Goldman Raises Year-End Oil Price Target To $90

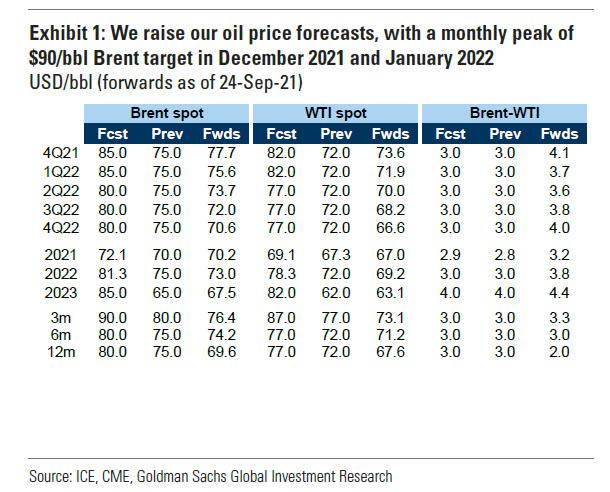

Just days after Goldman's head commodity analyst Jeff Currie told Bloomberg TV that the bank anticipates oil spiking to $90 if the winter is colder than usual, on Sunday afternoon Goldman went ahead and made that its base case and in a note from energy strategist Damien Courvalin, he writes that with Brent prices reaching new highs since October 2018, the bank now forecasts that this rally will continue, "with our year-end Brent forecast of $90/bbl vs. $80/bbl previously."

What tipped the scales is that while Goldman has long held a bullish oil view, "the current global oil supply-demand deficit is larger than we expected, with the recovery in global demand from the Delta impact even faster than our above consensus forecast and with global supply remaining short of our below consensus forecasts."

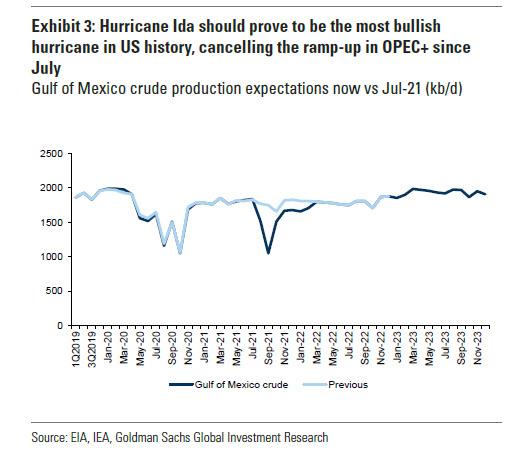

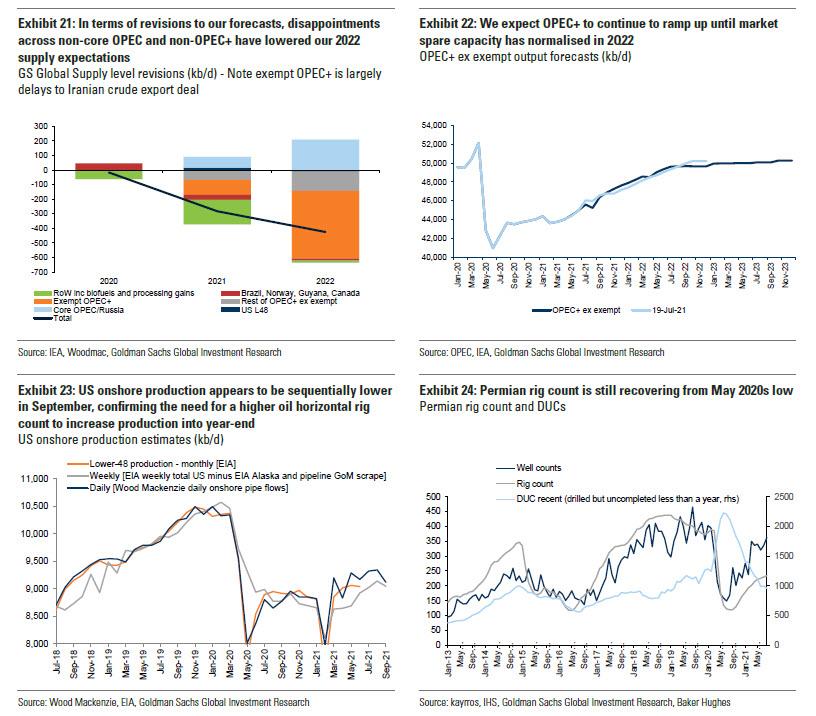

Among the supply factors cited by Goldman is hurricane Ida - the "most bullish hurricane in US history" - which more than offset the ramp-up in OPEC+ production since July with non-OPEC+ non-shale production continuing to disappoint.

Meanwhile, as noted above, on the demand side Goldman cited low hospitalization rates which are leading more countries to re-open, including to international travel in particularly COVID-averse countries in Asia.

Finally, from a seasonal standpoint, Courvalin sees winter demand risks as "further now squarely skewed to the upside" as the global gas shortage will increase oil fired power generation.

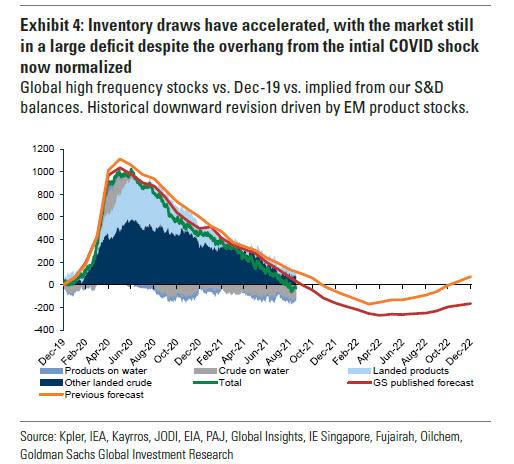

From a fundamental standpoint, the current c.4.5 mb/d observable inventory draws are the largest on record, including for global SPRs and oil on water, and follow the longest deficit on record, started in June 2020.

For the oil bears, Goldman does not see this deficit as reversing in coming months as its scale will overwhelm both the willingness and ability for OPEC+ to ramp up, with the shale supply response just starting.

This sets the stage for inventories to fall to their lowest level since 2013 by year-end (after adjusting for pipeline fill), supporting further backwardation in the oil forward curve where positioning remains low.

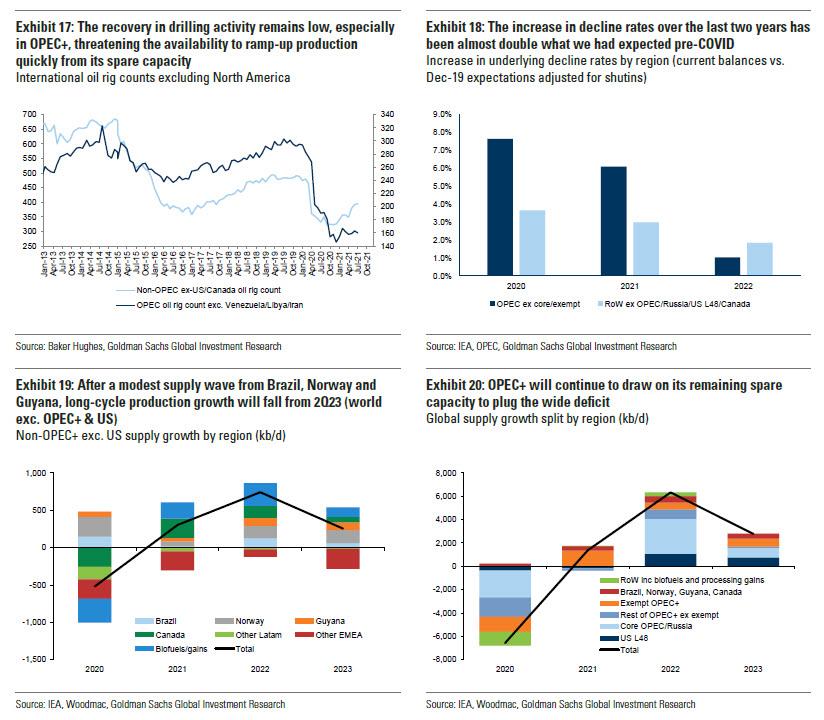

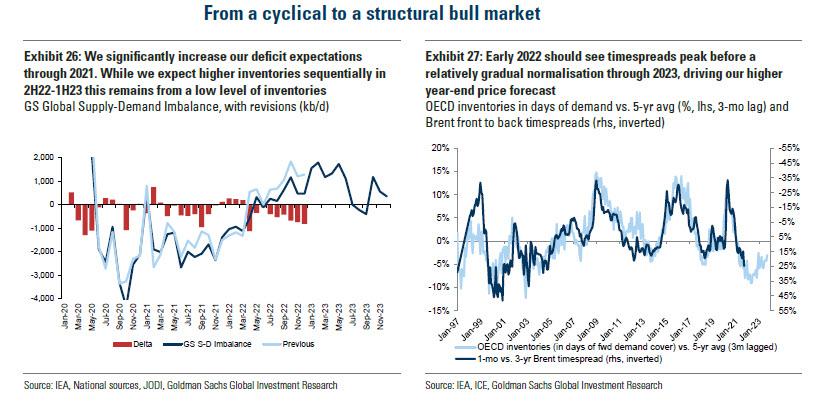

But what about a production response? While Goldman does expect short-cycle production to respond by 2022 at the bank's higher price forecast, from core-OPEC, Russia and shale, this according to Goldman, will only lay bare the structural nature of the oil market repricing. To be sure, there will likely be a time to be tactically bearish in 2022, especially if a US-Iran deal is eventually reached. The bank's base-case assumption is for such an agreement to be reached in April, leading the bank to then trim its price target to an $80/bbl price forecast in 2Q22-4Q22 (vs. its 4Q21-1Q22 $85/bbl quarterly average forecast). This would, however, remain a tactical call and a likely timespread trade according to Courvalin, with long-dated oil prices poised to reset higher from current levels, especially as the hedging momentum shifts from US producer selling to airline buying (a move which Goldman says to position for with a long Dec-22 Brent and short Dec-22 Brent put trade recommendations).

Meanwhile, the lack of long-cycle capex response - here you can thank the green crazy sweeping the world - the quickly diminishing OPEC spare capacity (Goldman expects normalization by early 2022), the inability for shale producers to sustain production growth (given their low reinvestment rate targets) and oil service and carbon cost inflation will all instead point to the need for sustainably higher long-dated oil prices. Remarkably, Goldman now expects the market to return to a structural deficit by 2H23, which leads it to raise its 2023 oil price forecast from $65/bbl to $85/bbl, and the mid-cycle valuation oil price used by Goldman's equity analysts to $70/bbl.

Translation: expect a slew of price hikes on energy stocks in the coming days from Goldman.

Finally, where could Goldman's forecast - which would infuriate the white house as gasoline prices are about to explode higher - be wrong? For what it's worth, the bank sees the greatest risk on the timeline of its bullish view. On the demand side, it would take a potentially new variant that renders vaccine ineffective. Beyond that, however, the bank expects limited downside risk from China, with its economists not expecting a hard landing and with our demand growth forecast driven by DMs and other EMs instead. This leaves near-term risks having to come from the supply side, most notably OPEC+, which next meets on October 4. And while an aggressively faster ramp-up in production by year-end would soften (but not derail) our projected deficit, it would only further delay the shale rebound, which would reinforce the structural nature of the next rally given binding under-investment in oil services by 2023. In addition, a large ramp-up in OPEC+ production would simply fast-forward the decline in global spare capacity to historically low levels, replacing a cyclical tight market with a structural one.

The full report as usual available to pro subscribers in the usual place.

https://ift.tt/3EOtfi1

from ZeroHedge News https://ift.tt/3EOtfi1

via IFTTT

0 comments

Post a Comment