Albert Edwards Notices "Something Shocking" In The "Transitory vs Persistent Inflation" Debate

Earlier this week, following the news from NBER that the covid recession lasted all of two months making it the shortest recession in history, we showed that opinions on wall street diverged as to whether the economy was in early cycle (as JPMorgan claims), mid cycle (which has been Morgan Stanley's view) or late cycle, as Deutsche Bank suggested. Picking up on this debate, in his latest note the ever skeptical Albert Edwards writes that one question that bothers him "is whether this recovery should really be considered a new economic cycle or merely a continuation of the old one, briefly interrupted by the pandemic" a view which we wholeheartedly agree with.

As Edwards explains, normally in a recession, especially at the end of a record long 130-month cycle like the one we saw up to February last year, excesses like too much leverage are purged and there is a sort of reset. Of course, this time that did not happen and instead the system doubled down on leverage. So "to the extent that did not happen due to super-sized monetary and fiscal largesse, are those vulnerabilities still lurking with the potential to trigger another recession much earlier than anyone suspects" Edwards cautions adding that "would definitely be a major market shock." There is more on this in the full note which pro subs can find in the usual place.

But while we doubt this debate will be resolved any time soon, what caught our attention was another observation made by Edwards relating to the other key debate raging right now - whether inflation is transitory or persistent.

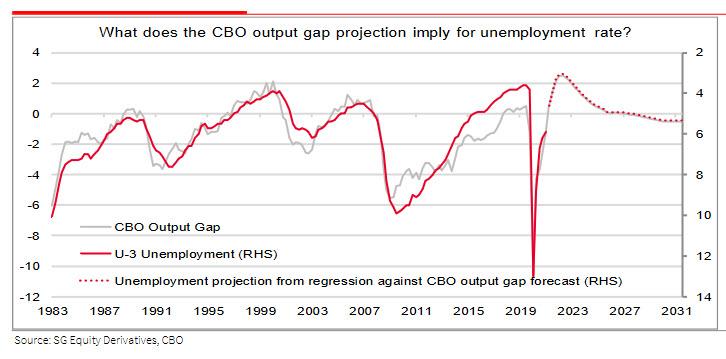

Edwards writes that while discussing his business cycle observations with his colleague Jitesh Kumar, he noticed "something shocking" - in its latest forecast, the Congressional Budget Office(CBO) have massively revised their calculations for the US output gap which as Edwards explains, "suggests US inflationary pressures are far hotter than previously thought."

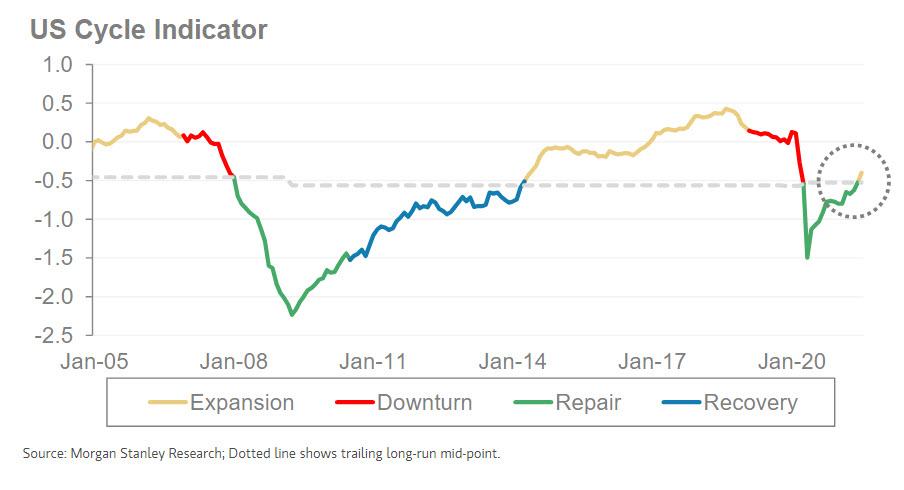

For those unfamiliar, the 'Output Gap' is important because many economists, especially Keynesian economists, tend to believe inflation only shows up when the economy is growing beyond potential capacity constraints. Normally in a recession as demand collapses it takes many years for the output gap to return from disinflation/deflation-inducing negative territory back to zero, and then beyond that into positive (inflationary) territory. Not this time though. Indeed, this is an observation also made by Morgan Stanley over the weekend, when the bank's Chief Cross-Asset Strategist Andrew Sheet noted that this has been a remarkable cycle in that we went from Downturn to Repair and then directly to Expansion without spending the requisite 35 or so months in the Recovery phase.

So going back to the Edwards note, he points out that similarly, "the CBO have had a total rethink and believe the economy will be operating 2% beyond full capacity as early as Q1 next year!" Edwards explains that "if unemployment follows its traditional close correlation with the CBO output gap, we could reach record low levels of unemployment far sooner than anyone expects."

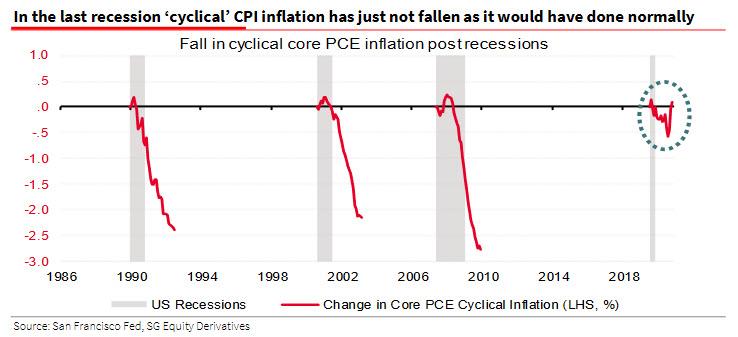

There's more: Jitesh also flagged a recent articlefrom the San Francisco Fed which splits core PCE inflation into a cyclical component and an acyclical (uncorrelated to the domestic output gap) inflation time series (link). As Jitesh writes, "to get directly to the point – the following chart shows the cumulative change in cyclical core PCE inflation over the three years following a recession in the US. It has “This time is different” writ large – a combination of timely monetary/fiscal support has managed to interrupt the “cycle” in the US. Normally 15 months after the beginning of the previous three recessions in the US, cyclical core PCE was down between 0.5% to 1.5% (see chart below), whereas it is above pre-recession levels this time around.”

As Edwards concludes, this is "food for thought indeed to challenge the prevailing ‘high inflation is transitory’ viewpoint."

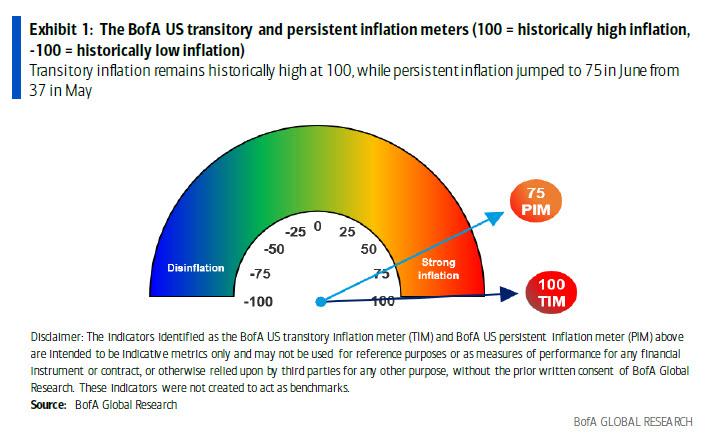

To this, all we can add is that as explained previously, the Fed has bet its remaining credibility on the absolutely critical assumption that inflation is transitory, and not, say, permanent, even though real-time inflation measures from Bank of America show just that.

But if the above observations are accurate and if inflation proves to be "non-transitory" as soon as Q1 of 2022 when the output gap is filled then the last two years of the Biden admin (with Powell long gone and replaced by some uber dove) will be very, very messy.

https://ift.tt/3iBoL42

from ZeroHedge News https://ift.tt/3iBoL42

via IFTTT

0 comments

Post a Comment