One Bank Spots A Bizarre Market Divergence: Stocks Are At All Time Highs Yet Investors Are Bracing For Crisis

Something strange is going on.

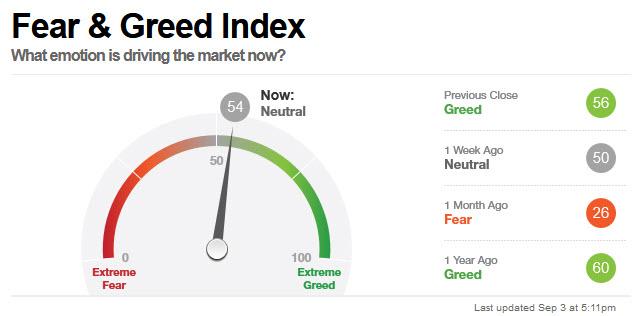

On one hand stocks are trading at all-time highs, levitating every day without an apparent care in the world, with traders seemingly complacent that any air pocket in the market will simply mean more accommodation by the Fed which may not taper and which, according to some, may even to more QE. On the other, traditional bear-market signals such as the CNN fear and greed indicator, are deep in neutral territory, having dipped in "fear" territory as recently as one month ago...

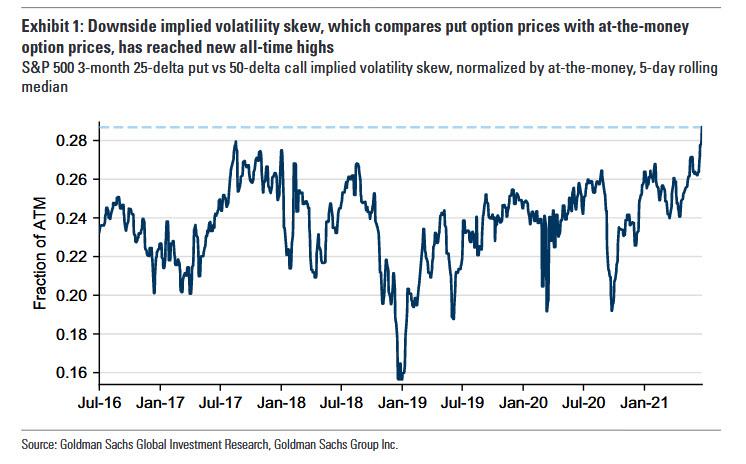

... while the SKEW index which many view as an indicator of crash preparation, is near all time highs, prompting a warning from none other than Goldman Sachs.

Picking up on this apparent schism in the market, last observed just last August when a marketwide gamma-squeeze orchestrated by SoftBank spooked traders who were fearful that the economy was nowhere near enough to support the market's epic ramp, SocGen strategist Arthur Van Slooten and Alain Bokobza ask if what we are seeing is a "qarning signal or excessive caution?"

As the SocGen duo puts it, the bank's Multi Asset Risk Indicator (SG MARI) is currently hovering just above deep risk off territory despite ever rising markets, which raises several questions:

- Are investors really deeply risk off?

- How unusual is the latest low?

- How did we get here?

- Was it equities, bonds, FX or commodities that triggered the dip?

- Most importantly, what’s the ‘message’ – a warning signal of major trouble ahead (= Sell) or are investors being overly cautious (= Buy)?

The SocGen strategists then cover each point one by one:

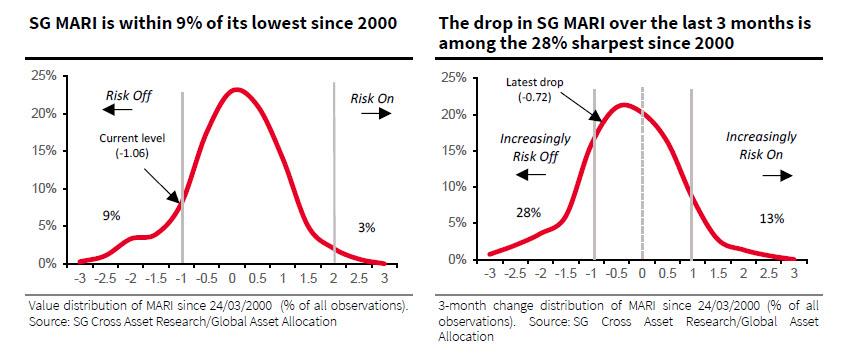

Risk on or Risk off? With the S&P 500 up +20.4% year to date and Euro Stoxx 50 at +19.2%, investors appear to be bristling with confidence, "perhaps even to the point of complacency" which was SocGen's first impression when its market strategist came back from vacation and took the pulse of the markets. But surprisingly, the bank's SG MARI tracker of investors’ risk positioning in futures and options is giving exactly the opposite signal, indicating that investors are remarkably risk off (see chart below). Just three days before Jay Powell’s ‘tapering’ speech at Jackson Hole, SG MARI touched the lower bound of its normal trading range at -1.06, almost one standard deviation below its long-term average.

How unusual is the latest SG MARI reading? Very. SocGen has only seen such a low reading in just 9% of all observations since 2000. In the past, any drop below the current SG MARI level has been typically trigged by a major crisis such as the TMT bubble, the subprime crisis and the ‘taper tantrum’. The current level is below even the Covid-19 blighted March 2020 reading! Conversely, whenever SG MARI has bounced back from current levels, it has typically heralded the start of a more positive tone, which is good for risky assets such as equity and commodities but not for rates.

How did the shift into risk off mode transpire? Since the COVID-19-induced lows at end March 2020 (-0.85, after a sell-off that lasted only 14 weeks), quick policy initiatives sent SG MARI higher, peaking at 0.56 on 15 January 2021. Since then, the indicator has gradually moved deeper into risk off territory, with the drop moderately accelerating in the last three months. The two charts below indicate that the current low (LH chart below) is far more unusual than the latest drop (RH chart).

Did any asset class in particular move the dial? No. SG MARI’s current low is the result of relatively weak readings from each of its four components – the weighted average of indicators for equities, bonds, FX and commodities – without a single metric standing out. Arguably, this is exactly what a good aggregate indicator should do: highlight a trend that is not immediately obvious from simple observation of its underlying variables.

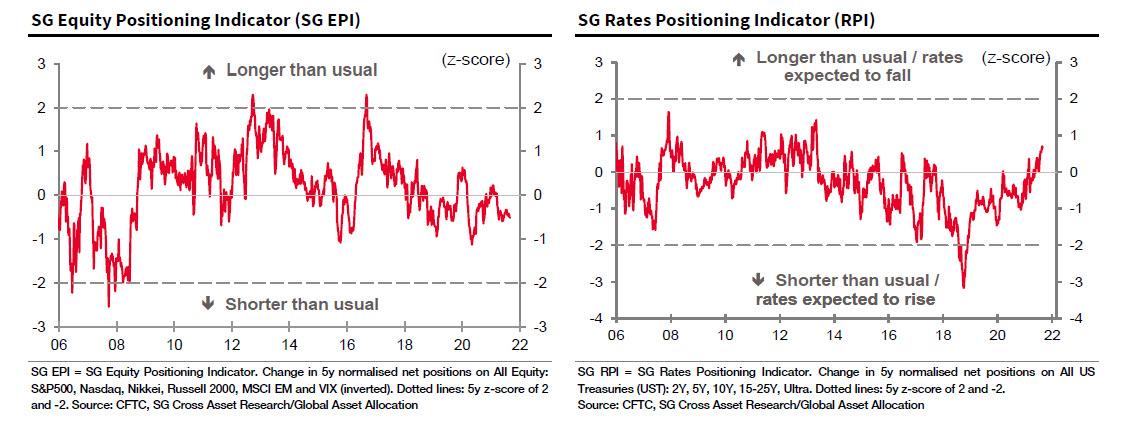

Cautious signals from equities and bonds. For SG MARI, net shorts from the bank's equity positioning indicator (SG EPI) come into the equation directly but net longs from the rates positioning indicator (SG RPI) are inverted first. Hence, the latest rise in SG RPI contributes to SG MARI’s low reading – which makes sense as SG RPI signals increasingly strong expectations of a further fall in rates, implying a bearish outlook for growth that would justify investors taking a risk-off stance.

Also cautious FX and Commodities positioning. The latest drops in SocGen's Foreign Exchange Positioning (SG FXPI) and Commodity Positioning (SG COPI) indicators have fed directly through to the SG MARI multi asset risk indicator, albeit with lower weightings than for equities and bonds. The drop in SG FXPI indicates generally shorter positions in cyclical currencies versus USD. In the case of the Australian dollar (AUD), this is largely explained by the drop in copper prices related to the slowdown in China’s economic growth. But as copper is not formally part of the bank's commodity indicator, the latest drop in SG COPI is 100% due to the equilibrium between crude oil and gold.

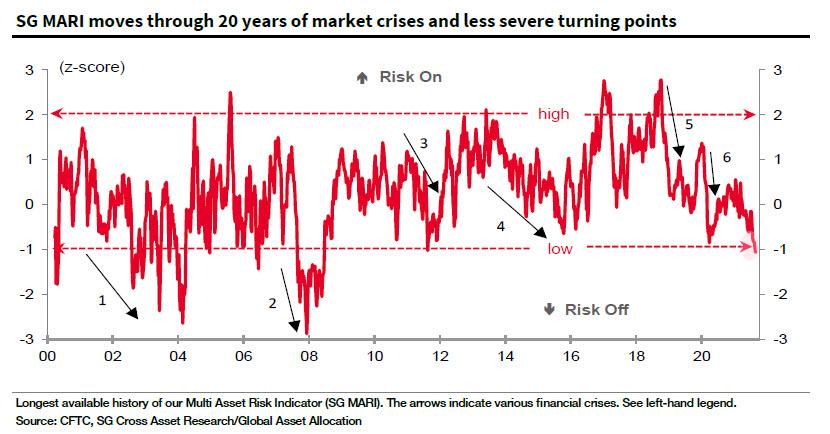

Does a low SG MARI reading spell major trouble ahead? According to SocGen, "the jury is still out." The chart below shows the longest available history of SG MARI, with arrows indicating periods of major financial crisis. An important observation is that crisis can arise regardless of the level of SG MARI just before they are triggered. In all cases, SG MARI then corrects strongly, with the length of correction indicating the severity of the crisis at hand. By extension, the current low level does not necessarily spell major trouble ahead... but it very well could.

Alternatively, are "spooked" investors sending a clear Buy signal? No. Here SocGen tries to preempt any accusations (ostensibly from its clients) that it is starting a market panic, noting that as illustrated by the chart above, whenever SG MARI’s shifts -1 standard deviation below its normal trading range – a point it has just crossed – it signals the start of a decent bounce higher, and the bank asks "Barring major trouble ahead, is there any reason why this is not the case now? If so, the latest drop in SG MARI could be interpreted as a Buy signal." Well sure... but the problem is that usually by the time its risk index is at -1, markets are tumbling. Only this time they are at all time highs. So extrapolating the past to the present situation seems naive at best and manipulative at worst.

Spin aside, SocGen is correct that after many months of exceptional market performance, we are now on the brink of an important shift, however gradual it may turn out to be in practice. The bank thinks that the pace of policy change that includes monetary and fiscal adjustments could be largely dependent on how fast COVID restrictions can be lifted, including in emerging markets. Meanwhile, peak growth has already been reached, first in China, where less restrictive policy may even be needed later this year.

In short, the French bank summarizes that "as markets transition from ‘goldilocks’ territory and heady valuation levels to a more testing environment with the prospect of decelerating earnings and rising bond yields, this is hardly the appropriate time to conclude that SG MARI is giving an outright Buy signal. Indeed, the relief over the announced gradual nature of Fed tapering and the decoupling with rate hikes thereafter may prove short-lived." And that's the non-spun version of reality.

https://ift.tt/3yNzXAx

from ZeroHedge News https://ift.tt/3yNzXAx

via IFTTT

0 comments

Post a Comment