An 'Unexpected' Systemic Crisis Is Assured Tyler Durden Sun, 08/16/2020 - 08:10

Authored by Alasdair Macleod via GoldMoney.com,

Downturns in bank credit expansion always lead to systemic problems. We are on the edge of such a downturn, which thanks to everyone’s focus on the coronavirus, is unexpected.

We can now identify 23 March as the date when markets stopped worrying about deflation and realised that monetary inflation is the certain outlook. That day, the Fed promised unlimited monetary stimulus for both consumers and businesses, and the dollar began to fall.

The commercial banks everywhere are massively leveraged and their exposure to bad debts and a cyclical banking crisis is now certain to wipe many of them out. In this article we look at the global systemically important banks — the G-SIBs — as proxy for all commercial banks and identify the ones most at risk on a market-based analysis.

Introduction

In these bizarre markets, the elephant in the room is systemic risk — visible to all but simply ignored. This is partly due to everyone in government and central banks, as well as their epigones in the investment industry and mainstream media, believing our economic problems are only a matter of Covid-19. In other words, when the pandemic is over normality will return. But Covid-19 has acted like a conjurer’s distraction: it has deflected us from the consequences of Trump’s trade wars with China and the liquidity strains that surfaced in New York last September when the repo rate soared to 10%.

The liquidity strains and the severe downturn in the stock markets that followed earlier this year before mid-March have been buried for the moment in a tsunami of central bank money. Liquidity problems following last September’s repo crisis and the S&P 500 index collapsing by one third between 19 February and 23 March were a clear signal that the multiyear cycle of bank credit expansion had already peaked. Ever since the last credit crisis in 2008, the banks had recovered their lending confidence and expanded bank credit, a classic expansionary phase.

If we take US dollar M1 money away from M2 money, we get a rough approximation of the growth of bank credit and that tells us two things. It has slightly more than doubled in the long expansionary phase, and since early June, despite the unprecedented injection of base money into the banking system by the Fed, bank credit is now stalling.

We are moving into this contractionary phase of credit with some significant banks dangerously leveraged. That is usual ahead of a credit crisis, but never to the extent we are experiencing today. And thanks to Covid-19, this danger is universally ignored.

Why bank market capitalisations matter

Not only are some of the global systemically important banks (G-SIBs) highly leveraged on their balance sheets, but in most cases stock markets are valuing their equity at a fraction of their balance sheet book values, contrasting with outrageously high valuations for non-financial stocks in the most severe economic downturn ever seen in peacetime. It would be reasonable to expect a new bull market for equities to include the banking sector, but this is not so.

Table 1 below illustrates the point by incorporating the combination of balance sheet gearing and stock market valuations for all the G-SIBs to give a multiple of balance sheet assets to market capitalisation, ranking them from most dangerous to the least on this measure. The only banks in the list with market capitalisations higher than balance sheet equity — price to book ratios of more than one — are North American banks, which might explain why critical leverages are not recognised as a systemic problem in US financial markets.

The three highest leverages are of Eurozone banks: remember these are just the G-SIBs — there will be many large and smaller commercial banks as highly leveraged which are not on this list.

To have your equity valued at less than 20% of book value, which is the indignity suffered by the French bank, Société Générale, should send warning signals to French banking regulators. But they insist on only looking at the ratio of balance sheet assets to balance sheet equity; which for Soc Gen is still an eye-watering 21.4 times. Unlike the regulator, investors appear to think this bank is most likely bankrupt, its share price little more than a call option bet on its survival. To be clear, the effect of every euro of new bad debts declared by this bank is magnified 118.8 times in pain for shareholders. It is worth taking a moment to let the implications sink in and to understand how little it would take to bankrupt the bank.

It is a problem which particularly affects banks in the Eurozone. In its twin towers in Frankfurt, a mere sneeze could destabilise Deutsche Bank. In France the regulator dismisses the balance sheet gearing and share prices with a Gallic shrug. Société Générale’s balance sheet gearing is 21.4 times, Credit Agricole’s is 28.1 times — the highest of all the G-SIBs — and BNP is 20.1 times. And experience tells us that the numbers reported by banks are bolstered by their gaming of the regulatory system, which is why when a bank fails the outcome is always worse than the pre-failure numbers would suggest possible.

Large banks do not operate in national silos, having trade finance activities, foreign exchange and derivative trading, lending in foreign currencies and even substantial branches and subsidiary operations abroad. The idea that a crisis in the Eurozone, or China for example, can be contained to national boundaries is wishful thinking. With the exception of Wells Fargo, US G-SIBs come out better than those of other jurisdictions, but that will not save them from a systemic crisis originating elsewhere.

While we can point to the end of the credit cycle, there is no doubt that Covid-19 has precipitated a more immediate crisis. We are now seeing the initial effects on GDP of lockdowns being reported, and doubtless their subsequent revisions will make them even worse. The official talk is of a V-shaped recovery, and indeed, government spending has increased with that result in mind. It is reported that we, the general public, have saved our money in the lockdown, and that we will resume spending as normal once Covid-19 passes. All that failing businesses have to do is just hang on in there, and as President Reagan famously put it, wait for the knock on the door: “I’m from the government and I’m here to help”.

But there is a truth swept under this proposition: in both the US and UK, with their consumer-driven societies in common, a Pareto 80% of employees live paycheque to paycheque. Those whose spending has fallen and upon which a spending recovery is banked are mostly retirees, who are unlikely to make much difference to a consumer-driven economy by splashing out when all lockdowns end.

Governments have introduced emergency plans. The US Government is distributing money by metaphorical helicopters, and Britain has a furlough scheme and tax deferments. But they do little to alleviate the concerns of highly leveraged commercial bankers, facing the prospects of soaring bad debts. Bank balance sheet asset values to market capitalisation ratios strongly suggest the banking system cannot cope with what is ahead.

The US and UK governments have also implemented or announced schemes to help employers, and doubtless are prepared to step up their support, particularly for those who employ large numbers of workers. But these measures cannot change the fact that many businesses and individuals face bankruptcy. The banks know it, and because their actions to protect themselves from bad debts in the non-financial economy are restricted for fear of making things worse, their actions in the financial economy will become important.

The dilemma is this. As a banker, do you take the view that financial assets will continue to grow in value, so that by increasing your bank’s involvement you might be able to trade your way out of trouble by expanding financial and investment activities, or do you crack down on financial risk and commitments, in the hope that you will release balance sheet space to handle bad debts in the real economy?

Presumably, central banks are rooting for the former but among their commercial charges it appears the latter view prevails. And with balance sheet gearing as it is, who can blame them.

Not only have many G-SIBs reduced or closed their investment banking activities following Lehman, but their recent experience in the derivative markets for gold and silver will probably encourage them to reduce their books in a wide range of other financial activities. We cannot know if this has impacted on equity markets yet; but the initial effect is likely to drive prices higher as market making liquidity deteriorates before trend-chasing buyers stop chasing rising trends. Given the strength of US equity indices, this is precisely what we are seeing.

The direction of share prices matters

Being bureaucrats who stick to their rules, regulators ignore the market values which we all know matter in the real world. But how values in the marketplace evolve is also critical; and with equity markets buoyant, bank stocks behaving like dogs are important to identify, for therein trouble surely lies.

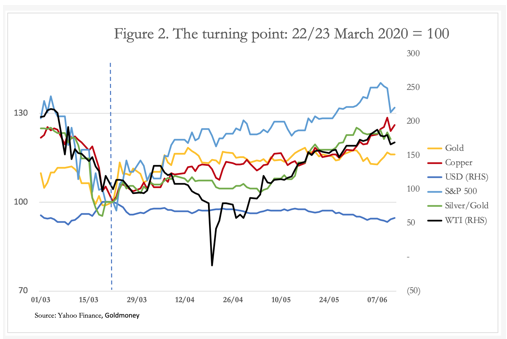

Earlier this year, in about mid-February, markets took seriously the deflationary implications of Covid-19. The dollar’s trade weighted index spiked higher in a dash for the safety of cash. Bank stock prices fell sharply as the implications of a deflation of bank credit began to be uppermost in investors’ minds. On Comex, open interest for gold plummeted from record levels and the gold/silver ratio soared to over 120. The S&P500 index collapsed from 3386 on 19 February to 2237 on 23 March, falling by a third. 23 March was also the day that the Federal Reserve announced it would unhesitatingly provide all the monetary support needed by the US economy, turning growing fears of deflation into certain inflation.

That marked the turning point for all financial markets: the dollar’s trade weighted index peaked and began to fall. The S&P500 began a new bull run and has recovered to new highs this week. Premiums over the gold spot price appeared on Comex, the gold silver ratio began to fall rapidly, and the copper price turned sharply higher. Oil turned higher as well, though temporarily it dipped in April due to technical factors before rising to join the other bulls.

Some of these effects are shown in Figure 2. The common factor was the downturn in the dollar, reflecting the switch from deflationary fears to expectations of monetary inflation. The dollar lost its deflation safe-haven status and was even sold for other currencies, particularly the euro. At the same time every dollar hedge, from equities to commodities, and even bitcoin began to rise. Financially, this is when the tide turned, and if the banks were solid, their share prices should have joined the upward trend. Therefore, all we need to do is look at those struggling to get off their lows to identify the G-SIBs most likely to be in real trouble.

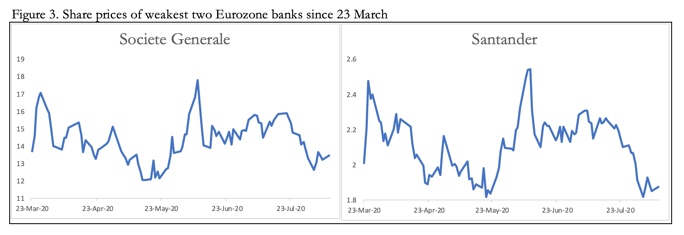

In the Eurozone the two standouts are Société Générale and Banco Santander. Their charts are from 23 March, the day when stock markets took off, and are shown in Figure 3.

As recently as 17 February Société Générale hit €31.93 before collapsing to €11.77 on 15 May. And as the chart shows, it is like a floored boxer struggling to get up off the canvas. Coupled with a ratio of assets to market capitalisation of a staggering 118.8 times, this bank’s ability to survive the slightest knock is very doubtful.

Santander’s weakness is a mild surprise. With assets to market capitalisation of 48.8 times, it is dangerously geared, but not so much as other Eurozone G-SIBs, such as Deutsche Bank on 79.5 times. Nevertheless, investors have sold it down from €3.955 on 12 February to €1.8232 on 19 May. Again, this bank is rated as likely doomed by the markets.

In this analysis we are restricting our commentary to those banks who post-March are behaving like dogs. But that does not necessarily mean other banks are safe. Deutsche Bank, for example, traded at under €5 in March and have rallied to €8.25, in theory recovering with equity markets. But on 14 February it had already collapsed from €10.19, more than halving. Furthermore, before the Leman crisis, the shares were as high as €91.625. Commerzbank, not on the G-SIB list, is similarly afflicted having recovered from a low of €3.05 on 19 March to €4.873 currently. But its share price was over €300 in March 2007, and its ratio of assets to market capitalisation is 76 times, similar to Deutsche Bank’s. These two large private banks are unconscious on their feet and could topple at the slightest nudge.

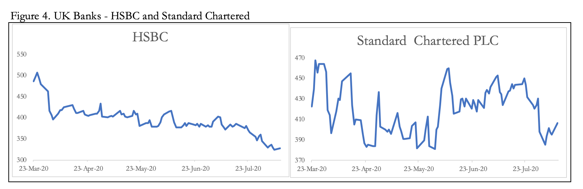

There are two British banks with a similar performance, close to their lows for the year. At 63.8 times Barclays has the highest ratio of balance sheets assets to market capitalisation, but it is not one of them. The British banks suffering most in the markets from 23 March are Standard Chartered and HSBC, shown in Figure 4.

HSBC peaked at 791.70p in January 2018, declining to 584.50p on 9 February, since when it has continued its decline. With a price to book of 51% it is still rated in the market better than many other G-SIBs. HSBC’s obvious problem is the China connection and sanctions against Hong Kong. With total assets to balance sheet equity of 14.8 times, HSBC is on a par with Standard Chartered at 14.3 But with Standard Chartered’s price to book at 23.9% and HSBC’s at 51.1%, the former appears to be the more vulnerable. However, geopolitics will likely mean that HSBC is also far from safe.

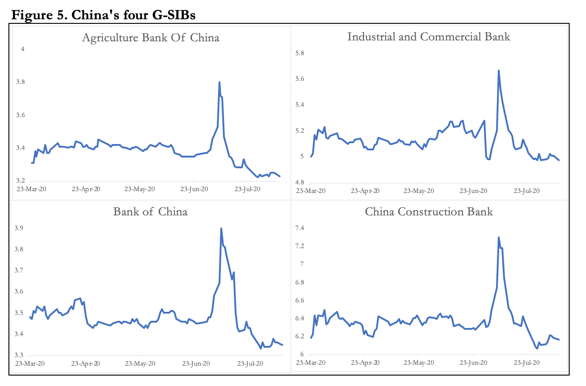

This brings us to our last category, China. All four Chinese G-SIBs’ share prices have collapsed, having initially enjoyed the post-23 March rally. And it is worth noting that the Shanghai Composite Index also turned higher on 23 March, from 2660 to 3320 this week. These major banks, government controlled, should have maintained their rally with the market and not declined. Figure 5 shows them all to be at or near their lows. And these banks, surely, are the safest in China, being organs of the state.

Following the easing of China’s lockdown, the Shanghai composite index rallied strongly, with retail investors piling into stocks. The authorities encouraged the appearance of a return to normality, with the state-run China Securities Journal in a front-page editorial talking up a healthy bull market and the wealth effect of rising share prices underpinned by an improving economy. Bank shares initially benefited, all hitting a peak on 7 July. The broader market topped out two days later and is down only 3.5% from the top. But the share prices of these major banks have all fallen.

The Chinese regulators have been cleaning up shadow banking activities and reforming the wealth management product market (WMPs), to which banks are exposed to an estimated $3.3 trillion equivalent. Not only has this been an immensely important business activity for them, but the banks have given explicit and implicit guarantees to investors absolving ownership of WMPs from risk. According to a Moody’s note released on 7 August, implicit guarantees amount to over half of these WMPs.

The problem for the regulator is that the banks are taking on the risk of changes in underlying asset values instead of investors. Understandably, they have sought to change what has become a systemic issue of major importance. Was it this that was behind the “official” recommendation for investors to pile into equities, given that before the stock market rally, the implicit guarantees to WMP holders were threatening to undermine the banks, and they needed some breathing space?

We will probably never know the truth, but recently the regulators decided to extend the deadline for risk transfer from banks to WMP owners by a year. The signal from the performance of Chinese bank shares in recent weeks, particularly when contrasted with the performance of the rest of the Chinese equity markets, is that risk perceptions for bank shareholders have become significantly elevated.

Then there is geopolitics. Inward investment flows through the Hong Kong – Shanghai connect has been effectively stopped by US sanctions. As noted above, banks such as HSBC are likely to be targeted next by the US administration, extending extra systemic risk into the Chinese banking system through their banking relationships.

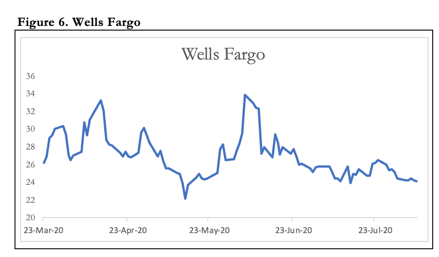

The last bank with a share price near its lows is Wells Fargo, which is Figure 6.

In January, Wells Fargo’s stock traded at $54, halving between then and 23 March, when everything in the world of finance changed. An unfortunate comparison perhaps, but WFC’s subsequent performance echoes that of Société Générale shown in Figure 3, which, as we noted above, is like a floored boxer struggling to get up off the canvas. Of the North American G-SIBs, it stands out with the greatest discount to book value, giving it a total asset to market capitalisation leverage of 18.6 times. Its balance sheet ratio to equity is a mere 10.4 times, which compares with that of JPM Chase at 10.3. Undoubtedly, US bank regulators see no problem here, though markets are telling us another story.

In conclusion, through our market-based approach we have identified some of the likely weak points in the global banking system: others will exist in banks not on the G-SIB list of which Commerzbank cited above is an example. The surprise finding, perhaps, is the systemic threat from China’s large banks combined with two British G-SIBs operating in Hong Kong and the Far East. If the US deep state sees China’s financial system as worthy of further attack, it could be responsible for the collapse of the global banking system.

Unquestioned bail outs by the state would be the most optimistic outcome in a G-20 world which has passed regulations to permit bail-ins. Any jurisdiction going down the bail-in route will probably make things worse by shifting the failure onto the shoulders of bank bond holders and large depositors, creating disorderly runs on other banks deemed to be at risk. Our assumption must be that when any one of these dominoes topples, it will be bailed out by the relevant authorities, without hesitation.

The consequences of a global bank failure

If a G-SIB fails, then it seems logical other lesser banks will also fail. Any state which has a G-SIB failure must therefore be prepared at the outset to underwrite its whole banking system. It will most probably turn into a wider problem with the result that the global banking system will fall into the hands of major governments.

Initially, the inflationary implications can only be guessed at. How the crisis affects economic prospects and undermines financial assets will feed into those guesses. But when banks are owned and controlled by the state, the impediment of the bank credit cycle to inflationary input will be replaced by the direction of central bankers and treasury ministers. Global monetary inflation to buy off a gathering slump will become unhindered and unprecedented.

The effect of a banking crisis on wider financial assets is an analysis yet to be made. We have seen how 23 March became the turning point for markets, which spinning on a sixpence adjusted expectations from credit deflation to unlimited inflation of fiat currencies. It is also the moment the clock started ticking for a full and final market and currency crisis. A consequence has been the start of dollar weakness, likely to persist. Foreign flows out of the dollar and dollar assets are likely to continue, or even accelerate. With foreigners being increasingly net sellers of US financial assets, not only will the foreign exchange rate for the dollar continue to suffer, but with foreign divestment it will be increasingly difficult for the Fed to maintain the financial asset bubble.

That the Fed will end up financing the US Government through intermediaries under the control of the government itself will blow away the fig leaf of non-inflationary financing through QE. Monetary inflation will be laid bare for what it is, calling for a market reassessment US Treasury bond yields. In short, with a weakening dollar, however it is measured, the Fed risks losing control over government bond markets, and therefore over other financial asset prices as well.

The Fed’s success in gradually reducing funding costs for the US Treasury has relied on its unchallengeable supremacy over markets: what the Fed says, goes. Following the now imminent banking crisis, this confidence is likely to be badly damaged, and the Fed’s actions questioned by increasing numbers of market sceptics. It threatens to be a replay of the problems faced by the Bank of England in the early 1970s, when nearly every action it took failed to convince the markets. Between 1972–75, the FT30 index fell 73%, a banking crisis ensued in November 1973, price inflation roared, and in 1976 the IMF was called in to bail Britain out.

We can only conclude that a systemic crisis leading to widespread bank failures and their being taken into public sector ownership will in turn be seen by the general public and investors alike as a failure of neo-Keynesian central bank monetary policies. A banking crisis more serious than the Lehman crisis of 2008—2009 would be a stepping-stone to a wider crisis for financial asset values, leading to an increasing pace of loss of purchasing power for the dollar, whose fortunes are now bound tightly to confidence that the US budget deficit will continue to be financed. And on the dollar’s fate hangs the future of all the other paper currencies linked to it.

https://ift.tt/3g3aqtA

from ZeroHedge News https://ift.tt/3g3aqtA

via IFTTT

0 comments

Post a Comment