A Detailed Look At Who Is Buying Bitcoin Here

The past two weeks saw some of the strongest crypto returns this year, with the broader crypto index rallying around 25%. The move started when bitcoin (BTC) rocketed 15% in a two-hour window during early Asia time on Monday 26 July.

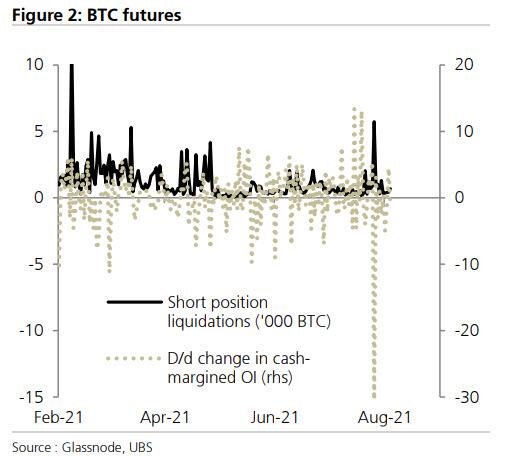

As we noted at the time, a break of the $35,000 level triggered stops on short positions, undermining record-high cash-margined futures open interest.

While many stories tried to tie the move to Amazon.com's posting of a job advert for a lead crypto analyst, this was not the catalyst as the news had first hid two days earlier, and the company was quick to quash speculation that it suggested they would consider accepting BTC payments.

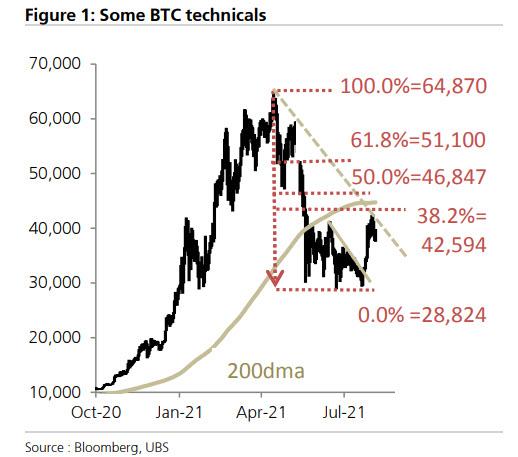

Echoing our take that the move was a squeeze and technical in nature, UBS strategist Alexey Ostapchuk writes in his weekly "Crypto Compass" note that "underlining its technical nature, price momentum ran out of steam right at the 38.2% Fibonacci retracement point, extending a clear downtrend from May which now becomes immediate resistance around 41k. Above that the 200dma comes in around 45k, then the 50.0% and 61.8% Fibos near 47k and 51k, respectively."

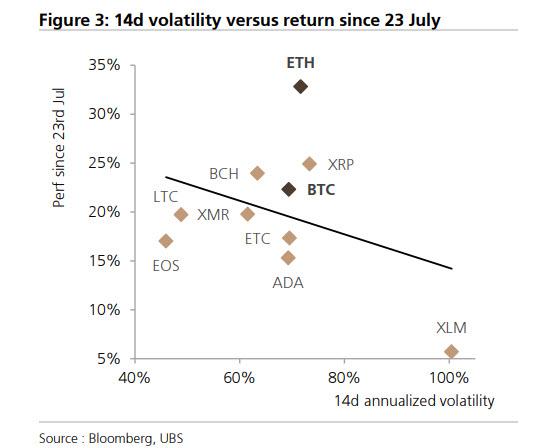

While the rest of the crypto space was dragged up in the buying frenzy, but Bitcoin Cash (BCH), Ether (ETH) and XRP proved to be subsequent standouts

Taking a modest tangent here, we look at a recent analysis by Copper.co of on-chain data which confirms UBS' observations and reflects that small to medium investors have returned to accumulation ever since Bitcoin hit the $35k mark at the end of May. The fact that the cryptocurrency dropped further to $30k was, by on-chain metric standards, seen as a cost-averaging opportunity. Simply said, retail buyers accumulated more.

Digging deeper, Copper founds that since the start of this year, on-chain data shows that entity holding between 0 and 1 BTC increased by 137k Bitcoins, equivalent to 72% of newly mined supply. Meanwhile, miner balances have actually increased since the start of the year, meaning, not all mined Bitcoins have come to market.

While it may seem that we’re speaking about small amounts of Bitcoin, context is important. These small amounts of accumulated Bitcoin are more than triple Tesla’s now infamous purchase. These investors have also accumulated more than MicroStrategies ballooned treasury of 105k Bitcoins. There is a key point to further consider. The demand by these investors has been and remains very consistent.

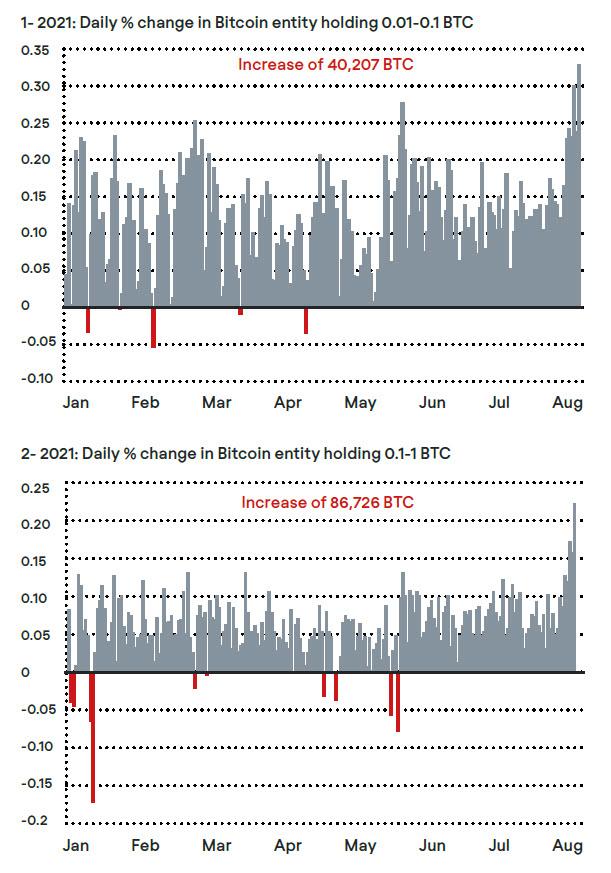

In 2021 alone, entity holding between 0.01 and 0.1 BTC increased by over 40k Bitcoins. Between 0.1 and 1 BTC entity holdings saw a huge 86k increase. But more interesting is the fact that it was only on a few days of the year did these entity holdings decrease.

This category of investors is seemingly price agnostic. Since the end of 2013 when Bitcoin hit over $1000 for the first time, these entity holdings never saw a month in decline. Since 2018, when Bitcoin met its top before declining from near $20k to $3k, entity holdings have grown by nearly 500k. Every month saw growth.

So linear is the growth of smaller investors that Copper did some simple extrapolation on how retail might chip away at the supply, Satoshi-by Satoshi.

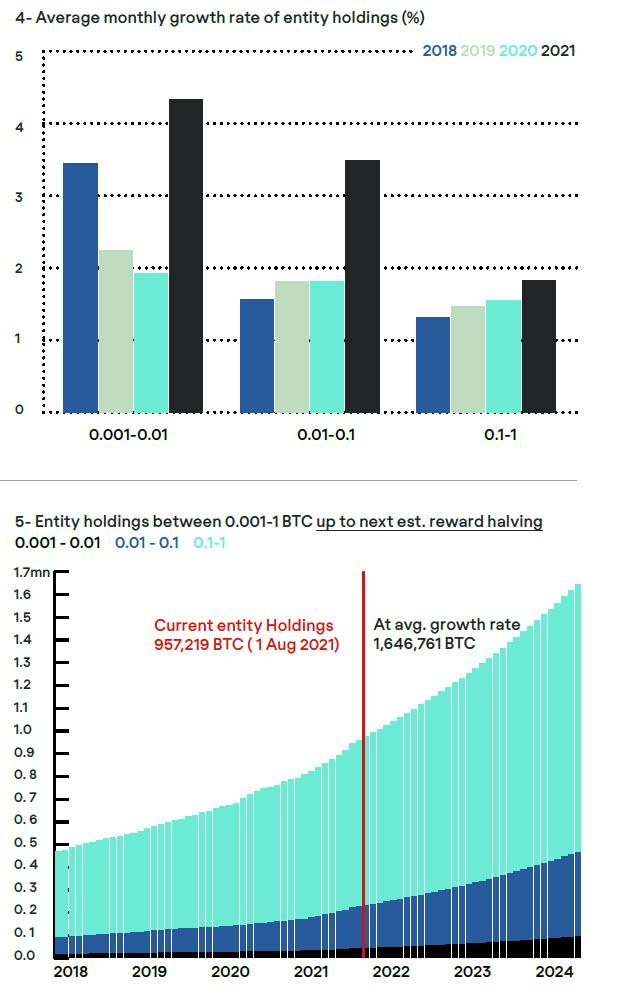

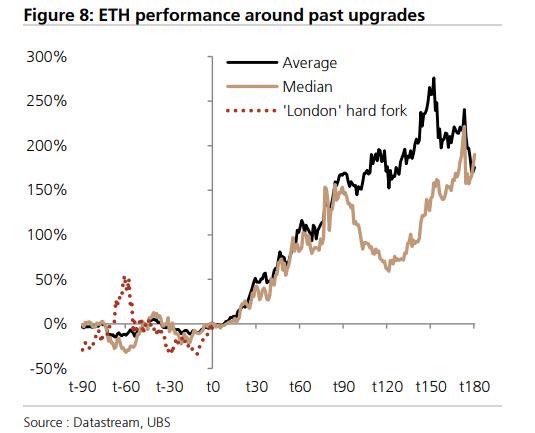

What if found is that average monthly growth rates for entity holdings have been fairly close year-on-year (see chart 4). And considering the consistent level of growth since 2018, Copper assessed the market supply should these levels continue and long-term investors remain price agnostic. After all, a near $65k BTC didn’t scare them off. Should growth continue at this pace up until Bitcoin reaches its next miner reward halving, entity holdings could grow to nearly 1.7mn BTC from just under 1mn today. This would account for nearly 75% of new mined Bitcoin (see chart 5).

Of course, there will come a time when price will matter. But to date, this can’t actually be seen by smaller investors. Growth has been particularly steady. And these entity holdings have increased more in the first seven months of 2021 than in all of 2020 already - at sky high prices (see chart 6).

This doesn’t account for institutional buyers. And what also needs to be considered despite not having actual figures, is that there is Bitcoin sitting on exchanges that also represents retail investors are accumulating.

The bottom line:

Small investors can make a big difference. Are these investors potentially new entrants attempting to gain a small slice of Bitcoin? Or perhaps traders rotating profits into Bitcoin? Listening in on the crypto community can seem particularly obnoxious to proponents of the traditional investor class. Every dip is an opportunity no matter the losses. Hold on to bitcoin for life. The institutions are coming. But what’s scarier is that so far, despite grandiose claims, they’ve been fairly accurate. One thing that time will test is the concept of “Stacking Sats”. Maybe they know something. So far, the data supports it.

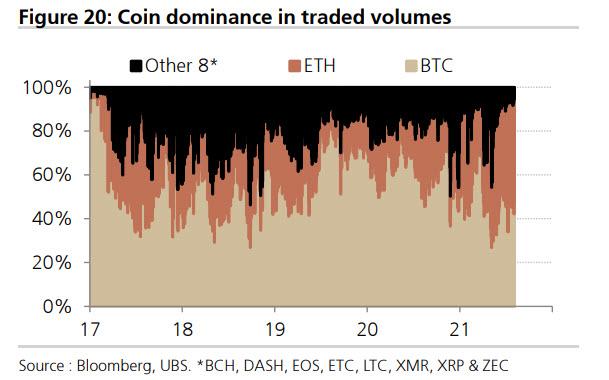

To be sure, some of these moves can be traced to idiosyncratic developments: the launch of SmartBCH sidechain, Ethereum's widely anticipated and just completed 'London' hard fork, and Ripple's On-Demand Liquidity service. Notably, ETH is following the pattern it mapped around its seven previous upgrades quite closely.

It is also worth noting that with Ethereum volumes now surpassing those of bitcoin...

... it may be just a matter of time before ETH becomes the biggest cryptocurrency and has a lower volatility than its historically larger peer...

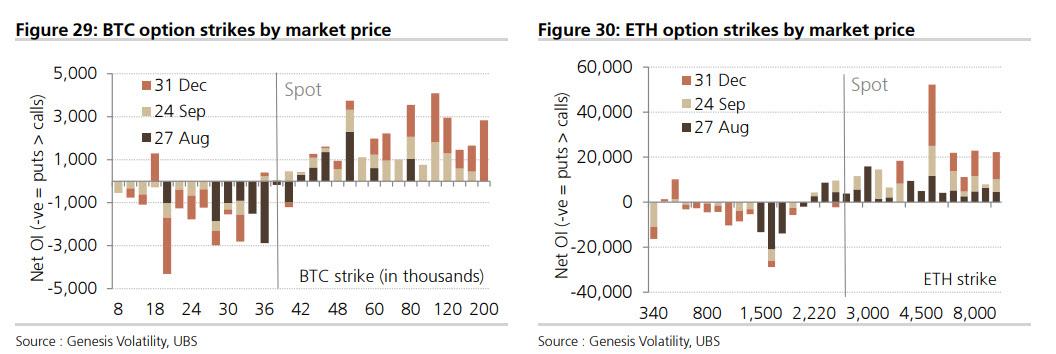

... especially if ETH is subject to a major gamma squeeze: as shown below, the bulk of long-dated ETH option strikes are in the 5000 and higher range, while most short-dated bitcoin option straks are below the current spot price.

Still, as Ostapchuk notes, "it's worth recognizing that these are all bigger market-cap coins which tend to be less volatile so would normally be laggards in any bull market.That this is instead an environment where market interest is unusually concentrated probably speaks of the hangover that is still affecting retail interest. It may also say something about attention focusing on better prospects for institutional adoption in the face of greater legal clarity."

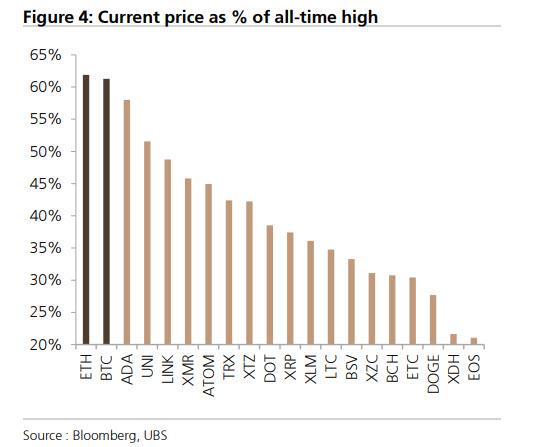

As the UBS strategist goes on, headline comparisons and on-chain metrics further illustrate some of these dynamics. Compared with BTC and ETH, most altcoins remain substantially further from their recent all-time highs.

Which brings us to arguably the key question: who's buying?

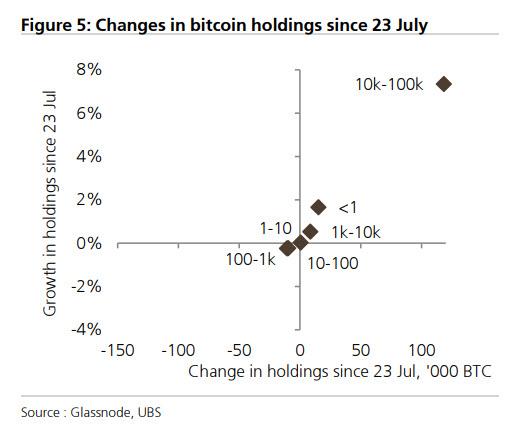

According to Ostapchuk, the main bitcoin buyers continue to be medium-size whales, holders of 10k-100k coins, generally at the expense of bigger entities. Remarkably, the smallest cohort of users that own less than 1 BTC saw the next-largest increase in holdings having absorbed 131% of new bitcoins minted over the last fortnight.

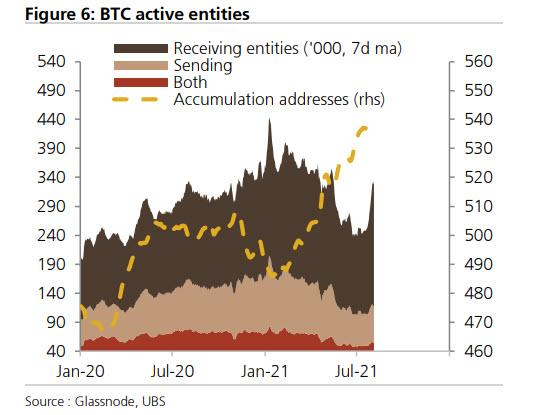

Furthermore, the recovery in on-chain activity was primarily driven by receiving entities and accumulation addresses, with the former count now back at January levels and the latter reaching a new peak. Meanwhile, exchange balances and the number of pure senders remain low amid sub-par transaction volumes.

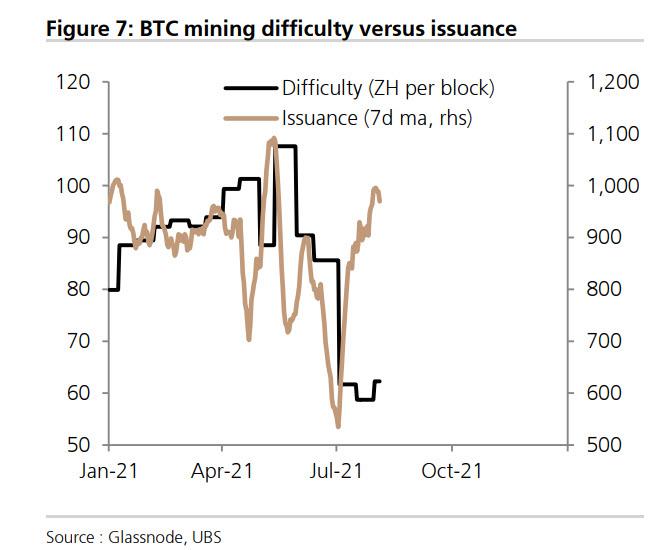

Separately, as noted recently, mining difficulty has rebounded with prices but remains well below its pre-China crackdown levels, lifting BTC issuance back to mid-May rates of growth.

As Ostapchuk summarizes, "such things generally accord with our composite measures that show trendiness scores below normal and no major coin prices screening as particularly stretched."

* * *

Away from market dynamics and looking at the news front, UBS points to a few holdouts like ShapeShift are going to extreme lengths to remain outside the regulatory fold. But most service providers are scrambling to become more compliant. Thus, Binance and FTX cut permitted maximum trading leverage on their platforms from 100 times or more to 'just' 20 so as to deflect attention and enhance consumer protection. Both face increased scrutiny over the 'open secret' that they have thus far done little to prevent US consumers from trading through their unregulated offshore entities. This was one of the points which Gary Gensler emphasized in a speech at the Aspen Security Forum on Tuesday. He also said that securing compliance from trading, lending and DeFi platforms should be a legislative priority, and that the Howey Test remained sufficient and suggested many digital assets are indeed securities so require registration. On a more accommodating note, he said he was looking forward to receiving SEC staff reviews of crypto ETF applications, especially those linked to BTC futures.

BlockFi also received a cease and desist order for new account openings in the first such clampdown on a platform that pays users a substantial (4-8% annualized) yield for staking cryptocurrencies that are then used to provide dollar loans. The New Jersey Attorney General alleges that these represent unregistered securities, and other states like Alabama and Texas have since followed suit. Such action is already reverberating across the sector. Another well-known industry name, Uniswap, delisted around 100 offerings on its trading interface, including tokenized stocks, options and indices.

The long-running Department of Justice investigation into Tether ratcheted up a notch just after the Fed and Treasury signalled their heightened focus on stablecoins. Bloomberg reported that executives there may have committed bank fraud by hiding the fact that their early business dealings were linked to crypto. Paxos also turned on its larger rivals in a scathing blog post. Fully 96% of its reserves are held in FDIC-insured cash deposits along with a further 4% in US Treasury bills; the equivalents for USDT and USDC are 4%+3% and 61%, respectively, with much of the remainder being unsecured commercial paper, secured loans, corporate bonds and some longer-dated Treasuries.

We got two surprises out of Washington. One was wrapped up in the much anticipated bipartisan infrastructure bill, which now incorporates enhanced supervision of digital asset transactions via the IRS to fund around USD28bn of the USD550bn in new outlays. Lobbying efforts by the Bitcoin Association and others succeeded in tightening the definition of 'brokers' in the final draft, though the USD10,000 threshold on transaction reporting stands. Some further changes are inevitable as it works its way through the Senate and the requirements won't go into effect until 2023. But this clearly marks a ratcheting up of the pressure on VASPs, who have hitherto been enjoying an unfair advantage over their legacy financial sector peers. The other twist came from Don Beyer (D-VA), chairman of Congress' Joint Economic Committee. He introduced a bill 'seemingly out of fresh air' that seeks to establish comprehensive oversight of crypto industry. Observers describe it as remarkably well researched and the most impressive piece of such legislation to date, making it too worth watching even if its immediate prospects for becoming law are less clear.

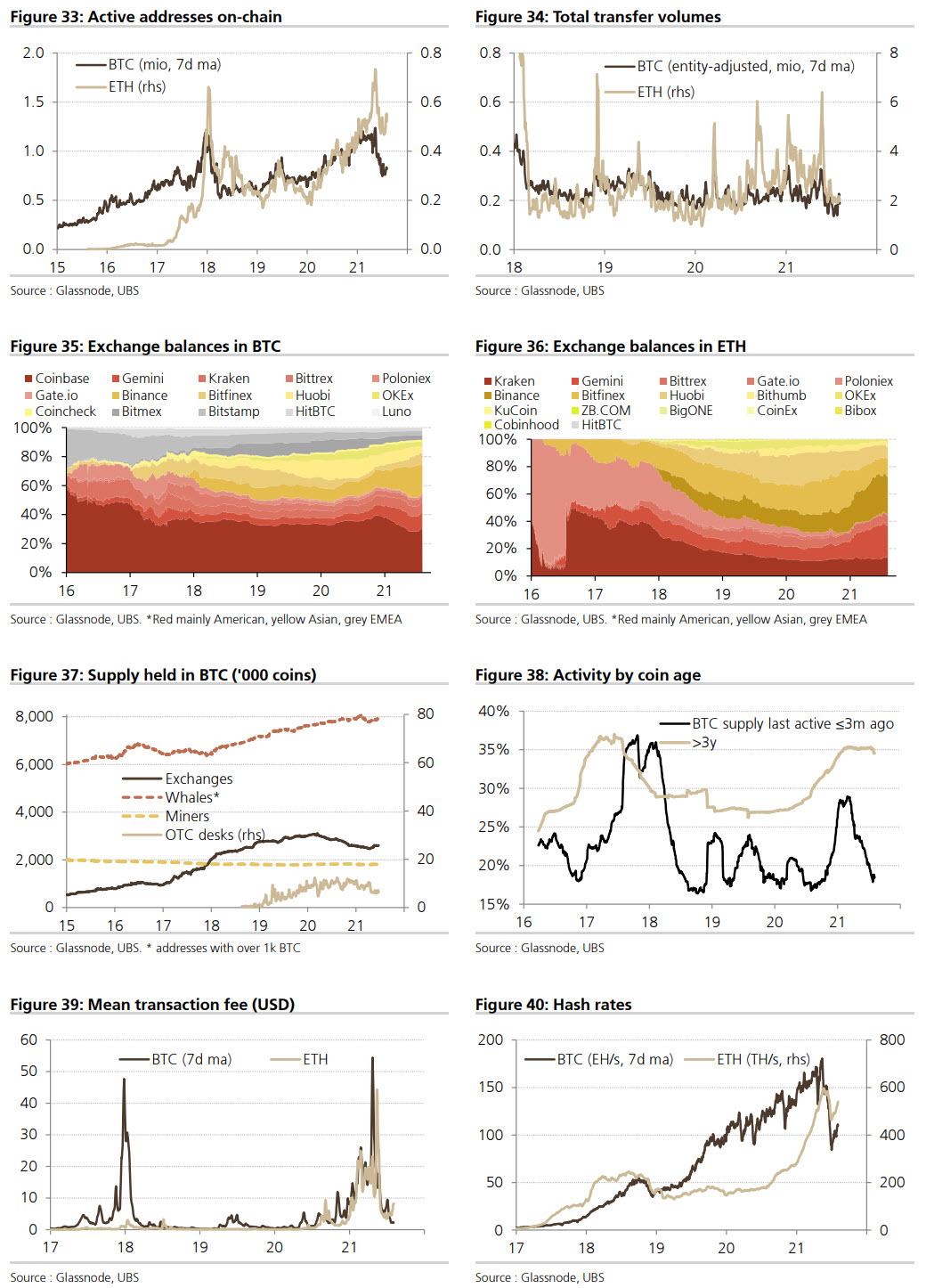

Finally, a handful of useful crypto charts courtesy of UBS:

https://ift.tt/2VAd1XX

from ZeroHedge News https://ift.tt/2VAd1XX

via IFTTT

0 comments

Post a Comment