interestingly, despite the deposit dump, loan volumes increased last week with large banks adding $5.8BN and small banks adding $2.5BN...

Source: Bloomberg

All of which pushed the un-bailed-out 'Small banks' back into 'crisis mode' (red line below constraint absent the $126BN still in the BTFP pot at The Fed which is slowly being unwound)...

Source: Bloomberg

And so, with rate-cuts off the table - and tapering QT very much back on - we wonder just how much jockeying between Janet (Yellen) and Jerome (Powell) is going on ahead of next week's QRA and FOMC news...

As the U.S. Justice Department decides whether to pursue a criminal case against Boeing, the Federal Aviation Administration (FAA) is investigating dozens of airplane incidents since January, including one in which a Swiss Air jet almost collided with four other planes on the runway at JFK International Airport in New York City.

The FAA has more than 100 aviation accidents and incidents since the beginning of 2024. These include airplane and helicopter crashes, equipment and mechanical malfunctions, and communication breakdowns with air traffic controllers that almost caused runway collisions at several major U.S. airports.

These incidents come as public scrutiny of Boeing increases after multiple issues have been reported with their jets. After an Alaskan Airways flight experienced a mid-air blowout of a door plug on Jan. 5, the Justice Department is considering revoking a 2021 deferred prosecution agreement with the company and pursuing a criminal case.

There is also growing criticism of Air Traffic Control (ATC) and the FAA’s hiring practices after multiple near-collisions were reported, including at JFK Airport and Reagan National Airport in Arlington, Virginia.

The JFK incident occurred on April 17. Pilots on a Swiss Air flight headed to Zurich, Switzerland, were forced to hit the brakes after the plane was cleared for takeoff because air traffic controllers simultaneously opened the runway for four other planes.

The next day, a similar incident played out at Reagan Washington National Airport, which services the Washington area. ATC cleared a JetBlue flight for takeoff as a Southwest Airlines flight was told to taxi across the same runway in front of it, according to ATC audio.

A runway controller cleared the JetBlue flight, while a taxiing controller cleared the Southwest Airlines flight. The two planes came within 400 feet of a collision before each controller ordered the planes to stop.

“JetBlue 1554 stop! 1554 stop!” said the tower controller, as the ground controller said “2937 stop!” to the Southwest Airlines plane.

Two airplanes—JetBlue and Southwest—nearly collided at DC’s Reagan National Airport on Thursday, avoiding each other by only 400 feet.

Air traffic control recordings show the moment controllers yelled at the JetBlue flight to “stop!” its takeoff.pic.twitter.com/Td1VTimVD0

Since sudden runway stops can overheat airplane brakes, the JetBlue flight was inspected before it safely departed the airport.

The agency said it is investigating both incidents.

Juan Browne, a Boeing 777 first officer pilot for a major U.S. airline company, told The Epoch Times that while the number of airplane accidents has remained steady, ATC incidents are “on the rise.”

He said the “primary driver” of this phenomenon is the “huge turnover” in the industry, as controllers retired during the COVID-19 pandemic. Many retired early, creating a “big shortage of people, pilots, and air traffic controllers,” and some, including pilots and others, retired due to vaccine mandates.

However, other factors leading to ATC communication breakdowns include diversity-focused hiring practices, a bottleneck in controller training, distractions, and pilot error.

Diversity Hiring Practices

Many, including aviation expert Kyle Bailey, have called out the FAA for prioritizing “diversity” in its hiring practices, alleging that hiring pilots or controllers based on their skin instead of their merit, can lead to safety issues.

“Diversity really has nothing to do with safe travel,” Mr. Bailey told Fox News Digital in January.

The aviation agency’s “Diversity and Inclusion webpage, last updated on March 23, 2022, says, ”Diversity is integral to achieving the FAA’s mission of ensuring safe and efficient travel across our nation and beyond.”

In its "Aviation Safety Workforce Plan, the agency explains this policy further.

“[Diversity] practices facilitate the organization in attracting and hiring talented applicants from diverse backgrounds and to meet future needs. A commitment to diversity and inclusion supports [aviation safety’s] strategic initiative to create a workforce with the leadership, technical, and functional skills necessary to ensure the U.S. has the world’s safest and most productive aviation sector.”

Later, the agency discusses how this can impact operations.

“The projected growth in demand and diversity from conventional customers, as well as new entrants in non-traditional areas will challenge the FAA’s ability to provide responsive and consistent service to our stakeholders, the report reads.

“It seems that the FAA has placed ‘diversity bean counting over safety and expertise, and we worry that such misordered priorities could be catastrophic for American travelers, Mr. Kobach wrote in the letter.

“Millions of Americans place their lives and the lives of their loved ones in the hands of your agency ... Unfortunately, the Biden FAA, under your administration, appears to prioritize virtue-signaling ‘diversity efforts over aviation expertise. And this calls into question the agency’s commitment to safety, he added.

The letter accused the Obama administration of seeking out applicants with “severe intellectual” and “psychiatric” disabilities, noting that the FAA’s “Diversity and Inclusion” webpage currently has the same language on it.

Mr. Browne, who has been a commercial pilot for 25 years, told The Epoch Times that there is a big drive towards on-the-job diversity in all U.S. industries, and aviation is no different.

“I can’t speak specifically to what those requirements are at the FAA ATC program, but we definitely need to ask ourselves: Are we hiring and training the correct people for the jobs?” he asked.

“How are we getting the most qualified applicants out there to fill these jobs?”

Retirements and Training ‘Bottleneck’

Another factor leading to issues with ATC is the sheer volume of retirements in the aviation industry during the pandemic, Mr. Browne said.

He explained that some pilots and air traffic controllers were close to retirement age when the pandemic started, with many deciding to retire early. This created a shortage of applicants and now a shortage of active workers, as both the FAA and ATC struggled to keep up when a waning pandemic caused airline travel demand to increase.

“So we got a lot of new folks out there on the job right now, a lot of on-the-job training going on right now. And a lot of mistakes being made up there as well,” he said.

Some also retired early because they declined to take the mRNA COVID-19 vaccine when it was briefly mandated by the FAA, Mr. Browne added.

With these early retirements came limited training opportunities and a “shortage of qualified controllers.”

“There was a big bottleneck in training throughout the aviation industry, whether it was for pilots or for air traffic controllers who have trained up in Oklahoma City, the home of the FAA,” Mr. Browne said.

“And so, now, the FAA is trying to do more with less.”

He explained that the agency is working its current and new controllers “much harder and longer hours than they have in the past” to “backfill” the demand after airlines quickly and unexpectedly recovered from the pandemic. This “exacerbated the shortage of both pilots and air traffic controllers,” Mr. Browne said.

In a statement to The Epoch Times, the FAA disputed the claim that there were “excessive controller retirements during the pandemic.”

Distractions, Infrastructure, Budget Issues

As a Boeing 777 pilot, Mr. Browne mostly flies overseas. When he flies into cities like London or Sydney, he says the radio channels through ATC are “a lot less chaotic” and more “organized” compared to the United States.

“Here in the States, we’re pushing so much material, so many aircraft through such a tight system and dealing with weather constantly,” he explained.

“And yet, there seems to be a lot of miscommunications between different members of the staff, for example, ground controllers versus tower controllers.”

It was a miscommunication between ground and tower controllers that resulted in the near-collision at Reagan Washington National Airport on April 18.

Mr. Browne said he often hears a lot of background noise coming over the radio from within the control towers. Pilots are instructed to maintain a “sterile cockpit” whenever they’re below 10,000 feet, he explained. That means pilots must refrain from any conversation outside plane operations until they reach that altitude to “avoid distractions.”

“Is that not the case with the ATC?” Mr. Browne asked.

He explained that working in ATC can be a boring job, so it’s “human nature to get distracted, to do something else to break the monotony,” even if it’s critical to avoid this to prevent putting passengers’ lives at risk.

However, it’s not just distractions leading to issues with coordinating plane routes on runways. The infrastructure throughout the aviation industry struggles to keep pace with the growing demand for air travel.

Mr. Browne explained that ATC, airports, runways, plane parking access, and the number of gates were all designed for “a lot less traffic.”

“But in general, where we are, the demand is outstripping the capacity of the system. And that leads to, in the case of the FAA controllers, a lot of overtime and a lot of tired controllers on the job,” he added.

There are also budget concerns for ATC. Mr. Browne wonders if Congress is allocating enough funds to keep pace with air travel demands but said that question is up to congressional leaders to consider.

Lastly, pilots are sometimes at fault as well for aviation incidents, he explained.

Mr. Browne said there are multiple factors worth considering in addressing these problems. Not only could Congress increase the FAA’s budget, but ATC can be more transparent when there are incidents like the ones on April 17 and 18.

When pilots make significant mistakes, a full investigation commences immediately. But for air traffic controllers, it’s not always the same approach, Mr. Browne said.

However, the most significant factor is getting the best applicants for pilot and air traffic controller positions.

“Make sure we’re hiring the right people for the job, regardless of who they are or what they are. Make sure you’re hiring the most qualified people for these very demanding jobs,” Mr. Browne added.

“If we continue to perform at this level, [these incidents] will eventually lead to a disaster.”

The FAA told The Epoch Times that it is working to address some of these issues, but did not specifically comment on the “diversity hiring” allegations.

“Hiring highly qualified air traffic controllers is a top priority at the FAA. Every FAA-certified air traffic controller has gone through months of screening and training at the FAA Academy, and that is before another 18-24 months of training to learn specific regions and airspace.

“There is a well-known national shortage of air traffic controllers and the FAA has ramped up outreach to ensure no talent is left on the table. We are accelerating the pace of recruiting, training, and hiring to meet demand while maintaining the highest qualification standards,” the agency said in a statement.