Futures Rise On Black Friday As Month-End Pension Selling Flood Fails To Show Tyler Durden Fri, 11/27/2020 - 08:14

According to Goldman and JPMorgan, markets were supposed to be hit with a near-record tidal wave of month-end pension funds selling (up to $160BN according to JPM) after a month of record equity putperformance over bonds. However, any selling has yet to materialize, with futures now trading higher than where they closed on Wednesday ahead of the Thanksgiving holiday, and once again within points of the all time high. Don't expect fireworks in today's subdued session which sees equity trading end at 1:00 p.m. and the bond market closes at 2:00 p.m. ET

Reopening after the Thanksgiving holiday, Dow e-minis were up 0.18%, the S&P 500 e-minis were up 0.25% to 3,636, and the Nasdaq 100 e-minis were up 0.37% in early Friday trading. Trading was subdued despite a Thursday statement from AstraZeneca that it’s likely to conduct a further global trial of its vaccine after current studies raised questions.

Political clarity has also pushed risk assets this month, as President-elect Joe Biden continues his transition to power. President Donald Trump said he’ll relinquish power if the Electoral College affirms Biden’s win, but he signaled he may never formally concede defeat, and may skip the Democrat’s inauguration.

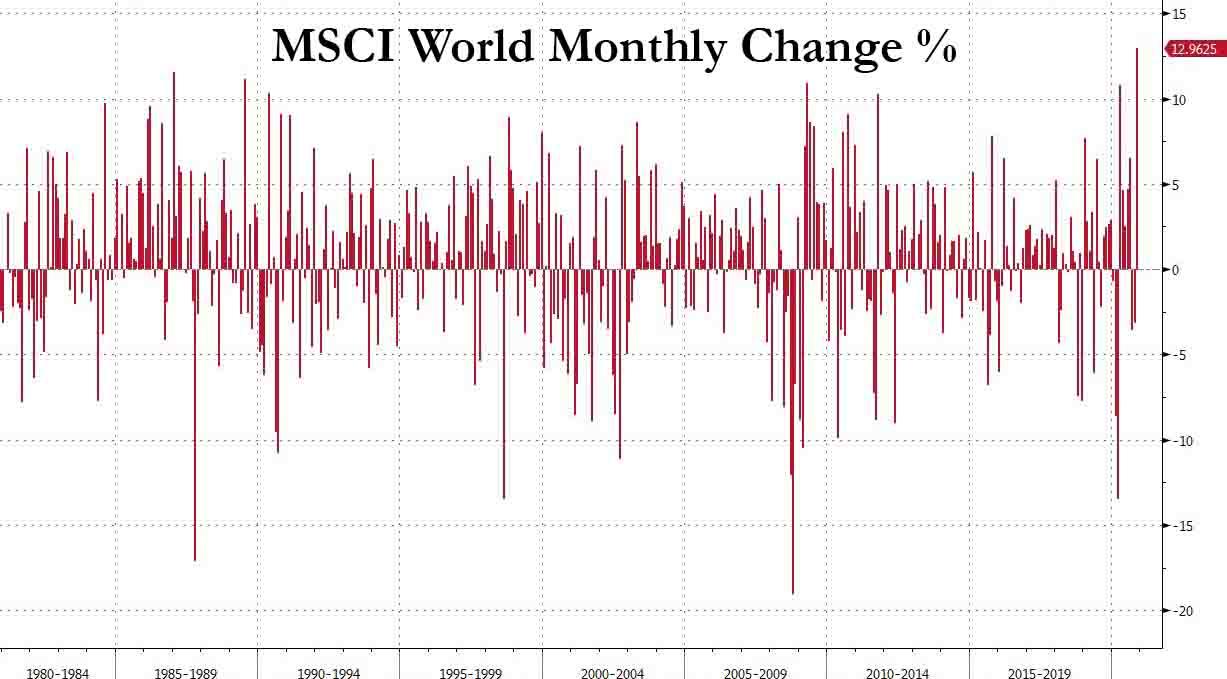

In what has been a record month for global stocks which are on track for the best month on record, up 13%, which has lifted valuations to near the highest in about 20 years...

... Wall Street’s main indexes gained more than 10% this month as investors bet on a sooner-than-expected COVID-19 vaccine and calmer global trade under President-elect Joe Biden, setting the S&P 500 for its best November ever. Still, sentiment remains fragile as the virus toll continues to rise in Europe and the U.S., while economic recoveries wobble. Investors are pinning their hopes on a swift rollout of vaccines, but the logistical challenges are considerable.

A rotation into sectors such as industrials and financials, deemed to benefit from an economic recovery, has also powered the Dow to record highs and put it on track for its biggest monthly gain since 1987. But both the indexes pulled back on Wednesday as data showed a stuttering recovery in the labor market, sending investors back to the perceived safety of technology heavyweights, including Apple Inc and Amazon.com Inc.

In Europe, the Stoxx 600 Index was up 0.1% after it fluctuated between gains and losses, with the index on track for its biggest ever monthly gain. Stock markets in Europe were subdued by doubts around the effectiveness of AstraZeneca’s COVID-19 vaccine, potentially hindering chances of the shot getting speedy U.S. and EU regulatory approvals. Electricite de France SA surged as much as 7.7% following reports that France and the EU are close to reaching a deal on nuclear regulation, while Banco de Sabadell SA plunged after terminating talks with Banco Bilbao Vizcaya Argentaria SA. putting a premature end to hopes for a return of European bank M&A.

Earlier in the session, the MSCI Asia Pacific Index added 0.2% while Japan's Topix index closed 0.5% higher, with Nidec and SoftBank contributing the most to the move. Most markets in the region were up, with China's Shanghai Composite advancing 1.1% driven by ICBC and AgBank while Australia's S&P/ASX 200 slid 0.5%. In China, data showed profits at industrial enterprises surged at the fastest pace in a single month in almost nine years in October, a further sign the country’s economic recovery is gathering pace, even if well beyond the point of credibility.

“To see whether the market will continue to have legs we will have to have confirmation of those vaccine hopes,” Credit Suisse CIO Nannette Hechler-Fayd’Herbe said in an interview with Bloomberg TV. "So very quickly now we want to see approvals, we want to see production outlooks as far as the vaccines’ broader distribution is concerned."

In FX, the Bloomberg Dollar Spot Index inched lower again, nearing a two-and- a-half year low and the dollar fell versus most of its Group- of-10 peers, with the yen leading gains along with a group of risk-sensitive currencies. The pound swung to a loss as Brexit enters a crucial few days, with U.K. and EU leaders resuming talks this weekend in an attempt to break the deadlock between the two sides.

In rates, treasuries advanced as U.S. trading resumes following Thursday’s holiday, led by long end. The 10Y was last seen at 0.855%, with yields were lower by 0.5bp to 3bp across the curve with long-end-led gains flattening 2s10s and 5s30s by 1bp-1.5bp; 10-year yields around 0.86%, richer by 2bp on the day. Expectations of buying tied to Monday’s month-end index rebalancing also underpin the market; Sifma has recommended a 2pm ET close of trading Friday. The 10-year TSY remains 4bp higher on the week after climbing more than 5bp over Monday- Tuesday amid gains for risk assets driven by vaccine development and U.S. politicial clarity, and as Treasury auctioned 2-, 5- and 7-year notes.

WTI and Brent futures have climbed off pre-European cash open lows as prices gain ahead of the OPEC/OPEC+ showdown next week (full preview available in the Research Suite) whereby markets have largely priced in the rollover of the current 5.7mln BPD cuts through Q1 2021. That being said, the recent price rally has cast doubts over the eagerness of some members to agree to this. Analysts at ING see downside risk heading into the meeting as "it is unlikely that OPEC+ surprise with a six-month rollover given the latest move in prices, while the three-month rollover is already largely priced in. Bitcoin and other digital coins steadied after posting some of the biggest declines since the onset of the pandemic.

There is nothing on today's calendar.

Market Snapshot

- S&P 500 futures up 0.2% to 3,634.50

- STOXX Europe 600 up 0.06% to 391.86

- German 10Y yield unchanged at -0.588%

- Euro up 0.04% to $1.1918

- Italian 10Y yield fell 1.4 bps to 0.49%

- Spanish 10Y yield fell 0.3 bps to 0.048%

- MXAP up 0.3% to 192.96

- MXAPJ up 0.02% to 634.40

- Nikkei up 0.4% to 26,644.71

- Topix up 0.5% to 1,786.52

- Hang Seng Index up 0.3% to 26,894.68

- Shanghai Composite up 1.1% to 3,408.31

- Sensex down 0.2% to 44,154.98

- Australia S&P/ASX 200 down 0.5% to 6,601.05

- Kospi up 0.3% to 2,633.45

- Brent futures up 0.4% to $47.97/bbl

- Gold spot down 0.4% to $1,808.71

- U.S. Dollar Index little changed at 91.93

Top Overnight News from Bloomberg

- U.K. and European Union officials will resume face-to-face trade talks this weekend with Michel Barnier, the EU’s chief negotiator, warning that big disagreements between the two sides persist

- The latest fund flow data underline how positive vaccine updates and ebbing political uncertainty in the U.S. spurred investors to pile into global equity funds. They injected more money into stock portfolios in the three weeks through Nov. 25 than in any comparable period on record, according to Jefferies Financial Group Inc. strategists, citing data from EPFR Global

- ECB policy maker Francois Villeroy de Galhau says ECB recalibration of its tools at December meeting should pay particular attention to the “duration, flexibility, and effective targeting” of policy; says he has rejected suggestions that the institution should consider writing off the public debt it bought during the pandemic, saying to do so would backfire

- France and Germany are leading efforts in Europe to make early contact with President-elect Joe Biden’s team, with the aim of accelerating talks to normalize trade relations between the U.S. and the European Union

- Health Secretary Matt Hancock asked the U.K. medical regulator to potentially bypass its European Union counterpart and approve the supply of AstraZeneca Plc’s Covid vaccine to speed its deployment

- Sweden’s economy grew 4.9% from the second quarter, Statistics Sweden said on Friday. That’s more than the 4.3% expected in a Bloomberg survey of economists, and follows an 8% contraction in the three months through June

A quick look at global markets courtesy of NewsSquawk

Asian equity markets were mixed as trade continued to lack firm direction following the holiday closure in US for Thanksgiving and lull seen across European counterparts. ASX 200 (-0.5%) was pressured amid further deterioration of Australia’s trade ties with China after the latter announced to collect anti-dumping deposits on Australia wine of around 107%-212% from Saturday which saw double-digit losses in Treasury Wine Estate before it was temporarily halted pending further announcement. The Australian coal blockage situation off Chinese ports also further deteriorated as 82 ships were now involved carrying a total value of AUD 1.1bln, with the ongoing spat overshadowing the encouraging COVID-19 development in which Victoria state reached the threshold for total elimination of the virus after 28 days of zero cases. Nikkei 225 (+0.4%) swung between gains and losses as hopes regarding an extension of COVID-19 relief measures were counterbalanced by the pressure from currency inflows, while there was plenty of attention on Tokyo Dome whose shares were untraded with a glut of buy orders at the daily upper limit after reports Mitsui Fudosan is planning to make a tender offer. Hang Seng (+0.3%) and Shanghai Comp. (+1.1%) conformed to indecision but with the mainland kept afloat after the PBoC’s tepid liquidity operations resulted to a net weekly injection of CNY 130bln and with Chinese Industrial Profits surging 28.2% Y/Y. Finally, 10yr JGBs were subdued amid the lack of firm direction across overnight markets and after mixed results at today’s 2yr JGB auction which showed a weaker b/c.

Top Asian News

- Alibaba, Tencent Put Talks to Buy iQIYI Stake on Hold: Reuters

- Covid Vaccine Delays Undermine Indonesia’s Path to Immunity

- Kim Jong Un Likely to Let His Missiles Do the Talking With Biden

- Australia’s Longest Lockdown Pays Off With No Cases for 28 Days

European majors have mostly drifted into positive territory (Euro Stoxx 50 +0.4%) following a lacklustre cash open, whilst the UK's FTSE 100 (-0.5%) remains the laggard as Brexit talks enter the final stretch, with EU's Chief Brexit negotiator Barnier out of isolation and headed to London for weekend talks; albeit, after giving EU27 a downbeat prognosis of the current state of talks. US futures have also been climbing off lows in tandem with EU futures on the holiday-shortened trading day with ES +0.2%, NQ +0.4% and RTY -0.2%. Sectors in Europe are mixed with no clear risk-profile - IT remains the top performer while Oil & Gas erased losses and now resides towards the top of the pile amid price action in the oil complex. Travel & Leisure fell and is now the laggard in what seems to be more of a retracement of the recent firm performance. In terms of individual movers, Banco Sabadell (-13%) plumbed the depths after the Co. terminated merger discussions with BBVA (+3%) as the parties did not achieve an agreement on the exchange ratio of both entities. AstraZeneca (-0.8%) is modestly softer as the AstraZeneca/Oxford University vaccine is set to undergo a new global trial to appease critics questioning the claim that the vaccine can protect up to 90% of people against COVID-19, however, this is not expected to impact regulatory approval in the UK. Finally, Indivior (-15%) shares slumped amid reports of a claim filed by Reckitt Benckiser (-0.9%) for GBP 1.07bln.

Top European News

- ECB Signals Bank Dividend Ban Could Be Cautiously Lifted in 2021

- VW CEO Says He Has ‘Old, Encrusted’ Structures Left to Break Up

- BBVA, Sabadell End Takeover Talks in Disagreement Over Price

- Danske Bank’s Watchdog Orders Fresh Probe Into Debt Errors

In FX, the Kiwi is just edging its Antipodean peer in first place among G10 majors, and fittingly perhaps with assistance from the NZ Treasury noting that the strong recovery in Q3 consumption will provide an upside skew to forecasts for overall growth in the quarter. Hence, Nzd/Usd is establishing a firmer base above 0.7000 and Aud/Nzd appears anchored to 1.0500 even though the Aussie is benefiting from ongoing Greenback weakness to inch closer to 0.7400 irrespective of yet more China trade angst as Beijing aims extortionate anti-dumping deposits on wine imports after finding fault with the environmental quality of coal. On a brighter note, Australia’s underlying cash deficit for the 4 months to October was narrower than expected.

- JPY/CAD/EUR/GBP - Also firmer vs the Buck as the Yen probes 104.00, Loonie 1.3000 regardless of a downturn in crude prices and dovish comments from BoC Governor Macklem, Euro retains grasp of the 1.1900 handle and Sterling straddles 1.3350. However, Eur/Usd remains capped ahead of 1.1950 amidst ongoing Polish and Hungarian objections to the EU Budget and Rescue Fund, while Cable is hampered and Eur/Gbp propped over 0.8900 on the back of Brexit uncertainty as UK-EU trade talks continue to draw a blank on the main outstanding irreconcilable issues. Indeed, Brussels is said to be growing exasperated and chief negotiator Barnier’s latest update to envoys was described as not that bright before he returns to London for further face-to-face discussions.

- CHF/DXY - The Franc is lagging somewhat, albeit still firmly beyond 0.9100 as the Dollar underperforms more broadly and index struggles to keep sight of 92.000 within a 92.053-91.868 range. Month-end factors are stacked against the Greenback and the lack of US participation as many extend their Thanksgiving holiday into the weekend leaves the DXY prone and only just holding off its 2020 low (91.740).

- SCANDI/EM - Mixed trade as the aforementioned retracement in oil offsets some positives for the Nok via firm retail sales and official labour data also eclipsing estimates for a more pronounced rise, while Swedish Q3 GDP also beat consensus, but largely irrelevant given yesterday’s Riksbank QE extension and expansion to leave the Sek lagging. Conversely, cheaper crude has helped the Try get over any concerns raised by the CBRT revising bank reserve ratio requirements and the regulator raising its FX and Gold holding estimates as a result, while the Cnh and Cny have been cushioned by a net weekly PBoC liquidity injection and Chinese industrial profits jumping 28.2% y/y. Elsewhere, the Brl will return to reflect and digest comments from Brazil’s Treasury Secretary stressing the need to tighten the fiscal reins and observe discipline in order to bring down long term rates.

- BoC Governor Macklem said vaccine news has been encouraging but they still project the economy will be operating below potential into 2023 and the economy will still require extraordinary monetary policy support as it recuperates. Macklem stated that borrowing costs are to remain very low for a long time and the Bank has committed to stop buying government bonds when recovery is well underway and most likely before inflation reaches 2% target. However, he added that there is a lot more room to purchase more government debt and do have capacity to do more if required, while negative rates are in the toolkit but they would not be terribly helpful at this time. Furthermore, Macklem stated they could potentially reduce the effective lower bound without going negative which is at 25bps and that it could be a bit lower. (Newswires)

In commodities, WTI and Brent futures have clambered off pre-European cash open lows as prices coattail on gains seen across the equity-sphere, and ahead of the OPEC/OPEC+ showdown next week (full preview available in the Research Suite) whereby markets have largely priced in the rollover of the current 5.7mln BPD cuts through Q1 2021. That being said, the recent price rally has cast doubts over the eagerness of some members to agree to this. Analysts at ING see downside risk heading into the meeting as "it is unlikely that OPEC+ surprise with a six-month rollover given the latest move in prices, while the three-month rollover is already largely priced in. So anything less than a three-month extension will likely be seen as bearish." Further, OPEC and OPEC+ experts are poised to meet today in preparation for the main event, whilst Saudi Arabia and Russia have invited delegation heads of the JMMC to hold informal consultations on Saturday at 13:00GMT, EnergyIntel's Bakr citing sources, thus weekend reports can be expected. Nonetheless, WTI Jan has reclaimed USD 45/bbl-status (vs. low 44.55/bbl) whilst Brent Feb re-tests USD 48/bbl (vs. low 47.35/bbl). Elsewhere, spot gold and silver exhibit somewhat of a holding pattern which reverberated from the APAC session amid lower volumes and a lack of fresh catalysts. Spot gold sees itself meandering just north of USD 1800/oz with the 200DMA residing just below the figure at 1799/oz, while spot silver fails to make much headway above USD 23.00/oz. Elsewhere, LME copper approached seven-and-a-half-year highs in light of the vaccine updates this month raising demand hopes. Finally, Chinese ferrous futures traded firmer overnight, with iron ore futures notching its third week of gains whilst hot-rolled coal prints its sixth amid depleting stockpiles prompted by demand hopes.

US Event Calendar

- Nothing major scheduled

DB's Jim Reid concludes the overnight wrap

Happy Black Friday. So far this week I’ve bought about 20 pairs of trousers from GAP in their sale. I only want about 4 pairs but as I can’t go to the shop at the moment I bought 10 in different fits last weekend in a Black Friday promotion only to find that on Monday they issued an even bigger sale. So I bought them all again with a view to sending the others back. Then I realised too late that customer service would have refunded me the difference. So I now have 20 pairs when I only need 4. Not for the first time this week my wife thinks I’ve gone mad. At least not being American I don’t have to try them on directly after Thanksgiving dinner or I may need to send them all back and get a bigger size.

With the US out on holiday, risk assets lost ground again yesterday as investors grappled with the likely spread in the pandemic over the colder winter months ahead as well as potential disruption with AstraZeneca’s vaccine rollout. Following the falls in US equities the previous day, futures there took a turn lower around the time of the European close, and the STOXX 600 itself saw a slight -0.12% fall as cyclicals including energy (-1.42%) and financials (-0.65%) led the moves lower. Other risk assets struggled too, with Brent crude oil prices shedding -1.67% as they came down from their post-pandemic high the previous day, though the traditional industrial bellwether of copper managed to advance another +1.40% to reach a 6-year high.

On the coronavirus, the main news yesterday was that increasing questions were being asked of the AstraZeneca/Oxford vaccine, with AstraZeneca’s CEO saying that the company was likely to conduct a further trial to test the vaccine’s efficacy. As you may recall, the average efficacy of the vaccine was found to be at 70% when the news came out on Monday, but this was an average of two different dose regimens, in which one had 90% efficacy where there was a halved first dose and a standard second dose, whereas the other had 62% efficacy. However, it’s since come out that the more effective dose came out because of an error in the amount of vaccine put into some vials, and the head of the US Operation Warp Speed has said that those who received this dose were limited to those aged 55 or below, and we know that lower age groups are at lower risk anyway.

In our view the US can afford to be more strict with this vaccine as they have more adequate near term supplies of Pfizer/BioNTech and Moderna. For Europe, and specifically the U.K., they may place more reliance on the data seen so far in their local jurisdiction and the regulatory approval process seems to be already in full flow. Indeed Bloomberg reported overnight that UK Health Secretary Matt Hancock has asked the UK medical regulator to potentially bypass its EU counterpart and approve the supply of AstraZeneca’s vaccine to speed its deployment. In addition and highlighting the importance of AstraZeneca’s vaccine for EM, Indian officials have said this morning that they will consider the dosing regimen with lower efficacy of 62% for granting regulatory approval adding that the efficacy of 62% is good enough for approval and use if it clears regulatory hurdles.

Overnight we got further signs from President Trump that the US presidential transition will be smooth as he said that he will relinquish power if the Electoral College affirms Democrat Joe Biden’s win. However, he added that he may never formally concede, and may not attend the Democrat’s inauguration.

Asian markets are a little up and down this morning with the Nikkei (+0.44%) and Kospi (+0.13%) higher while the Shanghai Comp (-0.08%), Hang Seng (-0.21%) and ASX (-0.53%) are all down. Futures on the S&P 500 are down -0.11% while European futures are also pointing to a weaker open. Yields on 10y USTs are down -2.6bps to 0.856%. Elsewhere, Bitcoin is up +1.29% this morning after being down -9.67% yesterday, the largest one day move lower since May 10, 2020. In terms of overnight data, China’s October industrial profits came in at +28.2% yoy (vs. +10.1% yoy last month). It is worth noting that the series is fairly volatile.

Even with a vaccine likely ahead, the continued high number of cases has been a cause for concern, not least with Thanksgiving/Christmas holidays occurring in which people are expected to mix increasingly anyway. Here in the UK, the government confirmed which regional restrictions would apply to different areas in England when the current lockdown ends, with the country grouped into three different tiers of restrictions. London evaded the toughest tier 3 measures, which include the closure of hospitality, and ended up in tier 2, though even then households are still banned from mixing with one another indoors. Large parts of England were placed in tier 3 however, including the other major cities of Birmingham, Manchester, Leeds and Bristol. And even in the lightest tier 1 restrictions, people are still unable to gather in groups larger than 6.

Elsewhere, New York reported that the number of Covid-19 hospitalisations had risen above 3,000, though in better news, Italy reported that the number of Covid-19 ICU patients fell for the first time in 7 weeks, and the 7-day average of cases in the UK fell to 17,329, which was its lowest in nearly 6 weeks. However, in Germany the number of ICU patients rose to record levels and Chancellor Merkel urged the country’s residents to do more to rein in the pandemic. We also saw a poll yesterday in Sweden that showed 82% of Swedes are either “somewhat” or “very worried” as to whether their health-care system can meet the challenge facing it thereby indicating that the country’s residents might be losing confidence in the nation’s less severe strategy to fight the pandemic. Sweden reported 5,841 new cases in the past 24 hours and now is the second most impacted country in our table below on the measure of 7-day rolling cases per 10k of population. Meanwhile in Asia, South Korea said that the country will decide soon on whether to further tighten social restrictions after the country reported another 569 cases after reporting 583 infections a day prior.

In other news, the ECB’s minutes from their late October meeting showed that there was growing concern about the outlook. The account said that views were exchanged on “whether revisions in the upcoming December Eurosystem staff projections were likely to result in the baseline being closer to the severe scenario included in the September projections.” Furthermore, it said “members widely agreed that … it would be warranted to recalibrate the monetary policy instruments in December”, so clearly setting the stage for some form of easing at the next meeting on December 10.

With the ECB pointing to yet more stimulus ahead, European sovereign bonds rallied further yesterday, and yields on Italian 10yr debt fell -1.3bps to a fresh all-time low of 0.60%, which just demonstrates the power that the ECB’s asset purchases have had in suppressing sovereign risk over recent months. Portugal was another country that saw yields at all-time lows yesterday, with their 10yr yields closing just clear of negative territory at 0.003%. The move was pretty uniform across the continent however, and yields on 10yr bunds (-2.0bps) and OATs (-1.8bps) also fell back.

Staying on Europe, the latest on the EU budget saw the Hungarian and Polish Prime Ministers refuse to back down on the dispute over the rule of law, where the EU is seeking to make budget funding conditional on countries obeying certain rule of law commitments. This is a problem for the EU since the long-term budget and the recovery fund need unanimous support from the 27 EU member states, so a compromise will need to be forged for this to go through, since others are strongly in favour of the provisions.

Meanwhile on Brexit, it was reported by RTE’s Europe editor that the EU’s chief negotiator Michel Barnier has called an “urgent” meeting of fisheries ministers for today. Arguably this is a positive development since fishing is one of the biggest sticking points in the talks, with the UK wanting to take back control of its coastal waters at the end of the year, while the EU want guarantees that their fishing industries will still have access to UK waters as they do at the moment. Face to face negotiations are set to restart this weekend according to Bloomberg after a period of isolation for Barnier. He had said earlier in the week there was little point in him coming if the U.K. wasn’t prepared to give ground so if talks do re-start tomorrow that will be encouraging. However Bloomberg is also reporting that Barnier will today update diplomats from the bloc’s 27 governments and will warn that discussions about the competitive playing field are still bogged down. So expect some headlines ahead of the EU negotiators’ trip.

To the day ahead now, and data releases include the French preliminary CPI reading for November, along with the Euro Area’s final consumer confidence reading for November. Central bank speakers include the ECB’s Panetta and Schnabel.

https://ift.tt/36ca4iX

from ZeroHedge News https://ift.tt/36ca4iX

via IFTTT

0 comments

Post a Comment