Earnings Kick Off With Markets Priced-For-Perfection

Authored by Lance Roberts via RealInvestmentAdvice.com,

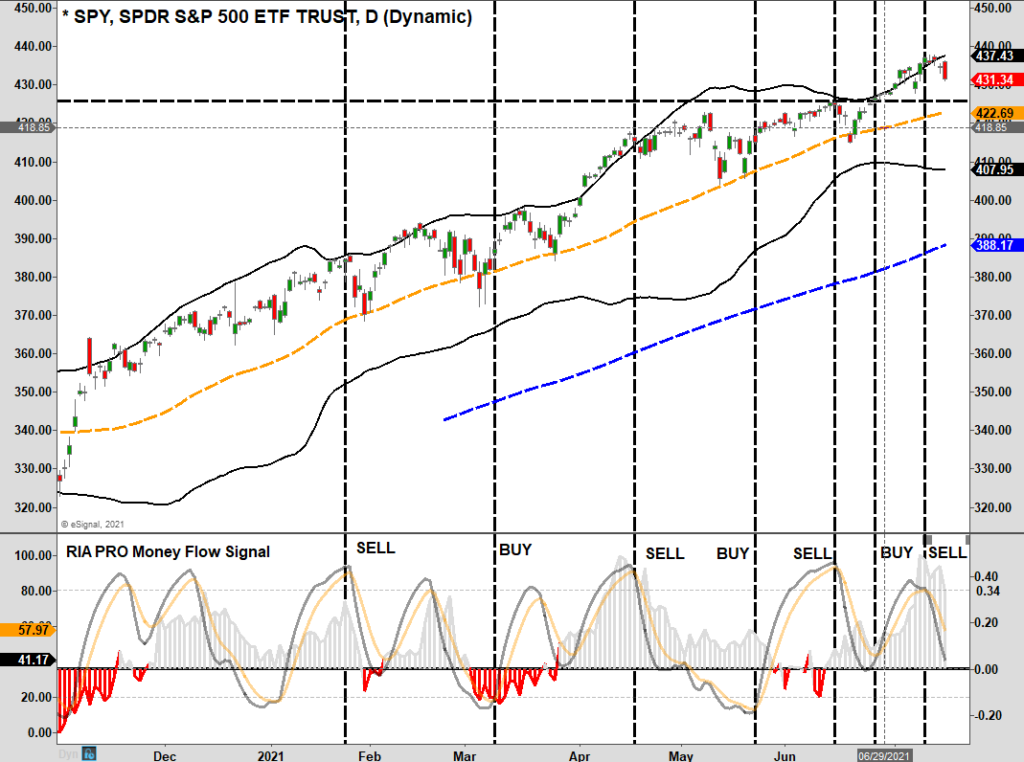

Market Pulls Back As Signals Turn

Last week, we discussed the market hit new highs with the index getting back to more extended and overbought conditions. To wit:

“While market volatility did pick up this past week, the index held its breakout support levels and closed at a new high. Such keeps the bullish bias intact. However, as shown, the money flow signals are now back to more elevated levels, which will provide resistance to higher prices short term.

“The bulls are indeed in charge of the markets currently, but the clock is ticking.”

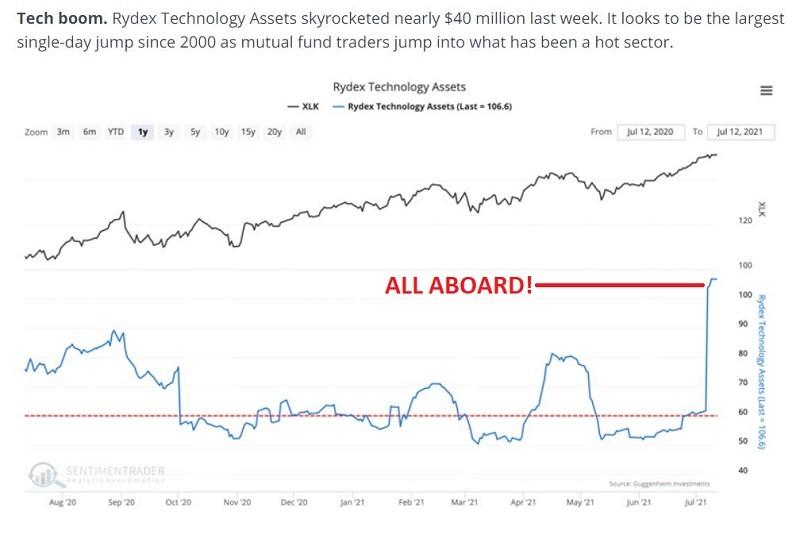

Not surprisingly, the market stumbled this past week as technology began to fade its recent outperformance. But, of course, investors have been piling into the trade as of late, pushing it to more overbought extremes. As noted by Sentiment Trader on Friday:

Of course, not surprisingly, investors are historically prone to “buying the most at the top.” With the seasonally weak trend of the Nasdaq approaching, with MACD’s triggering sell signals, there is likely to be some disappointment.

However, there are two reasons why investors are piling back into the 10-largest technology names:

-

Portfolio managers need to be invested to generate performance, and the mega-cap Technology names are easy to “hide” in given the large daily trading volumes.

-

These companies can generate earnings growth in a slowing economic environment.

The problem with the second point is that those top-10 mega-cap names generate the bulk of the earnings of the entire S&P 500 index. Such has only occurred at previous bull market peaks.

All of this suggests the risk of a correction remains elevated, particularly with the market priced for perfection.

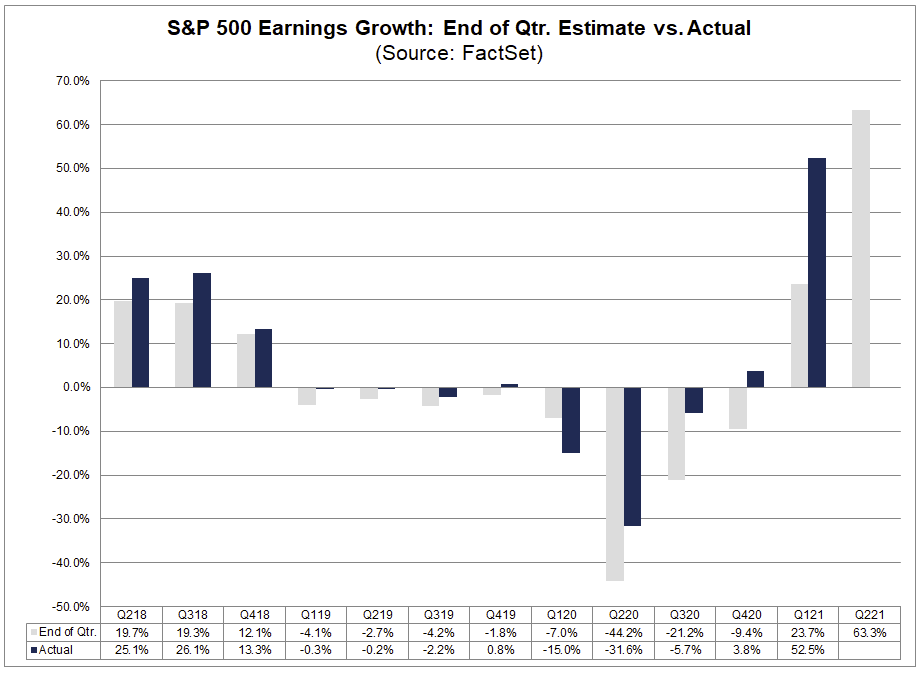

Earnings Season Has A High Bar

Over the last few months, the rush of analysts to upgrade earnings estimates for the S&P 500 is one for the record books. According to Factset:

“If the S&P 500 reports year-over-year growth in earnings of 69.3% in Q2, it would mark the highest (year-over-year) earnings growth rate reported by the index since Q4 2009 (109.1%).”

Of course, given the expectation of robust earnings growth for Q2, analysts still predict a double-digit price increase for the S&P 500. To wit:

“Industry analysts in aggregate predict the S&P 500 will see a price increase of 11.2% over the next 12 months. The bottom-up target price is calculated by aggregating the median target price estimates (based on company-level estimates submitted by industry analysts) for all companies in the index. On July 8, the bottom-up target price for the S&P 500 was 4803.62, which was 11.2% above the closing price of 4320.82.” – FactSet

(Of course, it is worth noting the S&P NEVER matches its bottom-up price target. In other words, estimates are always too high compared to reality.)

Analysts have set a very high bar for the markets to hurdle, given already lofty valuations. With indices already well-stretched above their historical means, there is much room for disappointment.

With the currently very overbought short-term market, a 3% to 10% correction this summer remains likely.

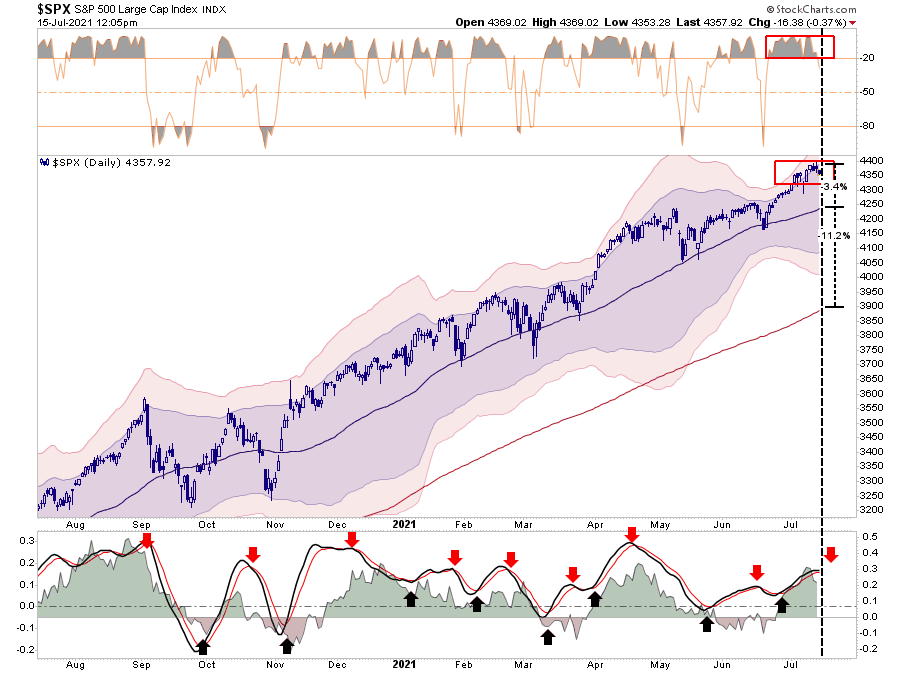

Markets Priced For Perfection

While earnings estimates are soaring on exuberant hopes of an indefinite economic boom, revenue may be telling a much different story. I noted this point earlier this week:

Thought this was interesting.#Earnings are expected to hit $151 #reported this quarter

— Lance Roberts (@LanceRoberts) July 13, 2021

Q4-2020 = 94.13

Q1-2021 = 128.20

Q2-2021 = 151.17 est.

But here is revenue

Q4-2020 = 367.48

Q1-2021 = 364.05

Q2-2021 = 360.81

Anyone notice an issue relating to #Price/Sales

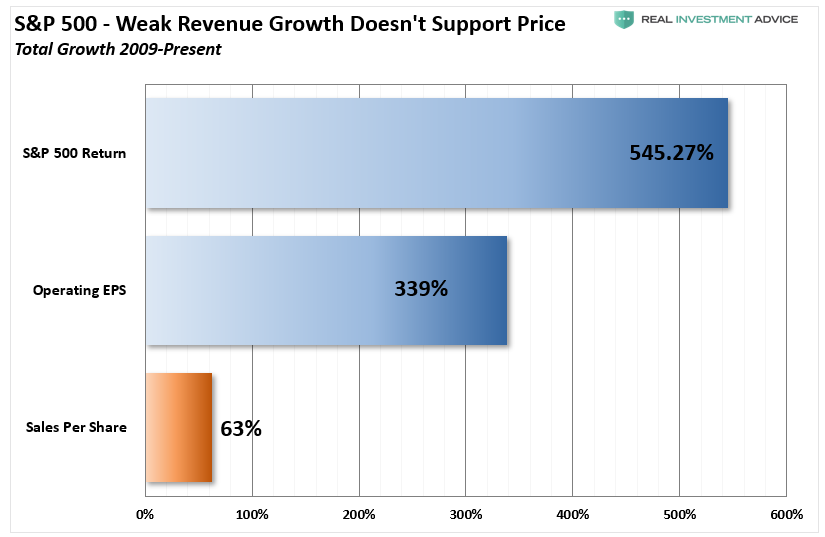

Investors should dismiss the above quickly. First, revenue is what happens at the top line. Secondly, revenue CAN NOT grow faster than the economy. Such is because revenue comes from consumers, and consumption makes up 70% of the GDP calculation. Earnings, however, are what happens at the bottom line and are subject to accounting gimmicks, wage suppression, buybacks, and other manipulations.

Since 2009, corporate operating earnings grew cumulatively by 339%. Yet, during that same period, the cumulative growth of revenue is only up 63%. It is through “accounting magic” that revenue gets multiplied to the bottom line. Out of each dollar of earnings, 82% is from accounting “management,” and just 18% is from revenue.

The majority of the rise in “profitability” came from various cost-cutting measures and accounting gimmicks rather than actual increases in top-line revenue. While tax cuts certainly provided the capital for a surge in buybacks, revenue growth, the result of a consumption-based economy, remains muted.

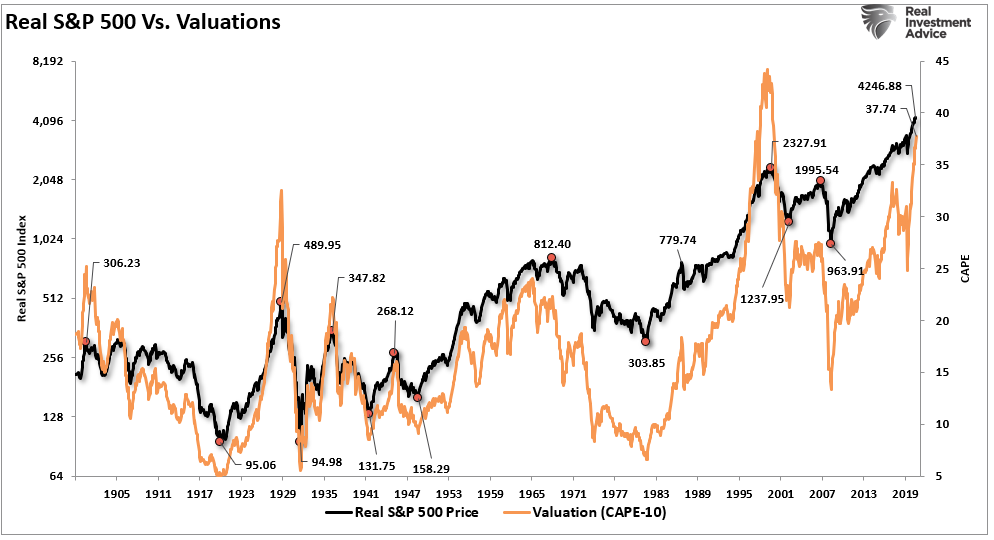

The Valuation Problem

The problem is the market surged higher due to the ongoing liquidity injections from the Federal Reserve. While liquidity drives asset prices higher, it does not foster economic activity, which creates corporate revenue. Currently, the price-to-sales (revenue) ratio is at the highest level ever. As shown, the historical correlation suggests outcomes for investors will not be kind.

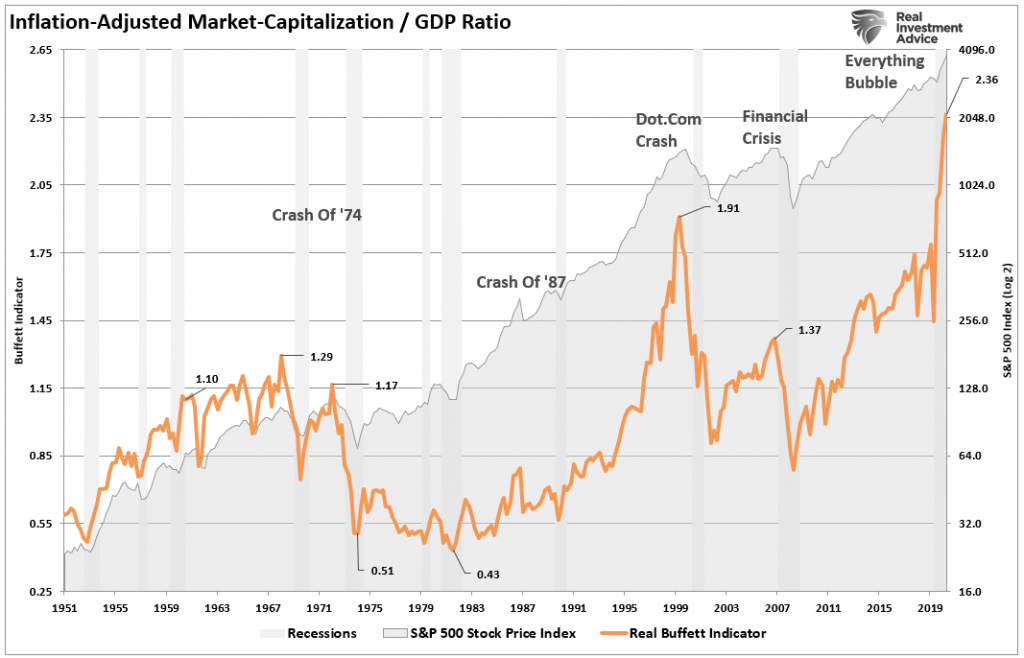

Of course, given that revenue can only grow roughly as fast as the economy, the market-capitalization to GDP ratio is very important. While the “price” of the market can outpace economic growth in the short term, it can’t do so indefinitely. Thus, at 2.4x economic growth, the market is highly overvalued relative to what the economy can generate in revenue growth.

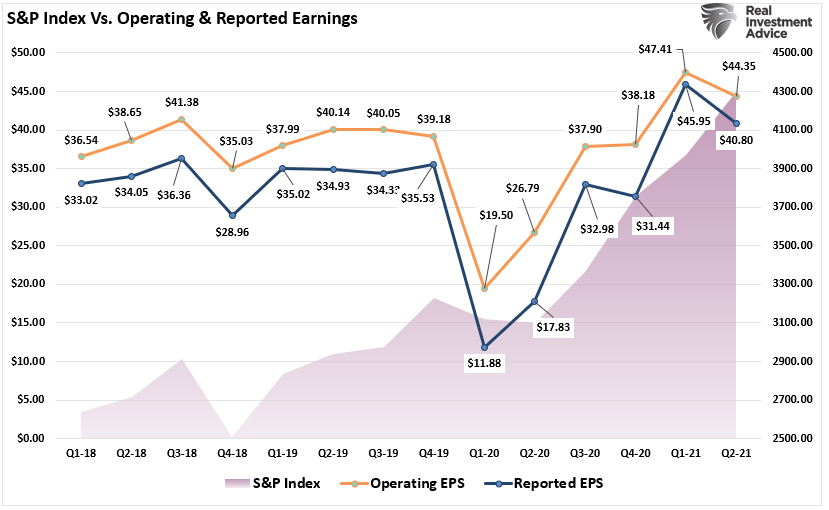

Lastly, with markets currently perched near all-time highs, both operating and reported earnings will fall in Q2 versus Q1 as economic growth peaks. (We have repeatedly warned of this issue.)

Note that as of Q2-2021, operating earnings (earnings without all the bad stuff) will only be 10% higher than they were in 2018. Yet, the market is currently trading 48% higher.

Even with the “sharpest recovery in earning in history,” the market continues to expand its valuation multiple. (Chart below uses current estimates for Q2-2021) So much for earnings catching up with the price.

As I said, investors have priced the market for perfection. Therefore, any disappointment could lead to poor outcomes for investors taking on excess risk.

https://ift.tt/36FMavA

from ZeroHedge News https://ift.tt/36FMavA

via IFTTT

0 comments

Post a Comment