How To Manage Risk In Crypto

Authored by Conor Ryder via Kaiko.com,

The FTX collapse was perhaps the single biggest risk management failure in the history of finance. Today, we provide a crash course in basic risk and liquidity metrics which should be required reading for anyone managing crypto investments.

We’ve seen enough incidents over the last few months, let alone years, to conclude there is a complete lack of adequate risk management in crypto. Throughout the Terra collapse, crypto credit crisis, and spectacular implosion of FTX we have collectively witnessed the industry’s largest (and most opaque) firms become insolvent in an instant.

This begs the question: where were the basic financial risk controls that are mandatory in any other industry?

A neglect of proper risk and liquidity management in a market as volatile as crypto has proven to be a death sentence for any business or investor. Today, we will demonstrate why risk metrics such as VaR and expected shortfall, alongside CeFi and DeFi liquidity metrics, are an absolute necessity for any crypto firm in a post-FTX world.

Part 1: Risk Metrics

While commonplace (and required by law) in traditional finance, risk metrics have been neglected in crypto largely because most crypto businesses have been extremely profitable up until lately. When numbers go up, risk management gets swept under the carpet. But the industry’s inherent lack of transparency and regulation has also contributed to a culture of negligence that eschewed basic controls.

Below, we explore three basic risk metrics: Value at Risk, expected shortfall, and implied volatility.

Value at Risk

VaR is a risk indicator to quantify the extent and probability of potential losses in a portfolio. It is particularly useful in risk management as it can essentially assign a cash value to a confidence level. These confidence levels usually range from 90% - 99%. For example, if the 95% daily VaR of my portfolio is $30k, it means that:

- My portfolio has a 95% chance of losing less than $30k over the next one day period.

- On average I will lose more than $30k one day out of 20 (5 days out of 100 = 5%).

VaR can be viewed as an acceptable loss, given a confidence level, which makes it a particularly useful metric for compliance purposes as well as capital requirement planning. Since the VaR for different confidence levels exhaustively describes the investment profitability, it can be used for investment management, allowing us to define limit-order levels to crystallize profits or cut losses.

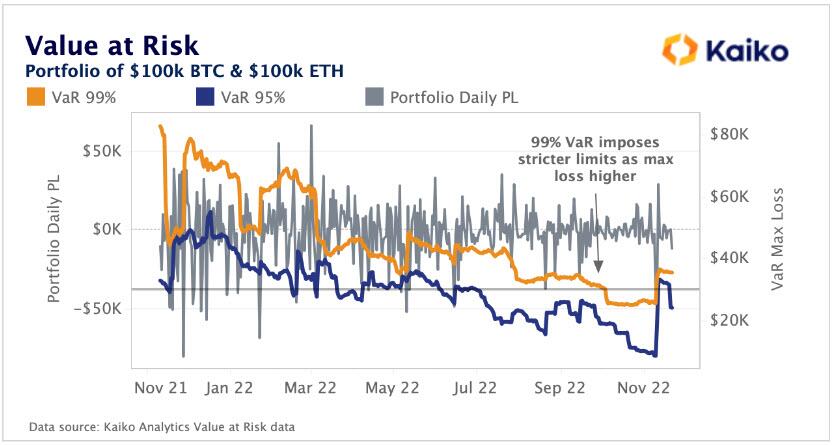

Kaiko’s VaR estimator can be applied to any cryptocurrency portfolio to accurately track VaR over time. Below, we have charted the Daily VaR of an equally weighted $200k portfolio of BTC and ETH.

Suppose I’m setting my risk budget for my portfolio, and I want a 95% probability of not losing more than $30k (-15%) each day. I would set my VaR confidence level to 95%, charted below, and monitor when my portfolio exceeds that $30k level. When the portfolio VaR exceeds that level I would look to de-risk my portfolio so that my Value-at-Risk is under that $30k threshold. We can see that in November as the FTX fallout began, VaR tripled in a matter of days to surpass the $30k max loss which would tell me to de-risk.

For a more conservative risk budget, perhaps for an exchange or lender, VaR at a 99% confidence level would be more appropriate. 99% VaR will impose stricter risk measures as the max loss is higher, due to the degree of certainty that it requires. We can see in the chart below that in times of higher volatility or returns, such as this time last year when the bull market came crashing to a halt, the max loss using 99% VaR was nearly double that using 95% VaR. This results in more stringent liquidity management being put in place, which will give businesses a better chance to remain solvent in volatile markets.

Expected Shortfall

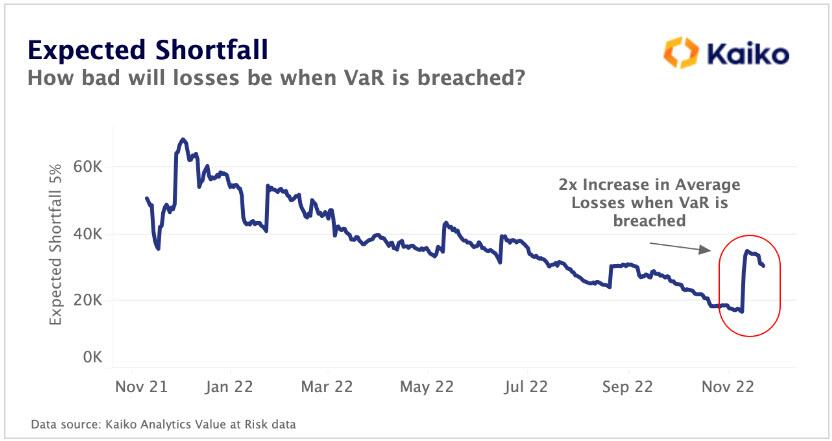

Expected shortfall (ES) is another useful metric, and particularly relevant for a volatile asset class like crypto where investors want to try and quantify their losses in the worst of cases. While VaR estimates a max loss 95% of the time, expected shortfall quantifies the average loss in the 5% of times. ES answers the question: If VaR is exceeded, how bad will our losses be?

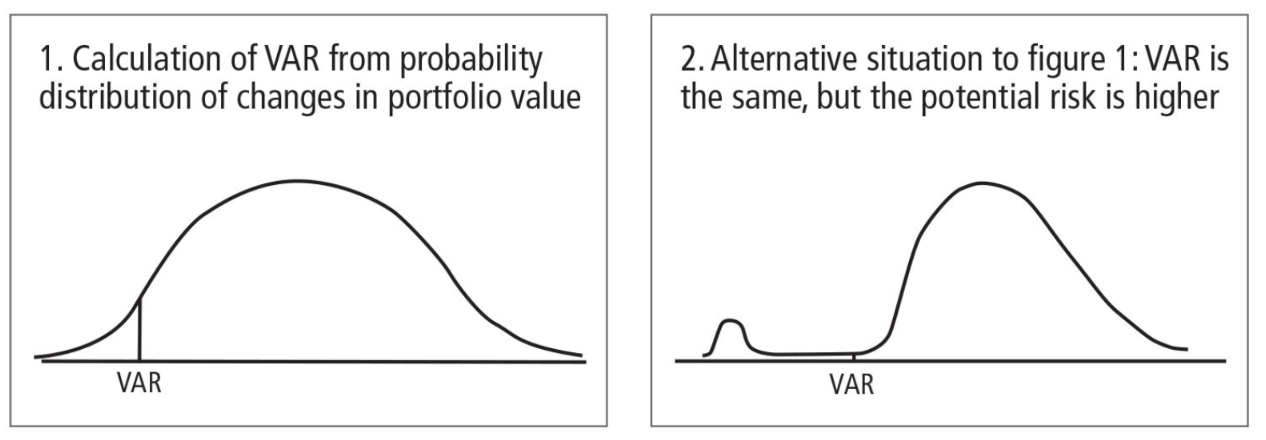

Distribution of returns in a crypto portfolio have historically had what are known as fat left tails, or black swan events, that alter the makeup of the return distributions. As we can see below, crypto markets exhibit more of the characteristics of chart 2. Both charts have the same VaR but result in different expected shortfalls: chart 2 losses are more extreme in the worst case scenario.

Charting the expected shortfall, or the average loss in the worst 5% of scenarios, for the same $200k portfolio above, we observe a decline in the average loss this year as crypto volatility generally eased. However, we can see expected shortfall spike during the recent FTX collapse, doubling in a matter of days. ES compliments VaR and gives risk managers a sense of how bad things may get in the worst of scenarios. This allows business to determine a risk budget, ensuring solvency during market crashes.

Implied Volatility

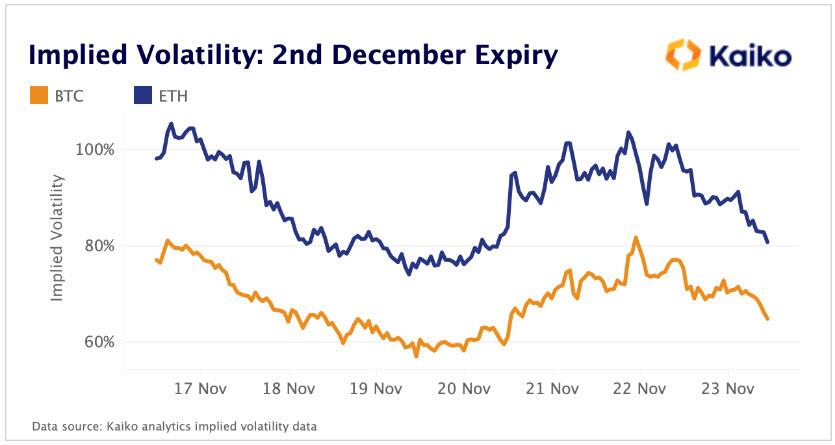

Risk managers can also turn to the options market to get a better idea of how much risk is being priced into markets. Volatility is one of the criteria that makes up an option price, and by calculating how much volatility the market is pricing into an option, it is possible to come to a conclusion as to how much volatility to expect until the option expiration date. Using the December 2nd expiry date as an example, the market is pricing in implied volatility of 81% for ETH options until the end of the month, decreasing from 98% since mid-November. Implied volatility can be one of the most useful metrics risk managers monitor when looking to adjust the risk of the portfolio.

Part 2: Liquidity Metrics

Market Depth on Centralized Exchanges

Two of the black swan events this year, the collapse of Celsius and FTX, were directly related to liquidity issues surrounding stETH and FTT, respectively. Holders of either tokens could have seen that there was little to no liquidity available on spot markets and if everyone rushes to the exit at the same time, the price of the token crashes.

We saw this happen with stETH, which hit a discount of +6% as liquidity dried up on exchanges as Celsius rushed to liquidate their holdings amid record redemption requests for ETH.

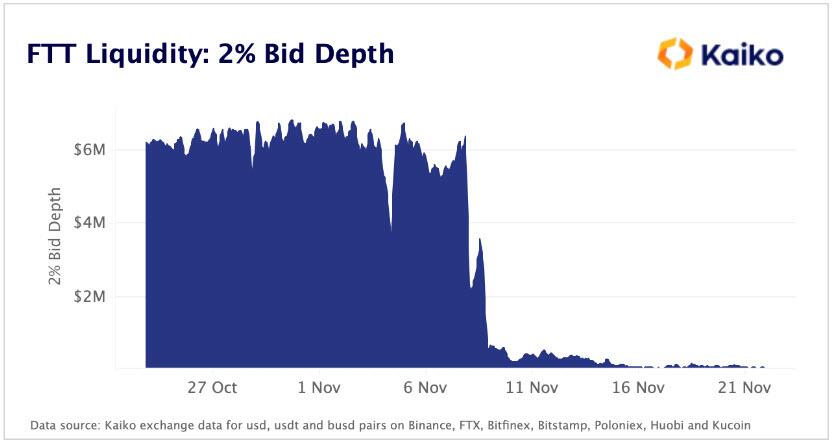

FTT didn’t have many buyers apart from FTX themselves, and the bid side liquidity was not enough to support immense selling pressure of the token throughout the FTX scandal, despite Alameda’s best efforts to defend the price. Bid side liquidity within 2% of the mid price for FTT was only $6m pre-collapse. A fund engaging in adequate liquidity management would have flagged this and likely reduced exposure to FTT on the off-chance a rush to the exit happened.

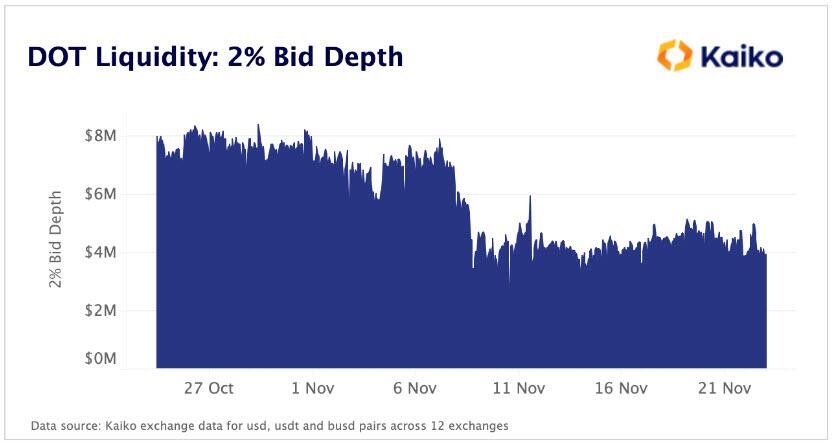

Looking at some other tokens which could be relevant from a liquidity management perspective, DOT, the token of the Polkadot ecosystem, had very similar bid depth to FTT pre-crash. Post-crash, DOT only has about $4m of bid side support within 2% of the mid-price across 12 exchanges it trades on, meaning a wave of sell orders could quickly crash prices.

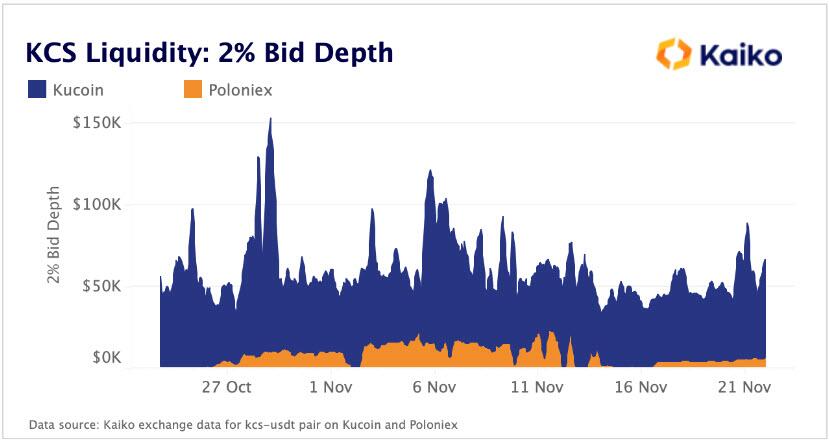

KCS is the native token of the Hong-Kong based exchange Kucoin. Kucoin is ranked 32 out of 42 exchanges in the latest Kaiko Exchange Ranking, largely thanks to a 42/100 score for Governance. According to recent proof of reserves releases from exchanges, the Block claims Kucoin holds nearly 20% of its reserves in its own token, KCS. Looking at 2% bid depth for KCS we can see there is only about $60k of bid side support for the token. A rush for the exit could see the KCS price crash and Kucoin taking a significant hit to their reserves.

Understanding liquidity is thus a vital component in a robust risk management framework. The valuation of a fund's balance sheet is only as strong as its ability to efficiently liquidate their holdings.

DeFi Liquidity Data

As centralized and decentralized markets become increasingly integrated, CEX market depth is no longer enough to fully understand a cryptocurrency’s liquidity

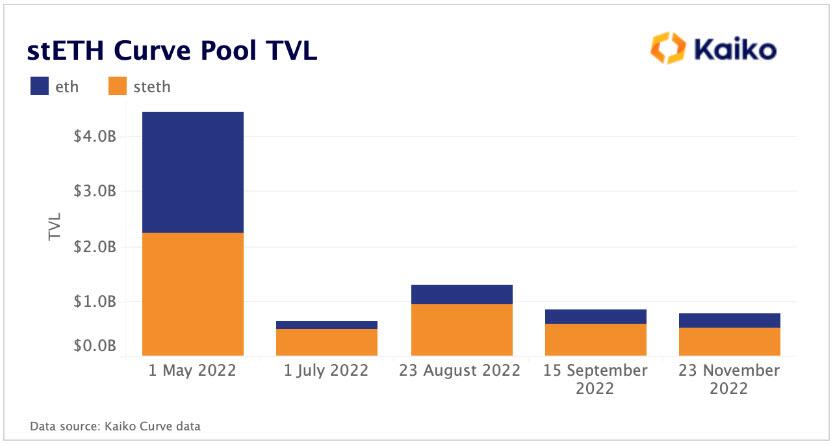

As mentioned earlier, staked Ether (stETH) played a large role in the liquidity issues faced by Celsius and Three Arrows Capital this summer. This caused market wide contagion at the time as investors scrambled to cash out of stETH and move into the more liquid ETH. In this case, the majority of liquidity for stETH wasn’t on centralized exchanges; rather, it was in DEX liquidity pools.

Diligent monitoring of the Curve stETH/ETH pool would have flagged a drop in the total value locked in real time as stETH made up over 80% of the pool at the height of the rush for liquidity. That allocation has improved slightly since, but remains quite imbalanced as stETH now makes up 67% of the pool.

Going forward, crypto firms will need to understand liquidity on both centralized and decentralized markets to be able to simulate large liquidations and price impact.

Part 3: Exchange Due Diligence

The importance of exchange due diligence has never been more relevant than it is today. FTX was one of the most trusted names in all of crypto, but after Coindesk did a bit of digging the whole charade unraveled and FTX ended up insolvent. Not only did customers lose money, but many sophisticated hedge funds and trading desks had their funds stored on FTX and now have to explain that decision to investors.

It is vital that going forward, as part of a robust risk management process, that businesses do their due diligence on exchanges, monitoring everything from liquidity to governance. Kaiko is aiming to assist investors in this vetting process for exchanges with our Exchange Ranking, which is structured around six criteria with a proprietary scoring methodology internally developed and maintained by Kaiko’s Indices team. Over the next few months, we will incorporate proof of reserves and other transparency metrics into this ranking.

Conclusion

When liquidity is plentiful, risk management is less of a concern as most companies’ balance sheets look healthy and liquid. However, when a bear market hits, the tide goes out and we see who was swimming naked. Those with significant positions in illiquid tokens, such as FTT or stETH, have paid the price for not monitoring the liquidity of those positions and not accurately assessing the outsized risk of their positions should prices go down.

Risk management and crypto are two words that up until lately have rarely been mentioned in the same sentence. To quote the new CEO of FTX, John Ray III, he had never seen “such a complete failure of corporate controls and such a complete absence of trustworthy financial information.”

If businesses investing in crypto are to survive going forward, risk management must play a central role in the investment process. Liquidity metrics, combined with traditional risk metrics such as VaR or Expected Shortfall will allow investors to survive bear markets like these and reap the rewards of survival come the next bull market.

* * *

Learn more about Kaiko's Value at Risk, Implied Volatility, and liquidity data.

https://ift.tt/taslzGN

from ZeroHedge News https://ift.tt/taslzGN

via IFTTT

0 comments

Post a Comment