Failure To Bury "Transitory" Inflation Narrative Risks Sparking Biggest Fed Error In Decades: El-Erian Warns

Authored by Tom Ozimek via The Epoch Times,

Failure on the part of the Fed to toss its stubbornly-held “transitory” inflation narrative and act more decisively to rein in persistently high price pressures raises the likelihood the central bank will need to slam on the brakes of easy money policies much more forcefully down the road, risking avoidably severe disruption to domestic and global markets, according to Queen’s College President and economist Mohamed El-Erian.

“In stark contrast with the mindset of corporate leaders who are dealing daily with the reality of higher and persistent inflationary pressures, the transitory concept has managed to retain an almost mystical hold on the thinking of many policy makers,” El-Erian wrote in an Oct. 25 op-ed in Bloomberg.

“The longer this persists, the greater the risk of a historic policy error whose negative implications could last for years and extend well beyond the U.S.,” he argued.

Consumer price inflation is running at around a 30-year high and well beyond the Fed’s 2 percent target, to the consternation of central bank policymakers who face increasing pressure to roll back stimulus, even as they express concern that the labor market hasn’t fully rebounded from pandemic lows.

The total number of unemployed persons in the United States now stands at 7.7 million, and while that’s considerably lower than the pandemic-era high, it remains elevated compared to the 5.7 million just prior to the outbreak. The unemployment rate, at 4.8 percent, also remains above pre-pandemic levels.

At the same time, other labor market indicators, such as the near record-high number of job openings and an all-time-high quits rate—which reflects worker confidence in being able to find a better job—suggest the labor market is catching up fast. Businesses continue to report hiring difficulties and have been boosting wages to attract and retain workers. Over the past six months, wages have averaged a gain of 0.5 percent per month, around twice the pace prior to the pandemic, the most recent jobs report showed.

Besides measures of inflation running hot, consumer expectations for future levels of inflation have hit record highs, threatening a de-anchoring of expectations and raising the specter of the kind of wage-price spiral that bedeviled the economy in the 1970s. A recent Federal Reserve Bank of New York monthly Survey of Consumer Expectations showed that U.S. households anticipate inflation to be 5.3 percent next year and 4.2 percent in the next three years, the highest readings in the history of the series, which dates back to 2013.

El-Erian, in the op-ed, argued that the Fed has “fallen hostage” to the framing that the current bout of inflation is temporary and will abate once pandemic-related supply chain dislocations will abate.

“It is a framing that is pleasing to the ears, not only to those of policy makers but also those of the financial markets, but becoming harder to change,” he wrote.

“Indeed, the almost dogmatic adherence to a strict transitory line has given way in some places to notions of ‘extended transitory,’ ‘persistently transitory,’ and ‘rolling transitory’—compromise formulations that, unfortunately, lack analytical rigor given that the whole point of a transitory process is that it doesn’t last long enough to change behaviors,” he wrote.

El-Erian said he fears that Fed officials will double down on the transitory narrative rather than cast it aside, raising the probability of the central bank “having to slam on the monetary policy brakes down the road—the ‘handbrake turn.'”

“A delayed and partial response initially, followed by big catch-up tightening—would constitute the biggest monetary policy mistake in more than 40 years,” El-Erian argued, adding that it would “unnecessarily undermine America’s economic and financial well-being” while also sending “avoidable waves of instability throughout the global economy.”

His warning comes as the Federal Open Market Committee (FOMC)—the Fed’s policy-setting body—will hold its next two-day meeting on November 2 and 3.

The FOMC has signaled it would raise interest rates sometime in 2023 and begin tapering the Fed’s $120-billion-a-month pandemic-era stimulus and relief efforts as early as November.

Some Fed officials have said that, if inflation stays high, this supports the case for an earlier rate hike. Fed Governor Christopher Waller recently suggested that the central bank might need to introduce “a more aggressive policy response” than just tapering “if monthly prints of inflation continue to run high through the remainder of this year.”

“If inflation were to continue at 5 [percent] into 2022, you’ll start seeing everybody potentially - well, I can’t speak for anybody else, just myself, but - you would see people pulling their ‘dots’ forward and having potentially more than one hike in 2022,” he said in prepared remarks to Stanford Institute for Economic Policy Research.

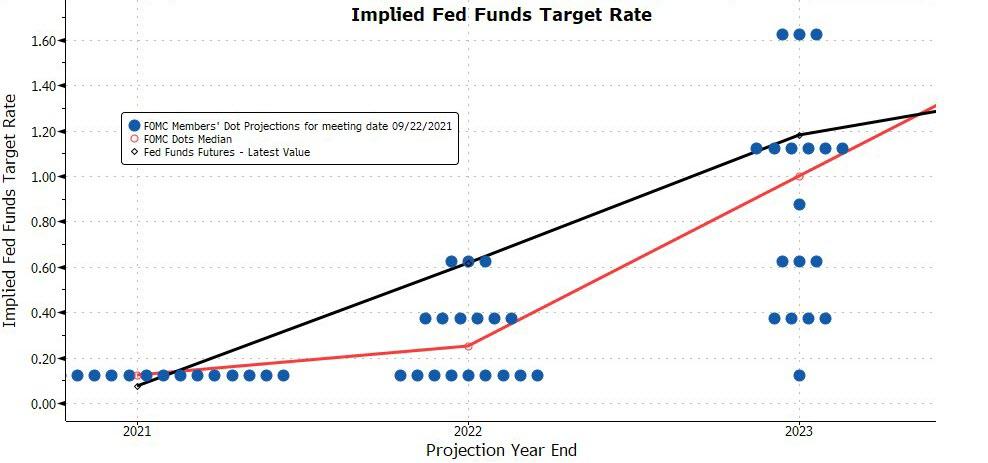

The Fed’s dot plot (pdf), which shows policymakers’ rate-hike forecasts, indicates half of the FOMC’s members anticipate a rate increase by the end of 2022 and the other half predict the beginning of rate increases by the end of 2023.

For now the market is pricing in a more hawkish Fed response in 2022

https://ift.tt/2ZuaZdG

from ZeroHedge News https://ift.tt/2ZuaZdG

via IFTTT

0 comments

Post a Comment