Tesla Soars: Misses Across The Board, But Is "Accelerating" Rollout Of "More Affordable Models"

As previewed earlier, today's TSLA print is likely to be ugly: the company is the only Mag7 member expected to reported negative earnings growth...

... as a result of anemic Q1 sales, where the (growing) delta between production and deliveries was 46,000+ cars. Since then, CEO Elon Musk has doubled down on his robotaxi vision and vowed to unveil said robotaxi on August 8th. He also laid off more than 10% of the workforce and lost two key executives, while over the weekend, Tesla slashed prices across its lineup yet again and also reduced the cost of Full Self-Driving, or FSD -- which despite the name requires attentive drivers to keep their hands on the wheel.

For those who missed it, this is what Wall Street is looking for, starting with the first quarter:

- Q1 Revenue estimate $22.3 billion

- Q1 Adjusted EPS estimate 52c

- Automotive gross margin estimate 17.6%

- Free cash flow estimate $651.7 million

- Gross margin estimate 16.5%

- Capital expenditure estimate $2.4 billion

- Cash and cash equivalents estimate $23.24 billion

Turning to the next quarter:

- Q2 Automotive gross margin estimate 17.9%

And the full year

- Deliveries estimate 1.94 million

- Automotive gross margin estimate 17.9%

- Capital expenditure estimate $9.91 billion

Goldman cautions that while there is clearly skepticism on both TSLA and the EV market as a whole, with deliveries already announced for 1Q (stock was down 5% on this and another -14% additionally since), much of this has been priced in with short interest is at 3-year highs. Goldman thinks the key focus for investors will be

- Can they grow volumes in 2024? Goldman thinks investors were at +10-15% y/y to start the year and are now in the 1-2% range, and

- What are gross margins and how low do they need to go? Consensus looks to be 15.8% (ex-credits) and bogey seems to be below 15% for the quarter.

The one thing that everyone -- from the Wall Street giant to the retail investor -- wants from this earnings print and call, is simple: Clarity. Each group historically assigns different importance to different things and never before has the dichotomy of a robotaxi thesis vs. the pursuit of an affordable EV been so important. So Elon better give the people (investors) what they want, unless he wants to see what is already a record-matching stretch of stock price declines extend further.

Musk has also given us plenty of hints on his focus (spoiler: it’s Robotaxi). And sure enough, the call with Musk will be more important than the print itself. As Bloomberg notes, do we get an expansive, optimistic Musk who sells investors on the robotaxi? Or is he testy and curt with Wall Street analysts?

While Tesla shares closed up 1.8% ahead of the results, snapping a seven day losing streak, and joining the other mega-cap names that also rose, Tesla earnings haven’t been a happy event for investors for a long time now: shares of the company have dropped at least 9% the day after its results in each of the past four quarters. Tuesday’s announcement can also lead to a volatile reaction, with options trading implying that investors are pricing in an 8.3% move in either direction.

Meanwhile, technical strategists, who analyze moves in share prices to predict their future path, are also warning that the stock currently has little support and there’s risk that any disappointment in Tuesday’s report or Musk’s conference call could snowball into a much larger decline.

* * *

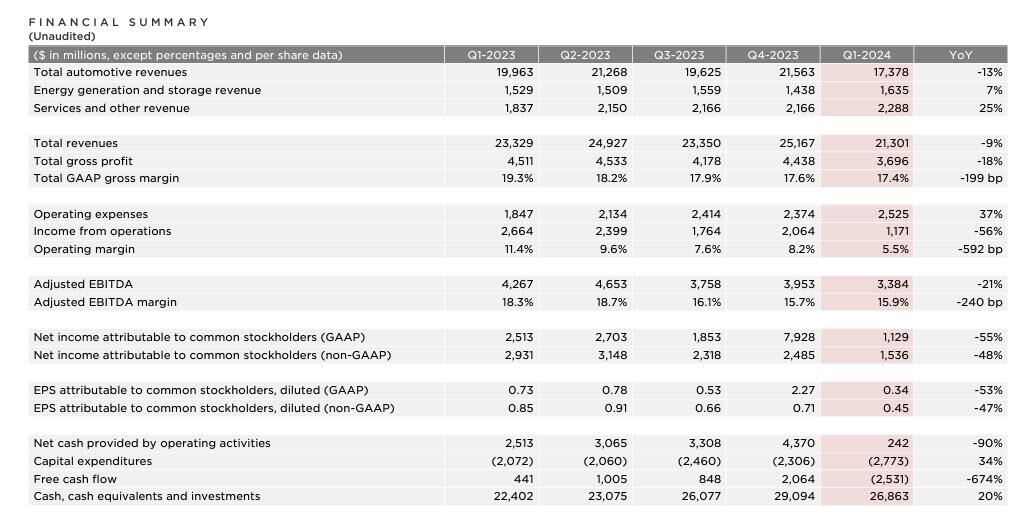

With all that in mind, here is what the company reported for the first quarter:

- Q1 Revenue $21.3BN, down 9% YoY, and missing estimates of $22.3BN

- Q1 Adj EPS 45c, down 47% YoY, and missing estimates of 52x

- Q1 Operating income $1.17BN, down 56% YoY and missing estimates of $1.53BN

- Q1 Automotive Gross Margin Ex-Regulatory Credits 16.4%, missing estimates of 17.6%

- Q1 Free Cash Flow -$2.53BN, vs +$441MM YoY and missing estimates of +653.6MM

In short: a hot mess as summarized below:

Some more details on the results, starting with revenue which declined 9% YoY in Q1 to $21.3B. YoY. revenue was impacted by the following items:

- - reduced vehicle average selling price (ASP) YoY (excl. FX impact), including unfavorable impact of mix

- - decline in vehicle deliveries, partially due to the Model 3 update in the Fremont factory and Giga Berlin production disruptions

- - negative FX impact of $0.2B1

- + growth in other parts of the business

- + higher FSD revenue recognition YoY due to release of Autopark feature in North America

Turning to operating income, that decreased YoY to $1.2B in Q1, resulting in a 5.5% operating margin. YoY, operating income was primarily impacted by the following items:

- - reduced vehicle ASP due to pricing and mix- increase in operating expenses partly driven by AI, cell advancements and other R&D projects

- - cost of Cybertruck production ramp

- - decline in vehicle deliveries, partially due to the Model 3 update in the Fremont factory and Giga Berlin production disruptions

- + lower cost per vehicle, including lower raw material costs, freight and duties

- + gross profit growth in Energy Generation and Storage including IRA credit benefit

- + higher FSD revenue recognition YoY due to release of Autopark feature in North America

The company's cash at quarter-end was $26.9B, a sequential decrease of $2.2B which was the result of negative free cash flow of $2.5B, driven by an inventory increase of $2.7B and AI infrastructure capex of $1.0B in Q1.

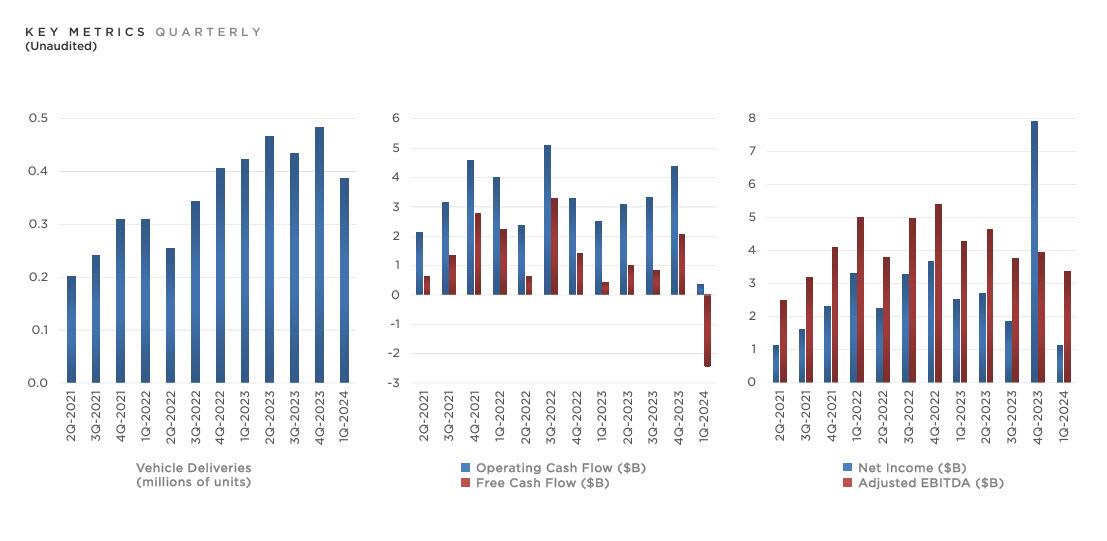

While we already knew the operating summary, here it is again:

Charted, the results are anything but pretty:

And while the disappointing results would likely have been enough to hammer the stock even more after hours, TSLA is soaring due to these four paragraphs in the company's "product outlook" section, which promise what everyone has been hoping for: cheaper cars are coming and sooner than expected, meaning Reuters indeed lied (it also mentions the robotaxi whose August 8 unveil Musk hinted at recently):

We have updated our future vehicle line-up to accelerate the launch of new models ahead of our previously communicated start of production in the second half of 2025.

These new vehicles, including more affordable models, will utilize aspects of the next generation platform as well as aspects of our current platforms, and will be able to be produced on the same manufacturing lines as our current vehicle line-up.

This update may result in achieving less cost reduction than previously expected but enables us to prudently grow our vehicle volumes in a more capex efficient manner during uncertain times. This would help us fully utilize our current expected maximum capacity of close to three million vehicles, enabling more than 50% growth over 2023 production before investing in new manufacturing lines.

Our purpose-built robotaxi product will continue to pursue a revolutionary “unboxed” manufacturing strategy.

An earlier launch of cheaper EVs would be a reversal of the Reuters news around a cheaper Tesla model being pushed back, which musk already pushed back on. Arguably Tesla does not need to just release a model to compete with a Toyota Camry to see further growth. BYD, for example, has dozens of models out there for consumers to choose from. Tesla, meanwhile, has opted for less model variety and that has contributed to some of the challenges they’ve faced.

Reuters is lying (again)

— Elon Musk (@elonmusk) April 5, 2024

Here are some other highlights from the company's Outlook section:

- Volume: Our company is currently between two major growth waves: the first one began with the global expansion of the Model 3/Y platform and we believe the next one will be initiated by advances in autonomy and introduction of new products, including those built on our next generation vehicle platform. In 2024, our vehicle volume growth rate may be notably lower than the growth rate achieved in 2023, as our teams work on the launch of the next generation vehicle and other products. In 2024, the growth rates of energy storage deployments and revenue in our Energy Generation and Storage business should outpace the Automotive business.

- Cash: We have sufficient liquidity to fund our product roadmap, long-term capacity expansion plans and other expenses. Furthermore, we will manage the business such that we maintain a strong balance sheet during this uncertain period.

- Profit: While we continue to execute on innovations to reduce the cost of manufacturing and operations, over time, we expect our hardware-related profits to be accompanied by an acceleration of AI, software and fleet-based profits.

Some more details from the presentation:

- Tesla notes (on page 7) that it produced 1,000 Cybertrucks in a single week in April. Positive ramping signs, although the Cybertrucks were recently recalled due to issues with its pedal.

- Working capital remains a big issue: global vehicle inventory rose to 28 days, a huge jump from the 15 days at the end of the last quarter.

- Tesla said that production at Gigafactory Shanghai was down sequentially due to seasonality and planned shutdowns around Chinese New Year in Q1. It also notes that demand typically improves throughout the year, and as it enters new markets, "such as Chile, many of them will be supplied from Gigafactory Shanghai.”

- There was the following interesting acknowledgmenet: “Global EV sales continue to be under pressure as many carmakers prioritize hybrids over EVs. While positive for our regulatory credits business, we prefer the industry to continue pushing EV adoption, which is in-line with our mission.”

Turning to the company's battery division, Tesla deployed a record amount of energy storage for the quarter – 4,053 megawatt-hours – topping its prior record by 2%. Tesla has become a dominant force in the storage business, vying with competitors such as Fluence Energy and Sungrow Power Supply to deploy big batteries that can back up solar plants or prevent blackouts on the electric grid. That market is growing at breakneck speed, with US deployments in the fourth quarter jumping 358% compared to the same period of 2022, according to Wood Mackenzie.

Still, as Bloomberg notes, probably for the first time since it bought SolarCity, Tesla didn’t disclose its quarterly deployments of solar, instead noting the following: "In its Energy Generation and Storage business: “Revenues were up 7% YoY and gross profit was up 140% YoY, driven by increased Megapack deployments, partially offset by a decrease in solar deployments." In Q4, the company deployed 41 megawatts.

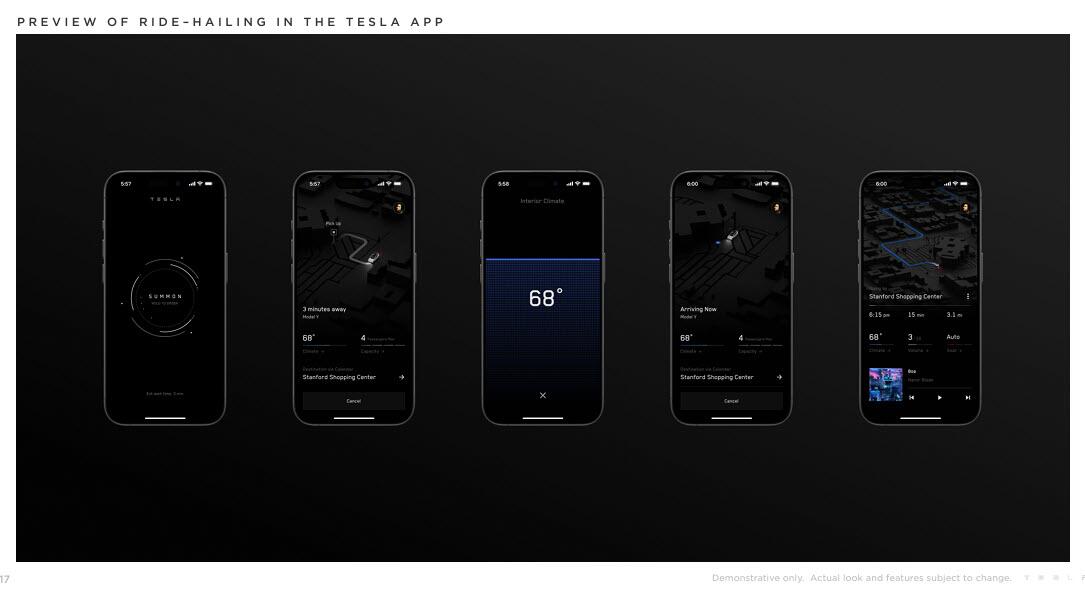

Another notable highlight: the company has previewed what ride-hailing will look like using the TSLA app. Watch out Waymo and Uber, TSLA is coming for you:

And so, with the stock having cratered in the past week, sliding for a record-matching 7 consecutive days, the market is finally happy with what Musk revealed and the stock is sharply higher after hours, surging some 6% and erasing the 4 most recent days of losses...

... although much will depend on Musk's tone during the earnings call, where TSLA's overtime fate will be decided.

https://ift.tt/J4njUfY

from ZeroHedge News https://ift.tt/J4njUfY

via IFTTT

0 comments

Post a Comment