US Surface Transportation Board Rejects CN-Kansas City Southern Voting Trust

By William Vantuono of Railway Age

The United States Surface Transportation Board—as expected by many industry observers and financial analysts—on Aug. 31, 2021, by unanimous vote, rejected the CN-Kansas City Southern voting trust whereby shareholders in KCS would be paid before the transaction had received full approval by the regulator, effectively killing the merger, and opening the door for Canadian Pacific to re-engage with KCS on the CPKC (“Canadian Pacific Kansas City”) deal it struck with KCS on March 21, albeit with a sweetened offer.

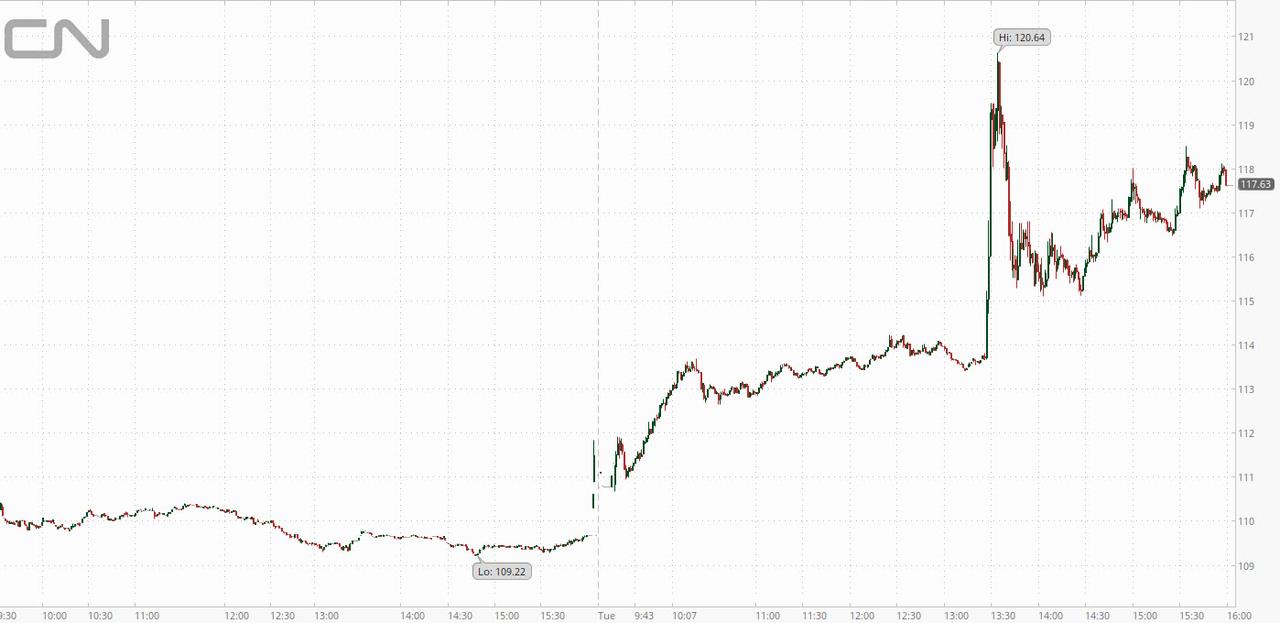

CN shares were up nearly 7 per cent in late Tuesday trade. CN and KCS could still choose to go ahead with the transaction without using a voting trust, but the regulator’s decision is likely to derail the deal altogether as shareholders of the US company are more likely to back an alternative union with rival railway group Canadian Pacific.

“The Board finds that the proposed use of a voting trust in the context of the impending control application does not meet the standards under the current merger regulations and therefore denies the applicants’ motion for authorization to establish and use the proposed voting trust,” STB said in Docket No. FD 36514 (downloadable below). “The Board has determined that the proposed voting trust is not consistent with the public interest standard under the Board’s merger regulations.”

Those merger regulation are the “new” ones established in 2001—new because they have thus far never been applied, and will not be in this case, provided that the CN-KCS deal is rejected by KCS shareholders on Sept. 3. A CP-KCS combination, if the two Class I’s rekindle their relationship, would be considered under the STB’s “old” (pre-2001) merger rules, with a CP-KCS voting trust pre-approved, and managed by the trustee—former KCS CEO Dave Starling—appointed by both Canadian railroads.

There were many factors STB considered in its decision. Several in particular stand out:

- “Many rail users said they are concerned that the 45% price premium CN has offered to acquire KCS, and the related debt burden it will incur to finance the purchase, would create incentives for CN to charge higher prices to current customers or decrease investment in CN’s network in order to improve financial performance; these commenters note that these incentives would arise whether or not a divestiture was ultimately required, because CN would be unable to rely on any of the merger “synergies” it plans for several years. They also argue that these risks would be increased if divestiture were required, both because CN would be unlikely to obtain a price that approaches the premium it paid for KCS, and because the economic climate in 2023 may be less favorable.”

- The Department of Justice, which has a statutory right to intervene through the Attorney General in Class I merger proceedings … filed comments on May 14, 2021, stating that the proposed acquisition ‘raises sufficient competition concerns on first blush that the CN should be prohibited from using a voting trust.’ DOJ argues that, even though the terms of the CN and CP voting trusts are similar, ‘the Board has good reason to hold CN’s proposed voting trust to a higher bar,’ because the diminished competitive incentives that arise from the unity in ownership created by a voting trust are heightened due to the direct parallel competition and overlapping routes in the CN and KCS networks. DOJ asserts that these threats to competition would be present immediately after the voting trust is consummated, and states that ‘[t]hese specific competitive concerns presented by CN’s proposed transaction magnify the general risks associated with voting trusts’ described in DOJ’s filing in Docket No. FD 36500, such that its concerns about the use of a voting trust in the proposed CP transaction ‘apply with greater force to CN’s proposed acquisition of KCS.’

- “DOJ also asserts that ‘[l]ike any other buyer that competes with its target, CN voluntarily assumed the risks associated with the regulatory review of the proposed transaction.’ DOJ argues that there are viable alternatives to the use of a voting trust that ‘better protect both firms’ incentives to compete vigorously’ while addressing regulatory risk, and asserts it is ‘particularly important to protect these incentives to compete where, as here, CN and KCS appear to compete head to head on multiple parallel routes.’ DOJ contends that ‘a strategic buyer should not be permitted to structure the deal in a manner that could give rise to anticompetitive effects simply because the alternative would be more expensive.’”

- “Applicants have not demonstrated that their use of a voting trust would have public benefits, and further finds that there are public interest risks to competition and divestiture associated with the use of a voting trust in the context of the impending control application. Accordingly, the Board finds that the use of a voting trust would not be consistent with the public interest and will deny Applicants’ motion for voting trust approval.”

- “Prevention of Unlawful Control: Applicants’ motion and supporting documents fail to address the subject of communications between KCS and CN during the trust period … Applicants make no provision for … an explicit acknowledgement that the trustee is responsible for implementing measures to monitor and assure that the information exchanges that occur between the carriers do not compromise the independent management and operation of the acquired company (Kansas City Southern) during the duration of the voting trust … Regardless of the deficiency described above regarding CN-KCS communications, which might otherwise be curable, the Board has determined that Applicants’ proposed use of a voting trust, in the context of their impending control application, is not consistent with the public interest.”

- “Applicants contend that they have shown that the proposed voting trust ‘would achieve substantial public benefits’ while presenting ‘no risk of harm to the public interest,’ and that their showing ‘overwhelmingly supports approval’ under the public interest standard established in 49 C.F.R. § 1180.4(b)(4)(iv) … [T]he Board finds that neither claim is persuasive and that it would not be consistent with the public interest to allow CN to acquire and place KCS into trust during the pendency of this control proceeding.”

- “Applicants’ … contention that a voting trust would serve the public interest by allowing CN and CP to compete to acquire KCS ‘on an equal footing’ fails to recognize two critical and related points. First … the two transactions are substantially different: The proposed CP-KCS transaction … is an end-to-end merger, whereas, here, the CN system overlaps with that of KCS. Second, the Board—after considering the overlapping routes and presently existing direct competition—agreed with CN’s commitment to file an application under the current regulations and thus placed the CN-KCS transaction under a different regulatory standard with respect to both approval of the transaction and use of a voting trust. These differences, particularly the heightened regulatory standards the CN-KCS proposal must meet, necessarily place CN’s proposal to acquire KCS on a different footing from Canadian Pacific’s proposal. Thus, the use of a voting trust for the CN-KCS transaction raises different and greater risks with respect to both competition and divestiture. Accordingly, Applicants’ contentions that approval is required because CN and CP are ‘two similarly situated potential acquirers, or because they may be ‘identically situated’ with respect to some factors pertinent to the Board’s consideration of a voting trust … are misplaced. To the extent the CN-KCS proposal is not on an ‘equal footing’ with the CP-KCS proposal, that is attributable to the differences in the governing regulatory standards and the proposed transactions themselves, and not the Board’s prior approval of a CP-KCS voting trust.”

- “Applicants’ related arguments—that the use of the voting trust ‘is crucial to place the CN-KCS transaction on a level playing field for KCS shareholders,’ and that ‘it would be fundamentally unfair for the Board to approve CP’s voting trust, and then to deny CN’s identical voting trust’ because ‘[t]his would effectively override KCS’s judgment about its preferred merger partner’—are equally misplaced. To be clear, the Board’s responsibility under these circumstances is to assess whether the proposed CN-KCS voting trust is ‘consistent with the public interest,’ … and not—as Applicants appear to argue—help private parties realize their transactional preferences regardless of that broader assessment. Like any rail carrier (or other bidder in a potential acquisition that requires regulatory review), CN had a choice about how to structure its offer; CN voluntarily assumed the risk that the voting trust might be rejected when it chose to make a voting trust an essential element of its offer, knowing that a CN-KCS proposed transaction presents geographic network overlap and that voting trusts must meet a heightened public interest standard for approval in major control proceedings under the current regulations. Similarly, KCS, as the potential acquiree, is in a position to weigh (among other things) the potential benefit of shorter or less burdensome regulatory review against potential benefits that a different proposal (with more demanding regulatory requirements) might provide, such as a higher purchase price … Accordingly, it is neither ‘fundamentally unfair’ nor does it improperly ‘override KCS’s judgment about its preferred merger partner’ to deny approval for the CN-KCS voting trust. KCS was not only aware of the regulatory risks associated with the proposed use of a voting trust in a CN-KCS transaction; it also appears to have engaged in negotiations with CN on that very issue before deciding to accept CN’s offer.”

- “The explanations Applicants offer to support their final claim—that a voting trust is necessary to serve the ‘undoubted’ public interest in ‘ensuring that merger decisions are made by capital markets, not by the Board’—also lack merit. As discussed above, their arguments that a voting trust is ‘essential’ to a competitive bid that would allow their transaction to go forward, and to respect KCS’s choice of a merger partner, are both unpersuasive as factual matters … Applicants essentially claim that there is a public benefit in allowing them to use a voting trust because they should be able to make merger decisions unfettered by regulatory requirements or uncertainty, or specific analysis of a transaction that may be distinguishable from that of other transactions. The Board disagrees. Applicants have failed to explain how their request to allow CN to acquire and place KCS into a voting trust would result in any material public benefit. … [P]lacing KCS in trust would insulate KCS and CN from the regulatory risks and uncertainties associated with the heightened scrutiny that the proposed transaction would face under the current major merger regulations and the heightened possibility of divestiture—an advantageous scenario for KCS shareholders and CN at the expense of the public interest in mitigating risks to competition and the stability of the rail network … Further, negotiation choices by private parties cannot control agency decision-making. CN’s choice to make a voting trust an element of its offer to acquire KCS cannot nullify an established regulatory standard that requires the Board to conduct an independent assessment of public interest considerations pertinent to the proposed use of a voting trust in a particular case.”

- “[T]he competition between CN and KCS via overlapping routes is apparent at this juncture, as the Applicants acknowledge for at least one route, and the potential harms to this competition constitute an important reason the transaction is subject to the new regulations and, in turn, the heightened voting trust standard. These are the exact harms (among others) the Board is tasked with preventing, or at least minimizing, as part of its public interest review. … For these reasons, in light of the overlap in Applicants’ networks, the Board finds that the use of the proposed voting trust creates competitive risks that are inconsistent with the public interest.”

- • “The Board emphasizes that it is not making a final determination regarding the extent of these competitive issues or whether they can be resolved. It is simply finding that, in view of the heightened scrutiny that both the use of a voting trust and the proposed transaction face under the current major merger regulations, it would not be in the public interest to allow CN to own KCS until the competitive issues have been thoroughly examined.”

- • “The possibility that a CN-KCS transaction would trigger downstream effects and, potentially, further consolidation initiatives, creates additional risks and uncertainties during the voting trust period.”

“[T]he Board finds that Applicants have not demonstrated that their use of a voting trust would be consistent with the public interest,” STB said in its conclusion. “Applicants have shown no benefit from the use of a voting trust to stakeholders other than KCS and CN. At the same time, the use of a voting trust, in the context of the impending control application, would raise risks that threaten to undermine the public interests the Board considers … These risks can be avoided, without preventing Applicants from continuing to seek approval for their merger plans, by not allowing the acquisition to take place until regulatory review of the transaction—the first to be considered under the Board’s current major merger regulations—is complete.

“It is ordered: Applicants’ joint motion for approval to use a voting trust is denied.”

Next Moves

As analyst Wolfe Research—without speculating on whether the voting trust would be approved or rejected— noted on Aug. 30, there are now two possible scenarios:

“CN could try and raise the bid for KCS yet again to try to convince KCS to wait out full merger approval to get a higher price. Alternatively, if the voting trust is rejected and CN doesn’t raise the bid again, it seems likely to us that KCS shareholders will vote against the merger with CN, and then KCS can re-engage with CP. In that scenario, KCS would owe CN a $700 million breakup fee. Given the [Aug. 30 Securities and Exchange Commission Schedule 13D] activist filing from TCI Fund Management Ltd. [which now is a ‘beneficial owner’ of CN with 5.2% of the company’s shares], it now seems less likely to us that CN would raise the bid again if the voting trust is rejected.”

Meanwhile, as the FT reports, UK hedge fund manager Chris Hohn has demanded that Canadian National abandon its $34bn pursuit of Kansas City Southern, after the US railroad regulator rejected the way the transaction was structured as it held the potential to harm the public interest.

In a letter to the board of CN seen by the Financial Times, the head of TCI, one of the largest shareholders in the Montreal-based company with a 5 per cent stake worth about $4bn, also called for the resignation of CN’s chair Robert Pace and chief executive Jean-Jacques Ruest.

https://ift.tt/3jw8Vcw

from ZeroHedge News https://ift.tt/3jw8Vcw

via IFTTT

0 comments

Post a Comment